Budgeting for Newlyweds and Printables to Help Manage Your Joint Finances

Taking your relationship to the next level brings new challenges as you deepen your connection. If you’ve recently tied the knot or plan to get married very soon, you know the importance of being open with your partner about everything. You may have already discussed buying a house or having kids, but have you talked about how to handle your money as a couple?

In 2018, the average cost of a wedding alone was $33,931 according to The Knot, so it’s no surprise that finances weigh heavily on your relationship. But with open communication and trust, you’ll understand where your partner is financially and how you can build a stronger future together.

While opposites may attract, you and your new spouse should be on the same page about budgeting. Whether you decide to combine your accounts or split everything 50/50, establishing financial trust early on will help you avoid money issues in your marriage.

Managing finances can be challenging, but with two people contributing you have more security and double the help. These printable budget templates will help you and your spouse discuss finances, set goals like building your credit and successfully budget your first year of marriage so you can enjoy the newlywed life!

Have the ‘money talk’ early and often

We found that 65% of millennials agree that talking about finances is necessary to a successful long-term relationship, however, more than half of them wait until marriage to discuss joint accounts.

Having the “Money Talk” early on in your relationship (or when you feel comfortable) can help build trust. Knowing your partner’s situation and being open about your own will improve your communication and provide accountability to make more responsible choices.

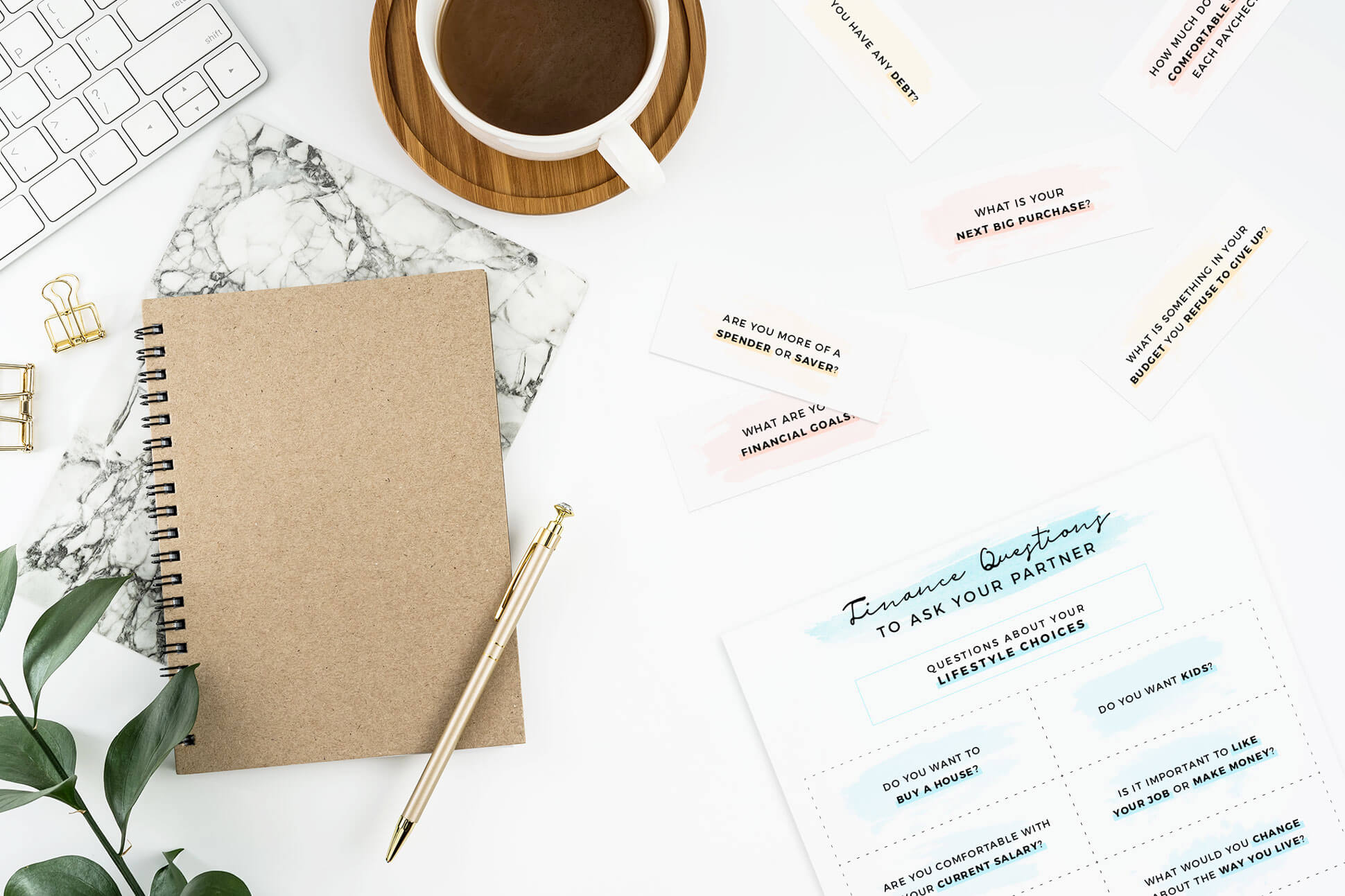

If you haven’t talked finances with your significant other or spouse, try not to put it off much longer. Use these conversation starters to help open up the discussion:

Questions about lifestyle choices

- Do you want to buy a house? Ease into the conversation by talking about upcoming purchases. If you and your partner would like to buy a home in the future, discuss plans on saving.

- Do you want kids? Hopefully, this one has come up before saying “I Do” but if not, establish whether you want kids in the future. This question also brings up thoughts on career paths, home location and saving for college.

- Are you comfortable with your current salary? Everyone would appreciate a higher salary so talk about whether your current salary allows you to just get by or if you are living comfortably.

- Is it more important to like your job or make money? At some point, you may face a career change that means making less income. Discuss what that could mean for your relationship.

- What is an ideal emergency fund amount? The difference between saving a 3 month, 6 month or 12 month rainy day fund can be huge. Talk through a savings plan that you both feel comfortable with and discuss how you would support each other.

- What would you change about the way you live? Discover if your partner wishes they could do things differently. Save more? Spend less?

Questions about your finance history

- How did your family manage money growing up? Discuss what your home life was like and how it’s shaped your current beliefs on saving and spending.

- Do you have any debt? Although this could be a sore spot, student loans and credit card debt are too common now not to bring up.

- Are you more of a spender or saver? Be honest with each other and talk about your money habits. Maybe you save conservatively but have issues with impulse buys. Let your partner know where you’re at.

- What is something in your budget you refuse to give up? This answer may change as time goes on, but it’s important to know where your priorities are. Whether it’s a personal care item or an entertainment expense, let your partner know why it’s important.

- What is your credit score? Run a credit score check and see where you’re both at (and make sure you each know how to read a credit report). No pressure, but studies have shown that couples with similar credit scores tend to form long-term, committed relationships.

- Do you have any other financial obligations? Put it all out there. Other financial obligations could be family related or include overdue bills.

Questions about the future

- What is your next big purchase? Look ahead and plan to save for the next big ticket item. Whether it’s new furniture or a new car, talk about what’s just around the corner.

- How much do you feel comfortable saving each paycheck? If your finances are more secure, try to bump up the percentage you save. You can always adjust as needed if things are too tight.

- What income level would you like to achieve? Be realistic with each other and talk about rough career plans for the next 5–10 years.

- What would we do with any unexpected income or bonuses? More money sounds like a good thing but if you and your partner aren’t on the same page about what to do with it, you may run into some tension.

- What are your financial goals? Talk about short-term and long-term goals. From building credit to retiring early, discuss what you can work toward as a couple.

- What would you like your retirement to look like? It seems far away, but the planning starts now. Discuss what age you’d like to retire, where you’d like to live, and the lifestyle you’d like to have.

Decide if combining your finances is the right move

There’s no right answer to whether or not you should combine accounts with a partner. What matters is that you have the discussion. After you get to know and understand each other's situation, talk about different options for splitting bills and expenses.

Many married couples decide to share joint accounts and split expenses 50/50 while others split up bills based on their income. Find out what works best for you and your partner by talking through these ideas:

- Talk about how to split up income. You can decide to keep your accounts separate, combine them or even set up a third communal account just for shared expenses.

- Discuss tracking your budget. Whatever you decide to do, make sure there’s a plan for tracking all of the purchases, expenses and savings since they may be in different spots.

- Should you “share” credit? There are ways to “share” credit with your spouse like opening a joint credit card. Learn more about the pros and cons of “sharing” credit to decide if it’s a step you’d like to take.

Set financial goals for your marriage

With hard work comes great success — that applies to your marriage too! Now that you’ve put a ring on it, set goals to stay on track both personally and financially. Find some time to sit down with your husband or wife and set goals for your marriage.

Financial goals work best when they are attached to a timeline and a specific number. For example, would you like to save 30% of your salary in the next year? Maybe you’d like to contribute 6% to your retirement each month. Make sure your financial goals are specific, measurable, actionable, realistic and have time restrictions (S.M.A.R.T.) so you are set up for success. Having these goals in place will make your financial decision-making easier.

Here are some ideas of financial goals to get you started:

- __Pay off X debt amount by age XX. __

- __Save X amount for a house by year XXXX. __

- Increase credit score to XXX.

- Save X amount for a vacation next year.

- Build an emergency fund by contributing X per month.

- Set aside X% each paycheck for retirement.

Plan your budget together

![]()

Once you’ve decided how to manage your money as a couple, create a plan to maintain your financial health after the honeymoon. Use the basics of budgeting to calculate your income and savings plan, while subtracting recurring expenses like rent and bills, and setting spending limits in other categories.

Make sure your budget is in line with the financial goals you set for your marriage. Use this printable budget template to plan your monthly budget.

Budgeting tips to keep in mind:

- Define “wants” and “needs. It sounds simple, but there may be some blurred lines between things you think you need. Setting boundaries will help keep your financial decisions crystal clear.

- Separate groceries from eating out. There’s a big difference between cooking at home and eating out. Keep fast food and restaurant meals separate from grocery store runs to monitor your spending in each category.

- Automate bill payments. Life gets busy so take advantage of online bill pay by setting up automatic payments for utilities, bills and recurring monthly expenses.

- Try the 30/30 rule. If you tend to impulse buy, try waiting 30 days for any purchases over $30. This will help you think about why you want (or think you need) the item in mind.

- Set aside “fun” money. Don’t be too hard on yourselves. Be realistic and set a budget for entertainment, going out with friends and date nights.

- Build up your emergency fund. Allocate a percentage of your paycheck to go toward a rainy day fund. You’d be surprised how quickly savings add up with two people contributing.

![]()

Commit to each other and your budget

Life as a newly married couple is all about discovering ways to make your marriage stronger. What works for others may not work for your individual situation, but putting your relationship first is guaranteed to build a healthy marriage.

Practice habits like being transparent in difficult situations and being flexible when things don’t go as planned. Enjoy each day with your partner and learn along the way. To build a stronger financial relationship, check in often and continue to have an open conversation about money.

This printable budget calendar will help you schedule check-ins with your spouse, document when bills are due and plan for paychecks so you can stay on track.

Enjoy the newlywed life with your partner as you take on new challenges and new adventures. Build a strong financial foundation so you can plan a life you love with the one you love.

About the author

Jeff Smith is VP of Marketing at Self.