Hi.

We're Self.

We're here to help you build credit and savings and reach your financial goals.

It all started with some missed payments.

Self began in 2015 after a mistake with Founder James Garvey’s credit card that tanked his credit score. Looking for a way to rebuild his credit, James saw the challenges faced by millions of Americans with low or no credit.

Traditionally, to get credit, you needed credit. It’s a catch-22, and the system was set up against many of us. So Self created tools that work regardless of credit history or bank balance.

Today, Self continues to innovate — making credit building more accessible for everyone.

Our Builders put it best — take it from Khyri R.

“This has been a HUGE help in starting my credit journey. Has opened up a lot of doors for me. Has benefited me immensely as a young man just getting my own taste of life. Grateful to Self for helping start it.”

4 Million Builders served, and counting.

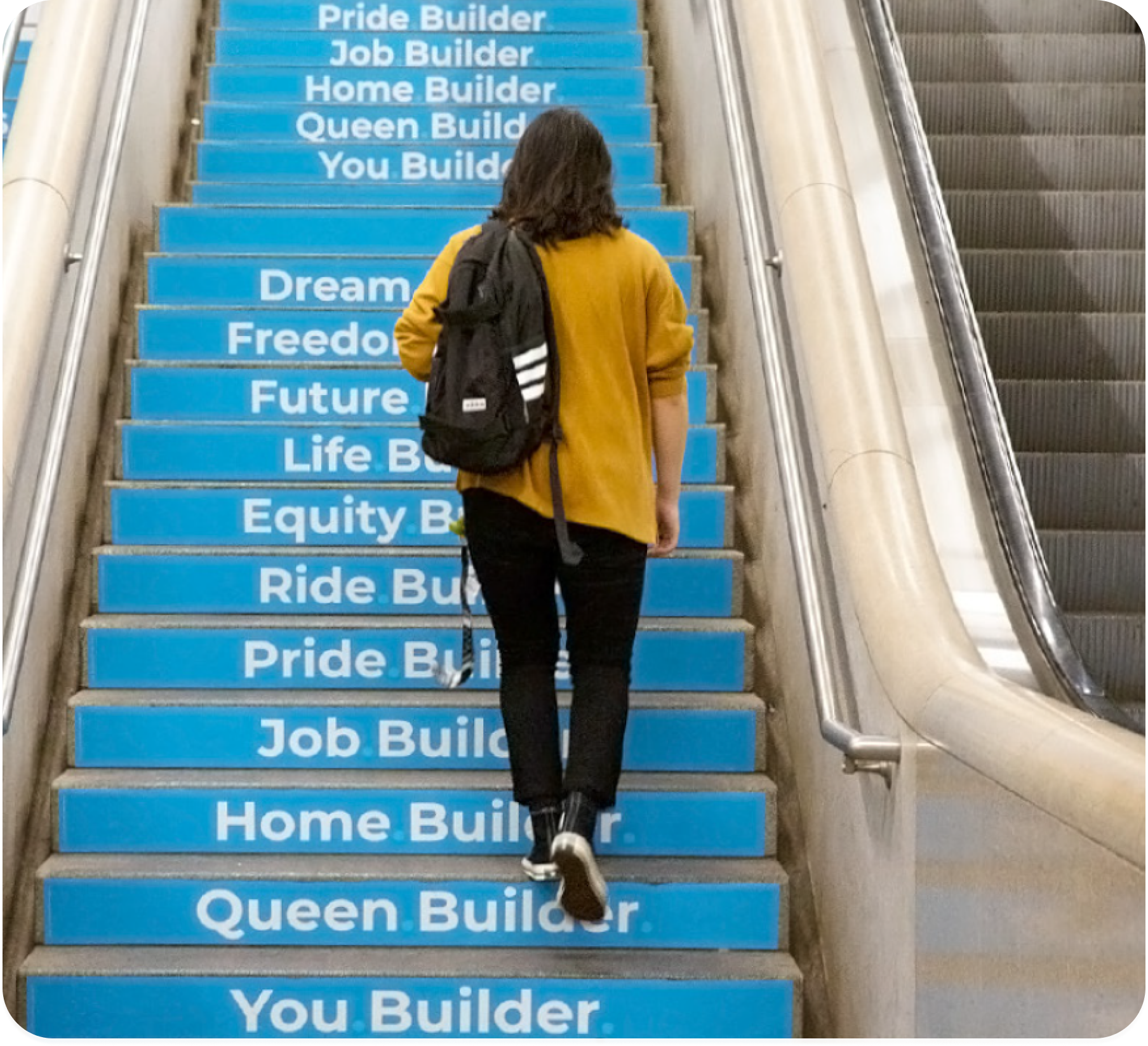

Better credit can open the door to achieving other goals. So whether you're simply a Credit Builder, or you’re set on becoming a Home Builder, a Car Builder, or a Life Builder, Self is here to help you make it possible.

Get SelfIndividual results vary. The ability to obtain a loan/mortgage may be dependent on a number of factors. Credit score is only one of those factors.

Meet the Self Team. We’re Builders, too.

From engineering to customer success, we are always looking for new, different skill sets with diverse backgrounds to expand the scope of the good our company can do. Join us.

View careersWe’re committed to DEI.

We strive for a work environment where every individual is seen and heard. Our Diversity, Equity, and Inclusion program and Employee Resource Groups enhance the contribution of all, making Self a better place to work.

Our core values

Be Your Authentic Self

- We value who you are and the path you've taken to get here.

- We value diversity and diverse perspectives.

- We treat people with respect for who they are.

We're Better Together

- Collaborate to meet our goals.

- Getting it right is better than being right.

- Assume positive intent.

- Be humble and kind.

- Work hard and have fun.

Own and Deliver

- Each of us is responsible for our words, our actions, and our results.

- See it through.

- Think of tomorrow, today.

Do the Right Thing

- Our business is complex; take the time to know the rules and live them.

- Speak up: see it, say it.

- Lead by example.

Builders First

- We create products that support our customers in achieving their long term financial goals.

- We provide customer service with empathy and respect.

Transparency Matters

- We maintain clear and open lines of communication.

- Mistakes happen; what matters is how we respond to them.