What Is A Balance Transfer and How Does It Work?

A balance transfer refers to moving debt from one or multiple accounts into a new account. Typically, you do this to consolidate debt into one account with a lower interest rate, which may save you money on interest as well as combine your debt into one payment. Sometimes you can find balance transfer credit cards with 0% APR introductory offers, meaning you may not have to pay interest if you pay off your debt prior to the offer’s expiration.

This post explains how to move debt to a new account and details how a balance transfer may affect your credit score and credit history. If you want to better manage your high-interest debt, you can discover the advantages and disadvantages of a balance transfer as well as review some alternatives so that you make the best decision for your financial situation.

How a balance transfer works

Because you may need to transfer different types of debt to a new account to avoid getting charged high interest rates, we walk you through what it takes to implement a balance transfer.

1. Review your existing debt balances

Take the first step by understanding exactly what existing debt balances you have and what interest rates the financial institutions are charging you. Create a spreadsheet and make a list of each account you have, the total balance on the account, and the interest rate. For credit cards, you can locate the interest rate by checking your current credit card statement or call the number on the back of the card. After you evaluate your balances and interest rates, you can better assess your needs.

2. Pick a balance transfer card that is suited for your needs

Once you know what you owe and what interest rates you’re charged, you can get a good idea for how much you need to transfer and how low the interest rate needs to be to make a balance transfer worth it.[1]

Read through the policies for each of the cards involved in your search. Some of them may have fees and penalties for balance transfers that could affect your decision. When choosing the card to transfer to, consider the following:

- Type of credit card issuer: Creditors may not allow transfers from an existing card of theirs — they prefer to gain balances from old cards and accounts affiliated with other financial institutions. Make sure to check with your issuer.

- Length of the introductory period: If they offer only an introductory interest rate for your balance transfer, check to see how long the intro period lasts. If you can’t pay off the balance before that period of time ends, the interest rate may change and make the payments unmanageable.

- The type of debt you are allowed to transfer: Check to see if you can transfer types of debt, such as auto loans, personal loans, and private student loans, in addition to high-interest credit card debt.

- Additional fees: Although the balance transfer rate may look like a good deal, consider all the costs associated with the card, including annual fees, balance transfer fees and penalties.

Read the fine print and keep in mind that each balance transfer process may be different based on the bank’s policies or credit card agreement. Not all offers impact your financial situation the same way so weigh your options carefully.

3. Apply for the new card and wait to be approved

If you’ve decided to apply for a new account, you have to submit an application, and the credit card issuer will pull your credit report and score. Knowing your credit score before you apply can help you see if you meet the minimum qualifications for the financial institution before you even consider applying.[2]

If you meet the minimum requirements, some of the information they may ask for includes:

- Name

- Address

- Social Security number

- Housing or monthly expenses

- Income[2]

4. Transfer the balance to the new credit card

Once you’re approved, your creditor establishes a credit limit. Check to see if that covers all of the debt you want to transfer, factoring in the balance transfer fee that will be added after you transfer the debt. Gather the account numbers for debt you plan to move as well as the total of each balance.[2]

Your new card issuer may supply you with balance transfer checks. You may also be able to initiate the transfer online by logging into your account. If you’re having trouble, call the customer service number on the back of the card.[3]

5. Wait for the transfer to go through

It usually takes 5 to 7 days for a balance transfer to go through, but it can take up to 21 days for some credit card companies.[4] Make sure you check the old accounts for payment due dates so you don’t miss any payments while the transfer is going through, as that may ding your credit score and result in late fees.[2]

6. Confirm the transfer and pay down your new balance

Once the balance transfer has gone through, take steps to confirm the transfer and pay down your debt:

- Set up autopay. Using automatic payments may help you make payments on time every month.

- Check the old accounts. Verify that the transfer went through and you no longer owe anything on that account.[2]

- Put a new payment plan into your budget. Try to pay more than just the minimum payment so you can pay it off faster.[5]

- Budget to pay off the new credit card before the introductory period ends. If you transferred the debts to a credit card with an introductory period, which usually lasts 6 to 18 months, paying the balance before the introductory interest rate changes may help you avoid paying a higher interest rate.[3]

How balance transfers affect your credit

Balance transfers may offer savings on interest and can simplify your monthly payments, but they do affect your credit. Your credit score assesses several factors of your credit history, many of which change — good or bad — with a balance transfer:

- Results in a hard inquiry: Applying for a balance transfer means potential creditors perform a hard inquiry into your credit, which temporarily lowers your credit score a few points.[6]

- Changes the age of your credit: Typically, a lengthier credit history impacts your score favorably, but when you open a new account, you add an account with a young age to your credit history.[7]

- Adjusts your credit utilization ratio: Since you’re opening a new line of credit, your credit utilization ratio may change, which can also impact your credit score. Adding a new line of credit without closing other accounts may improve your credit utilization, but if credit scoring models consider each individual account, then your ratio increases may negatively affect your score.[8]

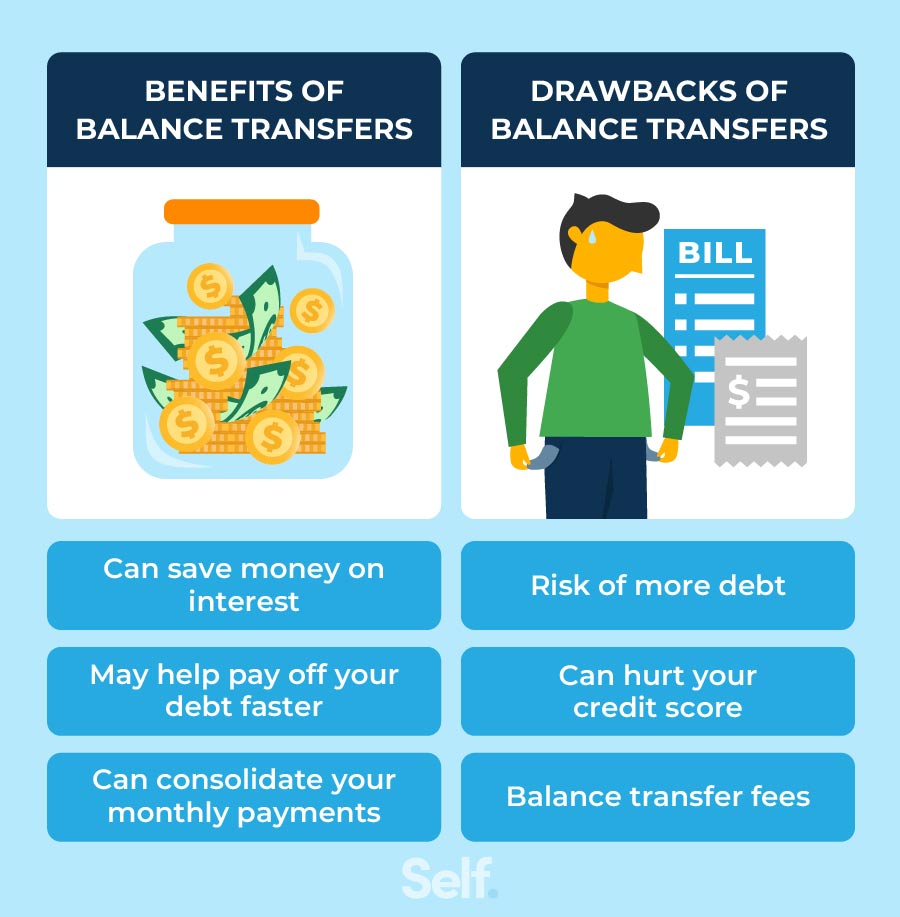

Pros and cons of balance transfers

Balance transfers may not be the right choice for your situation. Before making the decision to do one, consider the pros and cons.

Pros

- Can save money: If you’re transferring high-interest debt to a low-interest account, you may save money each month on interest.

- Consolidates payments: Instead of making multiple payments on different days scattered throughout the month, you’re making one monthly payment, which helps you keep up with payments easier.

- May help you pay off debt faster: If you get a low introductory APR that saves you money in interest each month, you can focus on paying off the debt faster during the promotional period.

Cons

- May lower your credit score: Because you’re opening a new account, that means you’re making a hard inquiry on your account and lowering the average age of all your accounts, which may impact your credit score.[8]

- May add fees: Balance transfers typically have fees associated with them (usually 3% to 5%) so if you’re not dropping your interest rate that much, you may not actually be saving money. Read the fine print first.[9]

- Can cause more debt: By transferring your debt to a new account, that clears up the remaining balances on old accounts, but you may be tempted to use that extra available credit for new purchases, which just adds to your existing debt.

Is a balance transfer right for you?

Deciding whether a balance transfer is right for you means both weighing the pros and cons and doing some calculations. These next sections walk you through a couple of scenarios to give you an idea for when a balance transfer may be a big money-saver or a pass.

Scenario 1:

Jill has a $2,000 balance with a 25% interest rate. Her monthly payment is $100, meaning it would take 27 months to pay off the account and she would pay a total of $2,614 over that period, with $614.04 of that being interest charges.

Because she has excellent credit, she qualifies for a balance transfer card with a 4% transfer fee ($80) and a 21-month 0% APR (annual percentage rate) introductory period (as long as payments are made on time). By transferring her balance to this account and paying $99 per month, she would pay off the account before the intro APR period ended and 6 months faster, paying just $2,080 and saving $534 in the process.[10]

Scenario 2:

Jack has the same financial situation as Jill, but he does not get approved for the 0% APR introductory offer. Instead, the credit card company approves him for a balance transfer card with an APR offer of 23% and a 4% transfer fee. Jack would have to also keep the payment at $100. While the APR is slightly lower than his current credit card, the total interest accumulated before the account is paid off would be $599. If you add the transfer fee of $80, Jack would end up paying $65 more than if he had simply kept paying off the current card.[10]

Before you determine whether to do a balance transfer, gather the following information to help you calculate how much you may pay in extra interest and fees for each option before you pay the account off:

- The current balance on any cards you want to pay off

- The interest rate on each card

- Your current monthly payments

- Any fees associated with balance transfer offers

Balance transfer alternatives

Although you may lower your debt and save money on interest with a balance transfer, you can explore other options that may offer a better solution for your financial situation.

Credit counseling

Credit counseling provides another set of eyes to examine your finances and help you figure out a way out of debt. Your credit counselor may also be able to negotiate with your current creditors on late payment fees or interest rates to help you pay down the debt faster.

Debt management program

A nonprofit credit counseling agency may recommend that you consider a debt management program. With this program, the agency will help you create a long-term plan for paying off debt, typically at a lower rate. This plan typically involves consolidating debt and paying it off in 3- to 5-year plans. These agencies usually do charge fees for the debt management program so be sure to seek out a reputable agency with reasonable fees.

Debt consolidation

Debt consolidation can be in the form of a personal loan or using a home equity loan that consolidates all your debts into one account. However, keep in mind that you may not qualify for a lower interest personal loan. In addition, if you are struggling financially, you may not want to take unsecured debt and secure it with your home.

Weigh your options

A balance transfer may help you pay less interest. However, that’s not always the case. Make sure to calculate interest and fees over the term of the loan to determine if a balance transfer will save you money.

Sources

- Experian. “How to Choose the Right Balance Transfer Credit Card,” https://www.experian.com/blogs/ask-experian/how-to-choose-the-right-balance-transfer-credit-card/. Accessed May 27, 2022.

- Forbes. “How To Do A Balance Transfer In 8 Steps,” https://www.forbes.com/advisor/credit-cards/how-to-do-a-balance-transfer/. Accessed May 27, 2022.

- Investopedia. “How Credit Card Balance Transfers Work,” https://www.investopedia.com/credit-cards/balance-transfer-credit-card/. Accessed May 27, 2022.

- Experian. “How Long Does a Credit Card Balance Transfer Take?” https://www.experian.com/blogs/ask-experian/how-long-does-a-credit-card-balance-transfer-take/. Accessed May 27, 2022.

- CNBC. “5 things to do once your balance transfer is complete,” https://www.cnbc.com/select/what-to-do-once-your-balance-transfer-is-complete/. Accessed May 27, 2022.

- MyFICO. “Credit Checks: What are credit inquiries and how do they affect your FICO® Score?” https://www.myfico.com/credit-education/credit-reports/credit-checks-and-inquiries. Accessed May 27, 2022.

- MyFICO. “What is the Length of Your Credit History?” https://www.myfico.com/credit-education/credit-scores/length-of-credit-history. Accessed May 27, 2022.

- Experian. “How a Balance Transfer Affects Your Credit Score” https://www.experian.com/blogs/ask-experian/how-a-balance-transfer-affects-your-credit-score/#:~:text=A%20balance%20transfer%20can%20be,inquiries%20on%20your%20credit%20report. Accessed May 27, 2022.

- CNBC. “Is a credit card balance transfer fee worth paying?” https://www.cnbc.com/select/is-a-balance-transfer-fee-worth-it/. Accessed May 27, 2022.

- Forbes. “Balance Transfer Calculator: How Much Can You Save With A Balance Transfer?” https://www.forbes.com/advisor/credit-cards/balance-transfer-calculator/. Accessed May 27, 2022.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).