Why Is CREDCO On Your Credit Report & Can You Remove It?

You may be wondering why CREDCO has shown up on your credit report (and if you can remove it). It may have popped up because you recently applied for a mortgage, auto loan, or another type of credit and the lender accessed your credit report through Credco.

In this guide, we explain what Credco is, how it appeared on your credit report, what kind of company Credco is, and how you may be able to remove it from your credit report.

Key points

- Credco is a reseller of consumer credit information owned by Cotality, supplying lenders with merged credit reports that combine data from all three nationwide credit bureaus.

- Credco can also appear on your credit report when a lender performs a soft credit pull, which does not affect your credit scores.

- You can only remove Credco from your credit report if the information is inaccurate or fraudulent, as legitimate inquiries from authorized applications cannot be removed.

What is Credco?

Credco is an indirect wholly-owned subsidiary of Cotality (formerly CoreLogic), which is a leading provider of merged credit reporting services.[1] Credco is a reseller of consumer reports and other information to its clients, which consist of banks, mortgage companies, and other lending institutions. Additionally, Credco provides identity verification products and compliance solutions.[2]

In March 2025, CoreLogic rebranded to Cotality, but the Credco division continues to operate under the Credco name.

Credco specializes in its merged credit reports, which means they merge the data from each credit reporting agency (Experian, Equifax, and TransUnion) into one consumer credit report. When conducting a credit pull, lenders who want credit information from all three national credit bureaus can use Credco as a single source. Lenders use this consolidated report to evaluate everything from mortgages to auto loans to lines of credit.[2]

Contact Information:[2]

- Website: https://www.cotality.com/legal/credco-consumer-assistance

- Phone: (800) 637-2422

- Mailing address: P.O. Box 509124, San Diego, CA 92150

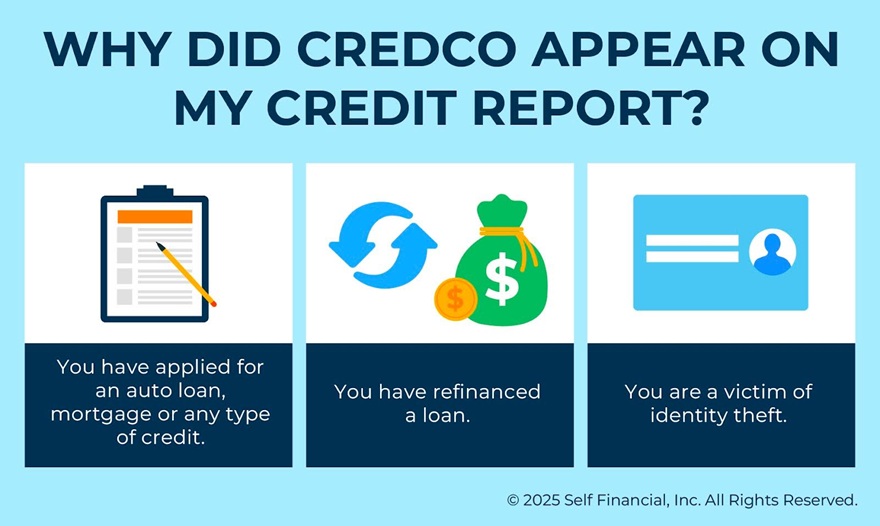

Why is Credco on your credit report?

If you are seeing Credco on your credit report, the next sections explore the different possibilities why you may have this company listed.

You have applied for an auto loan, a mortgage, or any type of credit

If you applied for a new loan, mortgage, or another type of credit that underwent a hard inquiry, you may have a Credco hard inquiry appear on your credit report. Since Credco serves as a go-between for some lenders and your credit information, you may not have been aware that Credco provided the inquiry for a lender until you see it on your report. You can contact Credco for additional information regarding which lender used its service.[2] This hard inquiry does impact your credit score temporarily.[3]

You have refinanced an existing loan

Refinancing an existing loan may be another reason you see Credco on your credit report. When you refinance or submit another application for credit, a lender may order a merged credit report through Credco, which can appear as an inquiry on your report. If you are unsure who requested it, you can review the company name listed on the inquiry and contact Credco to confirm the lender involved. [4]

You are a victim of identity theft

You could get it removed from your credit report, if you are a victim of identity theft or fraud. If you’ve never applied for new credit through which lenders used a report generated by Credco, it’s possible someone opened a credit account in your name.[5]

Is Credco a legitimate company?

Credco is a legitimate company, but it is not a consumer credit reporting agency. The company does resell your credit information as a three-bureau merged credit report to lenders. Following the Fair Credit Reporting Act (FCRA), Credco discloses your information only to lenders you have authorized to view your information for lending purposes.[2]

Can I remove Credco from my credit report?

You can only remove Credco — and anything else that shows up on your credit report — if the information is inaccurate. Unless Credco made a mistake or you can prove someone committed identity theft against you, you cannot have the item removed from your report.[6]

How to remove Credco from your credit report

If you have determined that the information on your report is inaccurate, you can take steps to remove it. These next sections explain how.

Send a dispute letter

If you believe a company or credit bureau has reported inaccurate information in your credit history, draft a dispute letter and submit it to both the company that reported it as well as the credit bureaus that list that information.[7] If the negative item was a result of fraudulent activity, this is especially important.

If you need help with this, the Consumer Finance Protection Bureau (CFPB) offers contact information, dispute forms, and letter templates. They also have guidelines on how to deal with a dispute with each credit bureau.[8]

How to check your credit report for free

To remove inaccurate information from your credit report, first determine which credit bureaus have the incorrect data — Experian, TransUnion, Equifax, or a combination of them. You can access your free weekly credit reports from all three bureaus at AnnualCreditReport.com

Sources:

- Cotality. "Meet Cotality," https://www.cotality.com/press-releases/meet-cotality. Accessed October 22, 2025.

- Cotality. “Credco Consumer Assistance.” https://www.cotality.com/legal/credco-consumer-assistance. Accessed October 23, 2025.

- myFICO. “Credit Checks: What are credit inquiries and how do they affect your FICO® Score?” https://www.myfico.com/credit-education/credit-reports/credit-checks-and-inquiries. Accessed October 8, 2022.

- Cotality. “Credco Credit Reports.” https://www.cotality.com/products/credco-credit-reports. Accessed October 23, 2025.

- TransUnion. “What to Do if You Don’t Recognize an Inquiry on your Credit Report,” https://www.transunion.com/blog/credit-advice/unrecognized-inquiry-on-credit-report. Accessed December 12th.

- MyFICO. "How to fix errors on your credit reports and how they occur," https://www.myfico.com/credit-education/credit-reports/fixing-errors. Accessed September 27, 2022.

- FTC.gov. “Credit report dispute,” https://files.consumerfinance.gov/f/documents/092016_cfpb__CreditReportingSampleLetter.pdf. Accessed October 8, 2022.

- Consumer Financial Protection Bureau. "How do I dispute an error on my credit report?" https://www.consumerfinance.gov/ask-cfpb/how-do-i-dispute-an-error-on-my-credit-report-en-314. Accessed September. 27, 2022.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).