25 Facts About Credit and Credit Scores

Credit can seem like a mystery at times. What’s the difference between a credit score and a credit report? Between a joint user and an authorized user? Is your income part of your credit report? What about your marital status?

What constitutes “good credit,” and how do you obtain it? And what role does it play in your overall personal finances?

These are just some of the questions that may come to mind as you’re seeking to qualify for a loan or credit card and get the best interest rate possible. We’ll look at 25 facts about credit and credit scores to clarify any misconceptions.

Key points

- Credit scores are complex but crucial - You have multiple credit scores calculated by different models, including FICO and VantageScore.

- Your credit impacts more than just loans - Credit scores affect interest rates you get on loans and credit cards, as well as employment opportunities.

- Credit management requires active monitoring - This includes things like on-time payments, keeping a low credit utilization, and checking your credit report for errors.

1. Good credit doesn’t guarantee your credit application will be approved

Lenders want to make sure all their bases are covered before they extend you credit. That means they may look at factors other than your credit score to determine whether to lend you money. Your employment status also can play a role: If your income is too low for the amount of credit you are seeking or you haven’t been at your current workplace long, those factors could weigh against you.

Your financial status apart from your credit score also matters. You might also be denied if you have high account balances or a high debt-to-income ratio.

2. You have different types of credit scores

“Your credit score” is a misleading phrase, because you actually have more than one. Two main credit scoring companies — FICO® and VantageScore — use different models to determine their version of your credit score, although both use a scale that ranges from 300 to 850. Different lenders may use custom scoring models to compile their own credit scores.

You can’t account for every possible variation, but you can home in on the most important factors, and there is a good deal of commonality between the two systems.

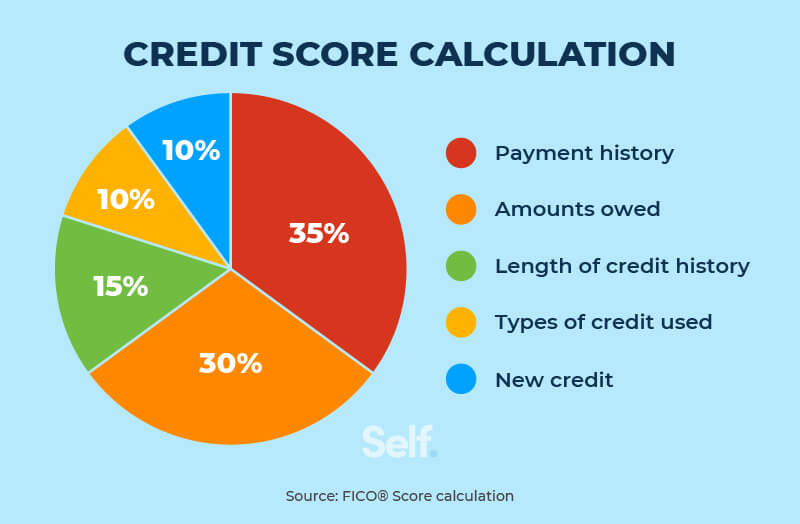

3. A FICO credit score is calculated by five factors

Your credit score is determined using five factors, which are weighted according to their importance under the scoring system being used.

Under the FICO system, the most important element is your payment history, which accounts for 35% of the total.

That’s followed by the amount you owe, which is a bit more complicated than a single figure. What’s really being evaluated is your credit utilization ratio, which is the total amount you owe on your credit cards divided by your credit limit total for those cards. Credit utilization accounts for 30% of your FICO score.

Other factors weigh less heavily. The length of your credit history counts for 15% of your total score with FICO, while the amount of new credit you have and your credit mix each count for 10%. [1]

4. You can dispute items on your credit reports

If you see an error or something you don’t recognize on your credit report, you can dispute it with either the lender or the credit bureaus. (There are three major credit bureaus that compile your credit history: Equifax, Experian and TransUnion.)

Errors can come in a variety of forms. You may not have been credited for a payment you made. A debt might be listed more than once, or your balance might be wrong.

Identity issues can occur because of problems like sharing a similar name with someone else, or they might be the result of fraud.

If you find an error on your credit report, you can contact the credit bureaus online or by mail. More information is available from the Federal Trade Commission and the Consumer Financial Protection Bureau.

5. Credit scoring models differ from country to country

Lenders in different countries have different ways of assessing creditworthiness. For instance, Australia has four reporting bureaus: Equifax, Experian, Dun and Bradstreet, and the Tasmanian Collection Service, while the Netherlands uses Krediet Registratie. India uses Credit Bureau Information India (CIBIL), a TransUnion partner. [2]

Scoring systems may be different, too, for example Canada uses a slightly broader scoring range (maximum of 900) than what’s used in the U.S. (maximum of 850). [2]

6. Keeping old credit cards open can positively impact your credit score

As long as you make your payments on time, there’s not really a downside to keeping an old credit card open. You can build credit by lengthening and improving your credit history.

Keeping a card with a low or no balance can also help your credit by improving your credit utilization ratio (CUR). If you close a card with a low balance, that may hurt your CUR — especially if you have high balances on your other cards. For example, if you have a $50 balance on a $1,000 card, that’s a 5% utilization ratio that can bring down your overall CUR.

Some experts say it’s important to keep it under 30%, and that under 10% is optimal; however, there is no set figure where your credit utilization will start to impact your score, and it depends on other factors as well. [3]

7. Potential employers are allowed to check your credit

Employers are allowed to look at your credit history by running a credit check — with your permission. The rationale? They may see your ability to manage your credit responsibly as a reflection on your overall management skills.

And yes, an employer is allowed to reject your job application on the basis of your credit report. They do, however, need to give you time to dispute any errors you discover in the report.[4]

The good news is that a credit check run by a potential employer won’t affect your credit. It counts as a soft inquiry or “soft pull” on your credit, which isn’t reflected in your credit score. A hard inquiry you make yourself (by applying for credit, such as a new credit card) may shave a few points off your score. [4]

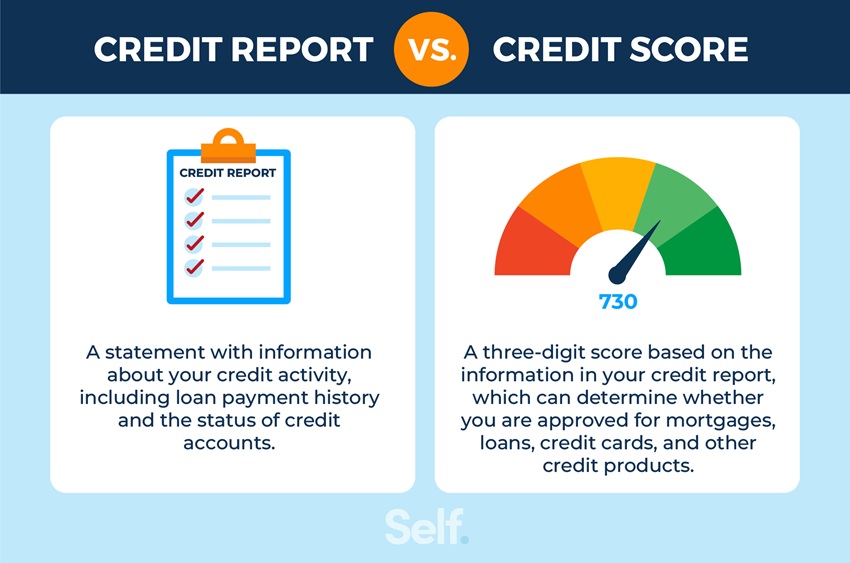

8. Credit reports and credit scores are not the same thing

Your credit report is a record of your credit history, your activity in seeking and using credit, and the current status of your accounts. Credit reports are compiled by credit reporting bureaus. Credit scores, on the other hand, are numerical values calculated based on the information in your credit report.[5]

9. You need a credit report before a credit score is determined

You don’t get assigned a credit score when you’re born or when you turn 18. Your credit score is based on what’s in your credit report, so you don’t have one until you start to build credit. You can do so by establishing a line of credit with a credit card company, getting a loan, or even renting your own place and paying utility bills: Utility bills appear on your credit report if they are delinquent and referred to a collection agency, but paid utility bills are not automatically reported to the credit bureaus. There are many services that can help you report your rent and utility payments to the credit bureaus. One example is Self’s Rent and Bills Reporting tool, which reports your rent, utilities and cell phone payments to the credit bureaus to help build your score. Rent payments will be reported to all three credit bureaus, and phone and utility bill payments will be reported to TransUnion.

10. Having a higher credit score may result in lower interest rates

A good credit score can show a lender you are responsible with your credit, and you regularly make payments on time.

FICO divides credit scores into five score ranges: Exceptional (800 or more), Very Good (740 to 799), Good (670 to 739), Fair (580 to 669) and Poor (anything below 580).

The higher your score, the more likely lenders will be to take a chance on extending you credit and the lower your interest rate will likely be.

Interest rates vary from one lender to another, but you can save thousands of dollars over a period of years in saved interest — especially on a high-dollar loan like a home loan — with good or excellent credit.

11. Exceeding your credit limit can impact your credit score

Credit utilization is an important factor in determining your credit score, so going over your credit limit can hurt your credit score. (If one of your cards is maxed out at 100%, that’s likely to hurt your CUR). When credit utilization exceeds roughly 30%, the impact on your FICO and VantageScore can become more pronounced. Typically, the lower your credit utilization ratio, the better.[6]

If you have authorized overdrafts on your account, overdraft fees can be another negative consequence of going over your credit limit. These fees can be up to $25 the first time you exceed your credit limit, and can be up to $35 if you exceed the limit twice in six months. An overdraft fee can’t be more than the amount you have gone over your limit. So, if you’re $10 over the limit, you can’t be charged a fee of more than $10.

If you don’t opt into overdrafts and their related fees, any payments that go over your limit will typically be declined, and federal law forbids you from being charged any related overdraft fees.[7]

12. Lenders and creditors decide your creditworthiness, not the credit bureaus

Lenders are under no obligation to approve a loan or line of credit, regardless of what your credit history shows. The role of the credit bureaus’ is to provide detailed information about your borrowing and credit payment history which helps lenders and creditors to assess your creditworthiness. It’s entirely up to prospective lenders to determine whether they believe you’re at risk of defaulting on your debt.

13. Your relationship status doesn’t impact your credit

Your marital status isn’t included in your credit reports, and neither is your spouse's identity — as long as accounts are held separately. Joint loans or credit cards will appear on both spouses’ credit reports. It’s not the status of your relationship that affects your credit, but the status of any jointly held accounts.[8]

14. Your income doesn’t impact your credit score

Your credit score is based only on what’s in your credit report including your record of paying off debts. Your income may well affect your ability to meet your credit obligations, but it has no direct impact on your credit score. As long as you make your payments on time, your income level—whether minimum wage or six figures—does not affect your credit score.

15. You can become an authorized user on someone’s credit card account to build credit

Becoming an authorized user on someone else’s credit card means that their account will be listed on your credit report.

A 2018 study showed that someone with fair credit could improve their credit score by 12.5% in six months or 20% in a year by becoming an authorized user on someone else’s card. Someone with poor credit could improve their score by 18.1% in six months and 28% in a year. Impacts were smaller for authorized users with better credit.[9]

Remember that your use of the credit card will go on their credit report, too, so you’ll want to be clear with the cardholder about what their expectations are.

16. You can freeze your credit to prevent identity theft

You can place a freeze on your credit report for free by contacting the credit bureaus either online, by phone, or by mail. If you put a freeze on your credit report, lenders won’t be able to see it, so they aren’t likely to approve any fraudulent requests for credit.

Once you request a freeze online or by phone, it will take effect the next business day. If you request one by mail, it will take three business days from the time the credit bureau receives your request.[10]

17. Most lenders use FICO scores to make decisions

According to FICO, they are by far the most widely used scoring system, and they state that more than 90% of top lenders use it when making decisions about loans.[11] Each lender decides when to upgrade to newer scoring versions, or may choose not change versions at all; this is why some lenders use different score versions. For instance, FICO Scores 8 and 9 are the most commonly used scoring versions among the three credit bureaus.

18. Late payments remain on your credit report even after paying off the debt

Late payments, like most other negative information, stay on your credit report for seven years. This is true regardless of whether you’ve since paid off the debt. But the more time that passes, the less that late payment will affect lending decisions.

If you make consistent on-time payments, those will help your credit score rebound, while the impact of old delinquent payments is reduced. [13]

19. Negative credit items fall off of your credit report after a certain amount of time

Bad credit isn’t forever, but negative information does stay on your credit report for a period of time. Late payments fall off your credit report after seven years, and so do most other negative marks. Bankruptcies can stay on your credit report for as long as 10 years, depending on the type, and closed paid accounts can stay there for 10 years, too.[13]

A hard inquiry stays on your credit report for two years and will only affect your credit score for one year.[14]

20. Checking your credit score won’t damage your score

Checking your credit score or looking at your credit report won’t damage your credit, and your score won’t change. When you check your own credit score, it is known as a soft inquiry, which doesn’t impact your credit score. On the other hand, if you apply for a credit card or loan, a lender will evaluate your credit, resulting in a hard inquiry. Hard inquiries generally have a small impact on your FICO® Scores and, for most people, one additional credit inquiry will take fewer than five points off your score. The good news is that FICO® Scores only review the most recent 12 months of inquiries when calculating your score.[14]

21. Each week, you can check your credit report for free

Under federal law, you’re entitled to receive a free credit report every year from each of the three credit bureaus. You can order a copy weekly online at annualcreditreport.com. It’s a good idea to check your credit report for accuracy to make sure you don’t see any errors you may wish to dispute or signs of fraud like accounts you did not sign-up for.

22. You can still get a loan with bad credit

You can get a loan with bad credit, but you’re likely to pay a higher origination fee and a steeper interest rate. Some lenders won’t offer loans to people with bad credit, but other companies make a business of it. It’s a good idea to be cautious about predatory lenders and high-interest businesses such as payday loans and car title loans.

Both are short-term, high-interest loans. With car title loans, the borrower turns over title to the vehicle as collateral — which you won’t get back until you repay what you borrowed, plus the lender’s finance charge and any additional fees.[15]

23. Credit isn’t the only deciding factor in lending decisions

While things such as your income and assets don’t affect your credit report, they still can affect a lender’s decision on whether to lend you money. Your employment status and history can be a factor, as well. A mortgage lender, for example, will want to see your savings account balance, total assets, and current income in addition to your credit report in determining whether to approve you for a loan, and if so, for how much.[16]

24. You can spot fraud by periodically checking your credit

A check of your credit report can reveal red flags that could indicate identity theft. If you see charges you don’t recognize from companies you don’t do business with, you might want to dispute them.

You also might find errors in your Social Security number and other personal information.

These may be simple errors, or they may be an indication of fraud or identity theft.

Regardless, they can affect your credit score. One Consumer Reports study found that 44% of consumers found at least one error on their credit report, and 34% found errors relating to their personal information.[17]

25. Activity from a joint account impacts your credit score

It doesn’t matter which cardholder makes charges to a joint account or whose checking account is the source of payments. Both users will have their credit score affected by the charges, payments, and the credit utilization level of the card. A joint user is different from an authorized user in that a joint user is responsible for repaying the debt, however not many companies offer joint credit cards. [18]

Moving forward

There’s a lot to know about your credit and how it affects your financial life, but you don’t need an army of calculators to know where you stand. With a free copy of your credit report and an understanding of the principles we’ve discussed here, credit won’t be a mystery anymore, but rather an asset you can use to your advantage.

*Results vary. You may not receive an improved credit score. Not all lenders use scores impacted by rent/utility payments.

Sources

- MyFICO, “How Are FICO Scores Calculated?” https://www.myfico.com/credit-education/whats-in-your-credit-score Accessed September 25, 2025

- CNBC. “Is the U.S. the only country with credit scores?” https://www.cnbc.com/select/is-the-us-the-only-country-with-credit-scores. Accessed October 7, 2021.

- Experian, “What is Credit Utilization Rate?” https://www.experian.com/blogs/ask-experian/credit-education/score-basics/credit-utilization-rate/ Accessed September 25, 2025

- Experian, “Why Employers Check Your Credit Report and What They See” https://www.experian.com/blogs/ask-experian/why-employers-check-your-credit-report-and-what-they-see/ Accessed September 25, 2025

- Consumer Financial Protection Bureau. “What is the difference between a credit report and a credit score?” https://www.consumerfinance.gov/ask-cfpb/what-is-the-difference-between-a-credit-report-and-a-credit-score-en-2069. Accessed October 7, 2021.

- Experian. “Does Going Over My Credit Limit Affect My Credit Score?” https://www.experian.com/blogs/ask-experian/does-going-over-my-credit-limit-affect-my-credit-score. Accessed October 7, 2021.

- CNBC. "What happens if you try to spend more than your credit limit," https://www.cnbc.com/select/exceeding-credit-limit/. Accessed October 21, 2021.

- Equifax, “Myths Vs Facts: Marriage and Credit” https://www.equifax.com/personal/education/life-stages/articles/-/learn/myths-vs-facts-marriage-and-credit/ Accessed September 25, 2025

- CNBC. “Does being an authorized user on someone else’s credit card actually build your credit score?” https://www.cnbc.com/select/does-being-an-authorized-user-affect-your-credit-score. Accessed October 7, 2021.

- USA.gov. “Credit Reports and Scores,” https://www.usa.gov/credit-freeze . Accessed September 25, 2025

- MyFico. “What is a FICO® Score?” https://www.myfico.com/credit-education/what-is-a-fico-score. Accessed October 7, 2021.

- MyFico. “FICO® Scores Versions,” https://www.myfico.com/credit-education/credit-scores/fico-score-versions. Accessed October 21, 2021.

- Equifax. “How Long Does Information Stay on My Equifax Credit Report?” https://www.equifax.com/personal/education/credit/report/articles/-/learn/how-long-does-information-stay-on-credit-report/ Accessed September 25, 2025

- MyFico. “Credit Checks: What are credit inquiries and how do they affect your FICO® Score?” https://www.myfico.com/credit-education/credit-reports/credit-checks-and-inquiries. Accessed October 21, 2021.

- Federal Trade Commission. “What To Know About Payday and Car Title Loans,” https://www.consumer.ftc.gov/articles/what-know-about-payday-and-car-title-loans. Accessed October 7, 2021.

- Consumer Financial Protection Bureau. “How does my credit score affect my ability to get a mortgage loan?” https://www.consumerfinance.gov/ask-cfpb/how-does-my-credit-score-affect-my-ability-to-get-a-mortgage-loan-en-319. Accessed October 7, 2021.

- Consumer Reports, “More Than a Quarter of People Found Serious Mistakes in Their Credit Reports” https://www.consumerreports.org/money/credit-scores-reports/serious-mistakes-found-in-credit-reports-a1061511185/ Accessed October 7, 2025.

- NerdWallet, “Considering a Joint Credit Card? Here’s What to Keep in Mind” https://www.nerdwallet.com/article/credit-cards/opening-joint-credit-card-account Accessed October 7, 2025

About the reviewer

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.