How to Create a Personal Balance Sheet (Examples & Templates)

Published on: 02/07/2023

If you’re struggling with your financial situation and are looking for strategies to help you gain control, you may want to consider creating a personal balance sheet.

By tracking your total assets, like cash and personal property, and total liabilities, like personal loans or credit card debt, a personal balance sheet gives you more insight into your financial health, and helps you work to grow your assets while reducing your liabilities.[1]

In this article, we go over what a personal balance sheet is, how to create one and how to use it as an effective tool in your financial planning.

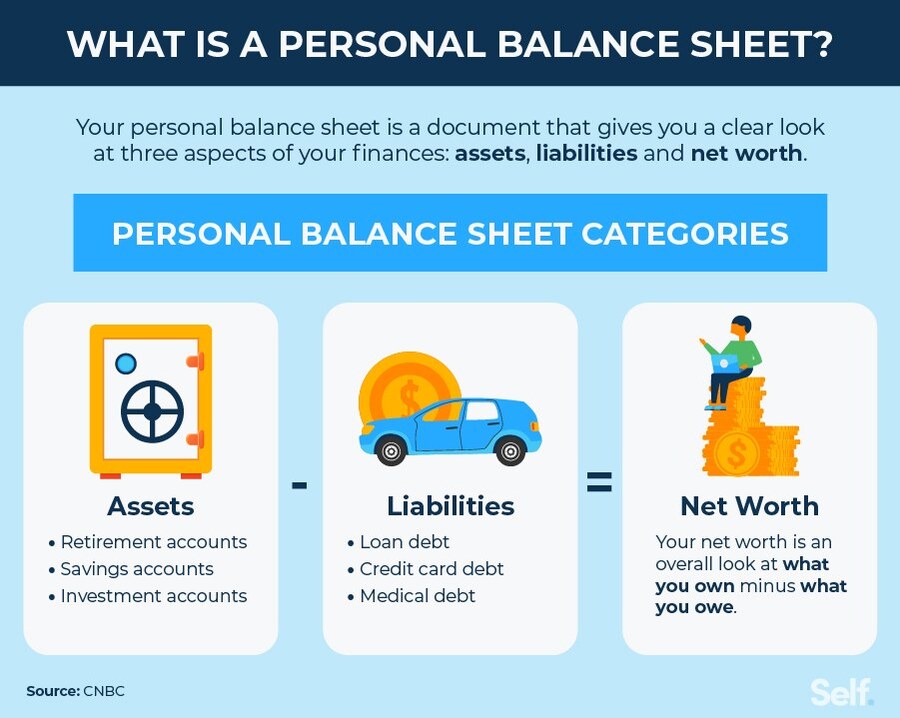

What is a personal balance sheet?

A personal balance sheet is a summary of your overall financial situation at a specific point in time. It includes your current assets, or what you own, as well as your liabilities, or what you owe. By subtracting your assets from your liabilities to calculate your net worth, it creates a picture of your financial position.[1]

Consulting a personal balance sheet can help you prioritize debt repayment and make other important financial decisions, like taking out a car loan. The sheet should be updated at least once a year to give you an accurate sense of your personal finances during different moments of time. It can also be updated periodically, alongside significant life changes like getting a higher paying job, getting married, having a child or buying a home.[1]

Depending on your financial situation, it’s possible that creating a personal balance sheet might reveal that you have a negative net worth. Many people have a negative net worth — this indicates that you owe more than you own.

Becoming more aware of your overall financial situation and tracking your debts and liabilities can help improve your personal net worth by helping you make better financial decisions and allowing you to target your debt repayment efforts.[2]

What’s the difference between a personal balance sheet and a cash flow statement?

Though both are personal financial statements, a personal cash flow statement is different from a personal balance sheet. A cash flow statement focuses more on how money comes in and where your money is being spent, rather than giving an overview of all assets and liabilities that a person has. A cash flow simply refers to your total personal income, or what amount is coming in, minus your expenses, or what amount is going out.[3]

Cash flow statements can be useful to track your spending habits, but they may not give quite as much insight into your overall financial health as a personal balance sheet does. It can be useful to review both reports together to get a more thorough understanding of your finances.

What are the main categories to include on a personal balance sheet?

Personal balance sheets are made up of three main categories: assets, liabilities and net worth:

- Assets — what you own: Your total assets can include direct business holdings, real estate holdings and financial assets. Financial assets include liquid assets, like cash and money in a checking account, savings account or mutual fund, and non-liquid assets, like personal property, retirement accounts and certificates of deposit.

- Liabilities — what you owe: Your total liabilities can include debt, from things like credit cards, personal loans, student loans, car loans, home equity lines or other lines of credit.

- Net worth — the difference between assets and liabilities: Your net worth is your total wealth, taking into account all of your assets and liabilities. You arrive at this number on your personal balance sheet by subtracting your total liabilities from your total assets.[1]

Creating your personal balance sheet

Follow these steps to create your own personal balance sheet.

1. Create a categorized list of your personal assets

Personal assets are what you own. Assets are what make up the value of your wealth, and adding them up gives you a sense of where you stand financially.[1]

Personal assets generally fall into these categories:

- Liquid assets: A liquid asset is anything you have with an immediate cash value or that can be easily converted into cash quickly. The most common examples are cash and cash equivalents, like money in your checking account or a money market fund.

- Personal property and equity: These assets are non-liquid and are assessed using their market value. Sometimes the value of your property can depreciate over time, like in the case of a car you own (have title to), or appreciate, like in the case of a rare collectible. This category also includes equity in business or real estate, like if you own a home or have a stake in a small business.

- Investment accounts: Investment accounts allow you to buy and sell a variety of investments and securities. Common examples include mutual funds, stocks and bonds.

- Retirement accounts: Retirement accounts are similar to investment accounts but are generally deferred until retirement age, meaning you can’t access them until you reach that age or you pay a penalty. Common examples include IRAs and 401(k)s.

[4]

2. Create a categorized list of your personal liabilities and debts

Personal liabilities and debts are the amounts you owe to various lenders, whether it’s a personal loan, line of credit or other account. Having a clear picture of the amounts you owe helps you not only keep track of how much debt you have, but also gives you a sense of how your liabilities compare to your assets.[1], [3]

Personal liabilities generally fall into these categories:

- Outstanding balance on loans: This is what you owe on any installment accounts you might have. Loans include personal loans, student loans, car loans and mortgages.

- Outstanding balance on revolving credit: This is what you owe on any revolving credit account you might have. A common example is having an unpaid credit card balance.

- Outstanding medical bills, taxes and other debts: This includes debt that has accumulated from other sources, whether it’s medical collection accounts, unpaid taxes or other debt owed to creditors.

- Other financial obligations: This category considers any other financial obligation you may have, including the debts of other family members, or other monthly payments you need to make.

[5]

When documenting your liabilities, you’ll also want to include the interest rates associated with your accounts. When you analyze your personal balance sheet, this will show you where you’re paying the most in interest and help you make informed decisions about which debt to pay down first. For example, you may choose to use the debt avalanche method where you pay down debt with the highest interest first.

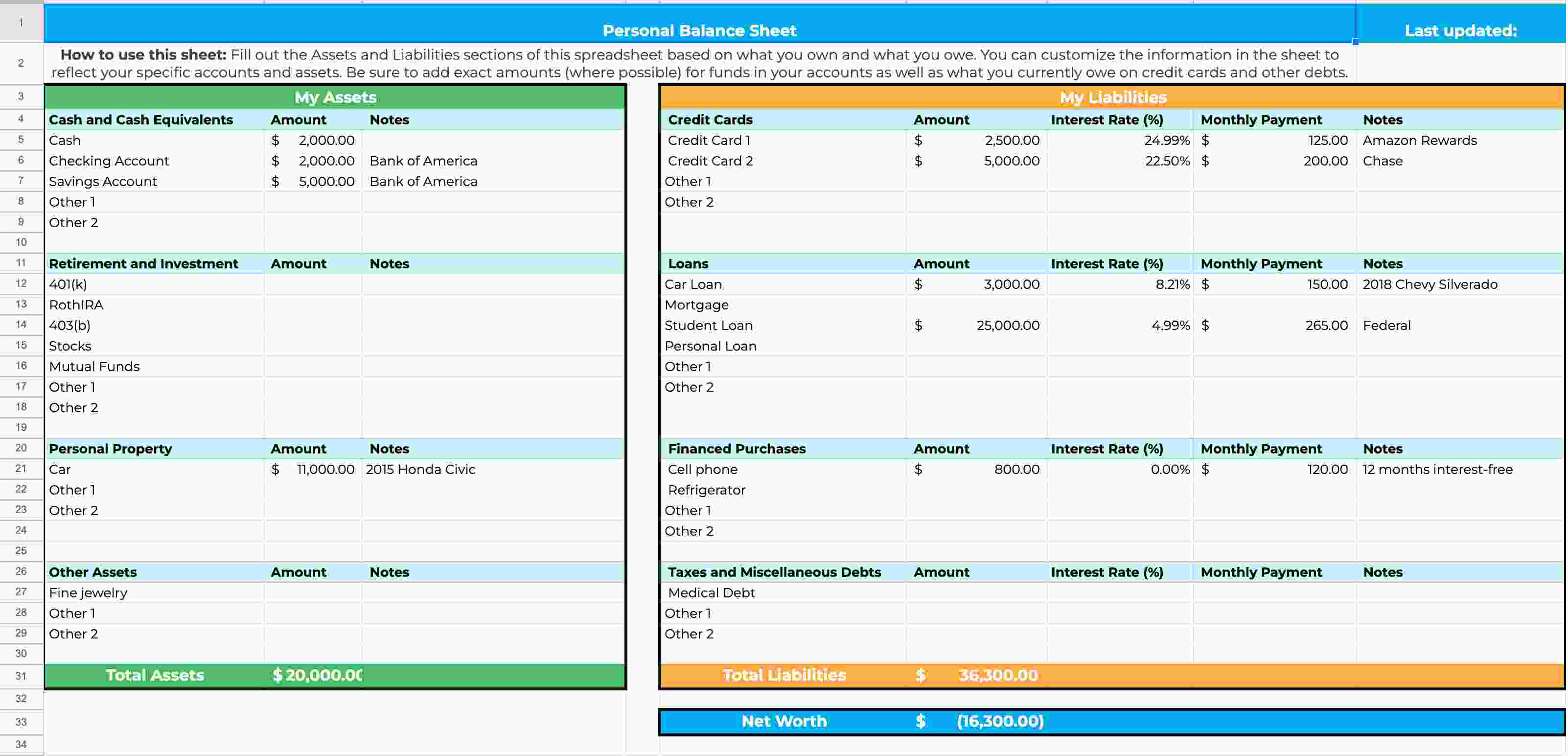

3. Add columns for your personal assets and debts onto your balance sheet

A personal balance sheet combines these two categories so that you can see them side-by-side. Being able to see both items that add to and subtract from your net worth helps give you a better sense of the total amount of wealth you have, and how you arrive at that amount.[1]

4. Check your balance sheet for any missing information or discrepancies

When preparing your balance sheet, be sure to double-check that all information is accurate. Missing an item or having discrepancies in what you include will throw off the calculation.

5. Use your assets and debts to calculate your personal net worth

A basic formula for calculating your personal net worth is:

- Add up all of your assets.

- Add up all of your liabilities.

- Subtract your total liabilities from your total assets.

This gives you your total net worth, or amount of wealth. Knowing your personal net worth and how you arrived at it gives you valuable insight into your current financial position and can help you in financial planning going forward.[2]

Use your balance sheet to identify areas for improvement in your finances

By giving you insight into your personal finances, a completed personal balance sheet can give you an idea of how to improve your financial situation.[1] These sections explore the steps you can take.

Consider how interest rates affect your overall financial situation

When considering your total liabilities, you should also be looking at the interest rates on each loan or credit card you add to your balance sheet. Including this gives you a better idea of where you are paying out the most in interest, which might help you prioritize where to focus your repayment efforts better.

For example, if you have a credit card with a $1,000 balance and very high interest rate, you might want to focus on paying that card off in full before targeting another debt that will take longer to pay off but has a lower interest rate, like an installment loan.[6]

Identify your liabilities with the highest debt and make a targeted repayment plan

A completed balance sheet will also show you where you owe the most money. Comparing how much you owe on each debt, and the corresponding interest rates, will help you come up with a debt repayment plan.

Two common debt repayment strategies are debt snowball and debt avalanche. With each, you make the minimum payment on each debt and apply extra cash to one particular debt. Using the debt snowball method, you apply that money toward paying off the smallest debt first. Under the debt avalanche method, you focus on paying off the highest-interest debt first.

Use your personal balance sheet to ensure you are protecting your assets

Knowing the value of your assets can help you protect your wealth better. If you have a full picture of where you stand financially and how much wealth you actually have, you’re likely to be more careful about the amount of debt you take on. This way, you protect your assets from any potential loss that could come from liabilities getting out of control. For example, if you have a lot of equity in your home, you may hold off on getting more revolving accounts so that you can help prevent overextending yourself and your mortgage continues to be paid.

Consult your personal balance sheet before making big financial decisions

The personal balance sheet can be a valuable financial tool, helping you make more informed financial decisions. If you’re facing a big decision, like taking out a loan, switching careers or making a large purchase, it’s better to go into it knowing your assets and liabilities.

A personal balance sheet helps you reflect on your net worth, whether positive or negative, and identify areas where you can work to improve it. You can use this information in tandem with your cash flow statement to help you create a budget and pay down your debt.

What should your balance sheet look like when finished?

When it’s complete, your personal balance sheet should contain columns for your assets and liabilities, and an area where your net worth is automatically calculated using the sum of each. Programs like Excel have spreadsheets that can calculate these values for you using simple formulas. Download our customizable personal balance spreadsheet template below.

Knowing your financial situation is key to improving financial health

It can be scary to look into your finances, but organizing your assets and liabilities in one place gives you invaluable insight into your current financial situation. Using a personal balance sheet, along with other good habits, like checking your credit report, can show you where you need to try to improve and how to work towards your financial goals.

Sources

- CNBC. “Do you know your net worth? Create a personal balance sheet to find out,” https://www.cnbc.com/2020/04/18/why-you-should-create-a-personal-balance-sheet.html. Accessed January 3, 2023.

- CNBC. “What is net worth and why is it important?” https://www.cnbc.com/select/what-is-net-worth/. Accessed January 3, 2023.

- Experian. “How to Create a Personal Cash Flow Statement,” https://www.experian.com/blogs/ask-experian/how-to-create-personal-cash-flow-statement/. Accessed January 3, 2023.

- Investopedia. “What Is an Asset? Definition, Types, and Examples,” https://www.investopedia.com/terms/a/asset.asp. Accessed January 3, 2023.

- Investopedia. “Liability: Definition, Types, Example, and Assets vs. Liabilities,” https://www.investopedia.com/terms/l/liability.asp. Accessed January 3, 2023.

- Equifax. “What Do Interest Rates Really Mean?” https://www.equifax.com/personal/education/personal-finance/what-do-interest-rates-mean/. Accessed October 14, 2022.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).