The Most Common Unexpected Expenses and How To Prepare For Them

We’re told to expect the unexpected. But dealing with the unexpected can be scary, and nobody likes unpleasant surprises, especially when they include unanticipated costs. Understanding what types of unexpected expenses might occur can help you develop a plan so that you’re prepared if they occur.

This article will help identify some common causes of unexpected expenses and create strategies to handle them successfully if and when they occur.

What is an unexpected expense?

An unexpected expense is one you can’t have foreseen. If you’re renting a home from a landlord who decides to sell, forcing you to move out when you weren’t planning to do so, the resulting costs such as moving expenses and the security deposit on a new place would count as unexpected expenses.

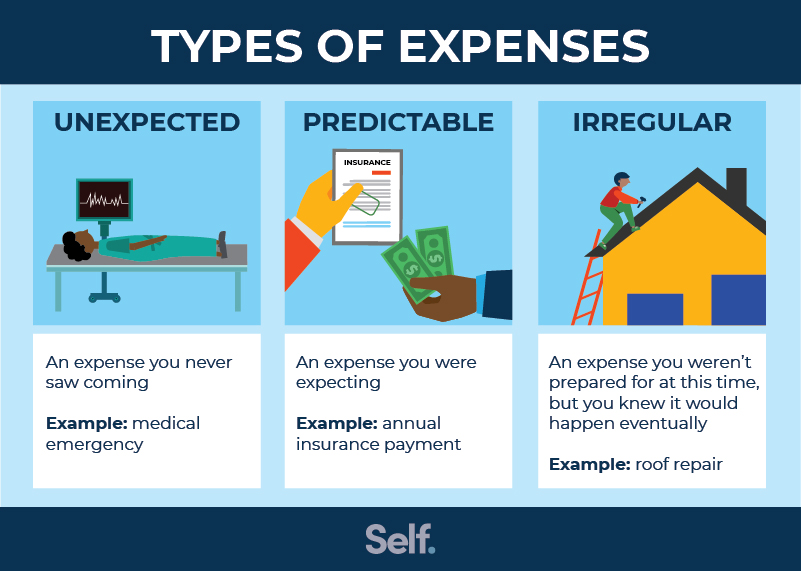

Unexpected expenses differ from two other categories: predictable expenses and irregular expenses, which we’ll look at next.

What is a predictable expense?

A predictable expense is one you not only know will happen, but also you know when it will happen. Most Americans plan for monthly expenses such as rent or a mortgage, a car payment, utility bills, phone bills and so forth by building them into their monthly budget.

But it’s easy to overlook other predictable expenses that happen less frequently, such as property taxes, car registration fees and annual or bi-annual car insurance payments. Costs such as annual medical, dental and eye exams fall into this category, too, along with school tuition and regular car maintenance such as oil changes and tuneups.

What is an irregular expense?

An irregular expense is an expense that you can predict will happen at some point — but you may not know when.

You can be pretty sure that, at some point, your dishwasher is going to break down, your car will need to be replaced, you’ll need a new HVAC unit or you’ll have a plumbing problem. But there isn’t a specific timeline when these expenses will occur.

Examples of unexpected expenses

Unexpected expenses can fall into several categories including home, car, and medical expenses. They can even involve gifts for special occasions, such as weddings.

1. Auto expenses

We aren’t talking about car payments or insurance costs. Those are predictable. What’s unexpected is a punctured tire or a car accident that leaves you with towing fees, costs of repairs not covered by your insurance, and an increase in your insurance premiums after the fact.

The average cost of a tow is around $109, depending on how far your car needs to go and the tow company’s rates, which can be anywhere in a general range of $2.50 to $7 a mile.[1] When it comes to repairs, you can pay $500 for brakes, between $400 and $900 for a timing belt, and $400 to $600 for a new starter.[2]

Less serious but also unexpected is a pebble in the road that gets kicked up into your windshield and creates a crack, forcing you to replace the glass, which can range anywhere from $100 to $400.[3] Weather damage (imagine if a tree falls on your car), vandalism, speeding and parking tickets, and the cost of getting your car out of impound if it’s towed are other examples of unexpected emergency expenses.

2. Home repair expenses

Several kinds of major home repairs can fall into the category of unexpected expenses.

If you’re lucky, you’ll never need to repair foundation damage to your home, but if the situation arises, it can cost between roughly $1,800 and $6,500.[4] Other unexpected home expenses might include remediating mold damage (at an average cost of more than $2,200); grading or ponding issues, which can cost up to almost $3,000; and replacing your water line to the street (up to nearly $2,500) or your septic system, which can run you between $3,100 and almost $9,400.[4]

You can prepare for these expenses by building an emergency fund. Homeowner’s insurance can be worthwhile because it can mitigate the cost of major repairs you may not be able to cover, converting some of that cost into the predictable expense of regular payments.

3. Medical expenses

On top of the deductibles and copays, there are unexpected expenses your insurance may not cover at all.

Surprise billing for medical treatment and procedures that aren’t covered by your insurance is common, with about 20% of hospital bills including surprise charges.[5] If your insurance requires that you be treated within a certain network to receive full coverage, you may face extra charges if an ambulance takes you to an out-of-network hospital.

Individual providers may be outside your network, too, which can add to your costs.

According to the Federal Reserve, 22% of adults incurred unexpected medical expenses in 2019, with the median expense falling between $1,000 and $1,999.[6] That’s not to mention unexpected medical bills for kids, such as a tonsillectomy, or for your pets if they develop serious conditions.

The average ER visit for infants and children younger than 18 cost $796 in 2019.[7] When it comes to unexpected veterinary care for cats and dogs, according to Petplan, the average cost in 2018 was between $800 and $1,500.[8]

You can help reduce the chances of incurring unexpected costs by seeing your medical provider regularly and addressing issues before they develop into more costly conditions. Wellness plans that include a good diet, exercise and adequate sleep also help.

4. Unplanned travel and event expenses

Unplanned travel can create unexpected costs, too. It can occur if you need to attend a funeral or if you need to travel for a wedding.

Beyond airfare (if you’re flying) or gas costs if you’re traveling by car, you may need to factor in costs like hotel rooms and parking, rental cars, fees for baggage on flights, etc.

Comparing different airlines’ policies and charges can also help you save money: Some charge for a carry-on bag, while others don’t. Compare lodging amenities and costs and decide what you really need and what you can take a pass on.

How to plan for unexpected expenses

In order to plan for unexpected expenses, it’s a good idea to have at least three to six months of living costs saved in an emergency fund — and ideally, one year.

Set up an emergency savings fund account

A good first step is to set up an emergency savings fund for that proverbial rainy day. You can start by setting a goal for a specific amount of money you want to save over the next year. Then create a plan for how to get there. Evaluate your budget and cut out unnecessary daily spending. Evaluate everything from impulse fast-food buys to streaming service subscriptions.

Even if you save just $10 a week, that can add up to $520 in a year’s time, which may be enough to cover the average cost of an urgent care or emergency room visit.

Evaluate your insurance coverage

Consider taking a look at your insurance plan. Are you paying too much? Too little? Do you have the right kind of coverage? When it comes to medical coverage, it’s not a bad idea to think about your risk factors when deciding what level of insurance you need, taking into account previous diagnoses and genetic risk factors (what runs in your family).

When it comes to car insurance, measure deductibles against monthly payments and decide what you can afford. You may want to ask yourself whether you would be able to afford out-of-pocket car repair costs if you choose a high deductible, for example. You might want more expensive collision coverage for a new car than for an old clunker.

You can call your insurance company and find out if you are eligible for any discounts. For example, if you take part in a defensive driving course, are a student, have multiple vehicles, are a good driver, or are part of certain organizations, like AAA, you can qualify for discounts that will bring your premium cost down.

There are several different kinds of auto insurance to think about: comprehensive, liability, uninsured motorist, collision, personal injury, medical payments, etc.[9] Some may overlap with other kinds of coverage, such as health insurance, so it’s worthwhile to consider that as well, so you’re not paying twice.

Track your spending

It’s always a good idea to know where your money is going. Why not take a look at your expenses over the past year and take note of where you might have saved? If you’re still spending money on those things, remove them from your budget.

You can use budgeting apps to help you track expenses; some will even cancel unused subscriptions for you. You may have signed up for free trials you’ve forgotten about, only to find they have been converted into automatic payment plans without you realizing it.

Online banking has made it easier than ever to check your accounts whenever you want from a mobile device or computer, without waiting for a monthly statement. On top of that, some banks offer you incentives for going paperless.

As you go over your expenses, it can help to take note of any that you’ve overlooked — everything from new tires to school supplies — and write them down; then, add them all up and divide by 12 to get your monthly costs.

Once you’ve done that, you can deal with how much you’ve paid for truly unforeseen expenses. That’s where your emergency fund comes in. It’s for things you really need and can’t put off, not for optional expenses that might make life a little easier or more convenient. The expense should be both urgent and absolutely essential to qualify.

Budget with all expenses in mind

It’s easy, and common, to plan only for day-to-day expenses, especially if you are living paycheck-to-paycheck. But it’s important to your financial health to take all different kinds of potential expenses into account when creating a budget. You may be able to pay for all your daily needs now, but if you don’t have an emergency fund, a big unexpected expense can jeopardize your ability to do so in the future.

That’s why it is important to account for predictable, irregular and unexpected expenses in your budget.

Next steps

Being prepared for unexpected expenses and one-time hits to your budget you can’t have foreseen doesn’t require a crystal ball. You don’t need to know where or when crises will occur, or even what they are, to protect your personal finances and safeguard your financial goals.

Things like a sound savings plan and adequate insurance can help you keep meeting your short-term goals even if you are challenged by sudden, unexpected expenses.

Sources

- J.D. Power. “How Much Does It Cost To Tow A Car?” https://www.jdpower.com/cars/shopping-guides/how-much-does-it-cost-to-tow-a-car. Accessed January 5, 2022.

- AAA. “Planning For Auto Maintenance And Repair Costs,” https://www.aaa.com/autorepair/articles/planning-for-auto-maintenance-and-repair-costs. Accessed January 5, 2022.

- Glass America. “How Much Does It Cost To Replace a Windshield Without Insurance?” https://glassusa.com/blog/how-much-does-it-cost-to-replace-a-windshield-without-insurance/. Accessed January 6, 2022.

- Million Acres: A Motley Fool Service. “7 Expensive Home Repairs You Need to Be Aware of,” https://www.millionacres.com/real-estate-investing/articles/7-expensive-home-repairs-you-need-be-aware/. Accessed December 29, 2021.

- WebMD. “Surprise Billing,” https://www.webmd.com/health-insurance/features/surprise-billing. Accessed December 29, 2021.

- Federal Reserve. “Report on the Economic Well-Being of U.S. Households in 2019, Featuring Supplemental Data from April 2020,” https://www.federalreserve.gov/publications/files/2019-report-economic-well-being-us-households-202005.pdf. Accessed December 29, 2021.

- Consumer Health Ratings. “Emergency Room - Typical Average Cost of Hospital ED Visit,” https://consumerhealthratings.com/healthcare_category/emergency-room-typical-average-cost-of-hospital-ed-visit/. Accessed January 5, 2022.

- CNBC. “Are you prepared for a pet emergency? Most Americans are not,” https://www.cnbc.com/2018/06/14/are-you-prepared-for-a-pet-emergency-most-americans-are-not.html. Accessed January 5, 2022.

- Car and Driver. “What Are The Different Types of Car Insurance?” https://www.caranddriver.com/car-insurance/a36367346/types-of-car-insurance/. Accessed December 29, 2021.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.