How To Pay Your Credit Card Bill

You can choose from several different ways to pay your credit card bill, from writing a check to paying online. So the next time you get a credit card statement that indicates your statement balance and due date, select a payment option that makes sense for your situation.

If you don’t know which option works best for you, this article guides you through your options and shows you how, regardless of which payment option you use, making on-time payments helps to keep your account in good standing and build your credit.

Table of contents:

- 5 ways to pay your credit card bill

- How to automate your credit card payment

- When should you pay your credit card bill?

- How long do you have to pay your credit card bill?

- What happens if you don’t pay your credit card bill?

- What happens if you carry a balance on a credit card?

- Credit card payment tips

- Learn how credit cards work

5 ways to pay your credit card bill

As with other bills, you can pay credit card bills over the phone, by mail, or online. You can pay using cash, check, money order, or money transfer, and you can automate your payments to ensure they get there on time.

Pay over the phone

Most credit card companies let you pay your bills over the phone. You can contact the credit card issuer at the number on the back of your card and provide them with the amount of money you want to pay along with your banking information.[1] To do so, you can typically pay using your personal debit card. You will also need to provide the account number and CVV code, which is also known as the security code for them to process your payment. However, you may incur a transactional charge for using a debit card to pay.

Pay online

You can pay your credit card payments online on a computer or through a mobile banking app. Many credit card issuers offer online banking, which allows people to access their accounts electronically and pay anywhere and at any time. Similar to paying over the phone, you need your banking details to set up this payment.

Using online bill pay offers the flexibility to instantly pay your bill when your monthly payment comes due without needing to speak to someone over the phone. You can also set up automatic payments so you don’t have to worry about missing a due date.

Perform a money transfer

You can transfer money from your bank to your credit card issuers through the Automated Clearing House (ACH) network. Transfers may take several days to process but, depending on the bank, may be as quick as one to two days.[2] You typically need your bank’s routing number and account number as well as your credit card account number to set up the transfer. You can make money transfers in person or by phone, by calling the number on the back of your credit card.[1]

Pay at your credit card issuer’s bank by cash

If your credit card issuer has a financial institution branch or ATM nearby, you may be able to pay your bill in cash or with your debit card, although you may be charged a transaction fee if paying with your debit card. Check with your credit card issuer to see if that option is offered in your area and what fees you might incur.[3],[4]

Send a check

You can still pay using personal checks issued by your bank. Just fill out the name of the recipient along with the amount you’re paying, then sign and date. Checks provide a convenient way to both pay your bill and prove you’ve paid in the case of a dispute. You do, however, have to pay postage and get the check mailed on time since you can’t automate check payments. Make sure you allow enough time for mail processing so your payment doesn’t end up getting to the credit card company after the due date.

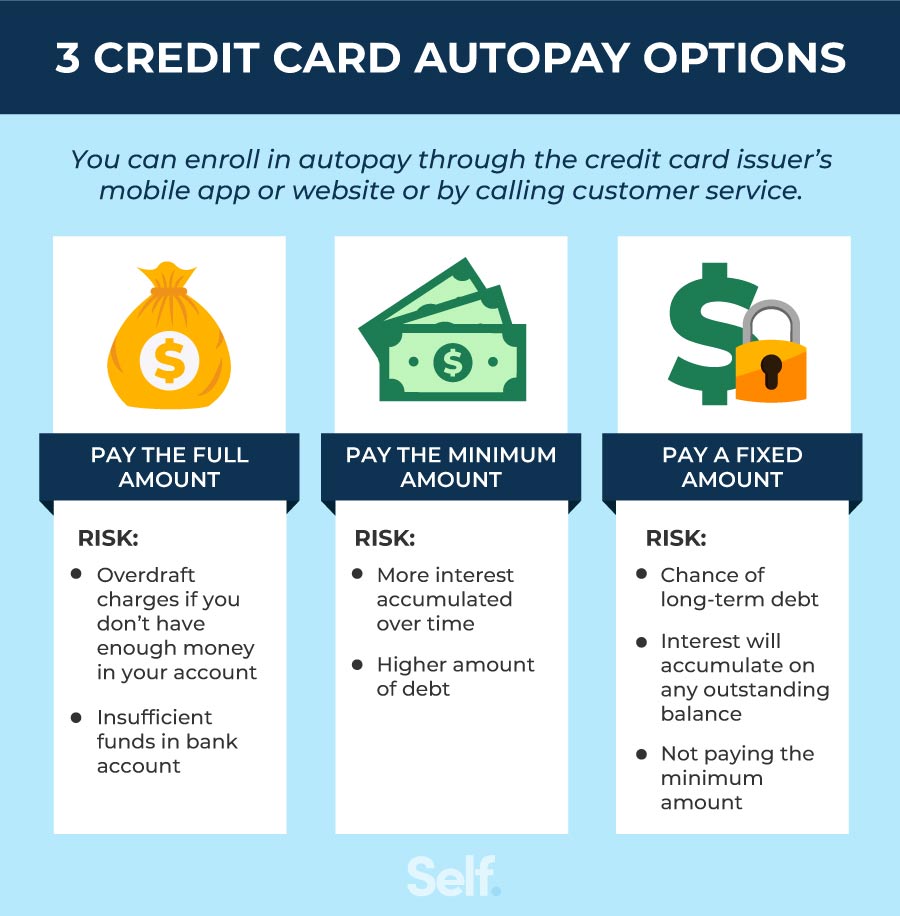

How to automate your credit card payment

You can set up automatic payments through your creditor’s website or mobile app or by calling customer service. Just use this step-by-step guide to automate your credit card payments:

- Set your payment date. Determine your credit card payment due date and set up your payment ahead of that date to ensure you’re on time.

- Select an amount to pay. Decide if you can pay the full amount, the minimum payment due, or a fixed amount each month.

- Set up the payment. Log into your account online or via mobile app to set up online payments.

- Remind yourself of due dates. Create alerts on your mobile device to let you know when a payment nears its due date so you can ensure you have enough money in your bank account to cover it.

- Create bank alerts. Set up bank alerts to notify you of low balances so you can avoid potential overdrafts. If your bank account doesn’t have sufficient funds when your automated payment is processed, your bank may pay it and charge an overdraft fee or decline the transaction altogether. If your payment gets declined due to insufficient funds, your payment will end up as a late payment.[5]

When setting up automatic payments, consider these factors as you make payment decisions:

- Set your payment date after payday, if possible, to ensure you have adequate funds in your account.

- To save on interest charges, you can pay more than the minimum amount required, if you have the money in your account to cover it.

- At least set up to pay the minimum amount so that you avoid late fees and missing your payment.[6]

When should you pay your credit card bill?

Paying your credit card statement in full and on time offers the most benefits, including:

- Carrying no balance on your credit card account helps you avoid paying interest, which adds up when it compounds.

- On-time payments can positively impact your credit score since payment history accounts for the biggest chunk of your FICO® credit score (35%).

- Depending on when the timing of when the bank reports, paying the total amount of what you owe and keeping your balance at zero may also better your credit score by keeping your credit utilization low. Credit utilization refers to the ratio of the amount you owe on your credit cards to your total credit limit, and it counts for 30% of your FICO score.

If you aren’t able pay your balance in full at one time, you may be able to make multiple payments throughout the billing period if that works for you.[7]

How long do you have to pay your credit card bill?

Credit cards give you a grace period before charging you interest on purchases as long as you don’t carry a balance. This grace period doesn’t apply to other transactions like cash advances. Your credit card agreement contains details about your grace period and what is or isn’t included.

This grace period is not an extension for your due date. In fact, if you don’t pay your balance in full by the due date, you will lose your grace period and be charged interest on your balance.[8]

What happens if you don’t pay your credit card bill?

Missing your credit card payment due date can have consequences to your finances and your credit. Your due date is different from your closing date, which is the last day of your credit card’s billing cycle. Once you reach your closing date, you still have about 21 days to pay your bill before your due date.

However, missing a credit card payment’s due date can impact you in the following financial ways:

- Your credit card company may charge a late payment fee.

- Your interest rate may rise or you could receive a penalty APR.

- Your credit score could possibly decrease.[9]

What happens if you carry a balance on a credit card?

Carrying a balance on your credit card can be expensive and can even hurt your credit. When you carry a balance on your credit card you can be impacted in the following ways:

- Potentially losing access to your credit card’s grace period

- Using too much of your available credit, which affects your credit utilization

- Accumulating interest over time that you’ll have to pay, costing you money and potentially delaying you from paying off your balance[10]

You can best resolve this by paying the balance off in full or making multiple small additional payments until it is cleared out.

Credit card payment tips

If you find credit card debt creeping up or want to avoid it altogether, you can use the following ways to manage credit card debt:

Set up automatic payments. You can set up autopay through your credit card issuer. This can be done over the phone or through the company's mobile app.

Consider changing the credit card due date. Contact your issuers and ask if you can change the due date to one that’s convenient for you. You may want to ensure that it falls after payday or, if you have several credit cards, space out when you make payments so they don’t hit all at once.

Pay more than the minimum amount. Paying only the minimum amount costs you more money because you pay interest on any remaining balance carried over from month to month.

Pay your credit card bill on time. Paying on time will help you avoid late fees, and penalties, while at the same time safeguarding your credit.

Try a debt strategy. Use one of the following debt strategies to manage credit card debt:

- Snowball method: Focus on paying the smallest debt first. Once that’s paid off, dedicate the amount you’ve been paying to the next-smallest debt. Continue this way up to the largest debt, until you pay off all your debts. This method can help motivate you to keep paying because you see progress quickly as smaller debts are paid off.

- Avalanche method: Concentrate on paying off the debt with the highest interest rate first. This way, you minimize the amount of interest you end up paying.

Use debt consolidation. Consolidating your debt might be a way to help manage credit card obligations. You can use a balance transfer to consolidate various debts into one source that’s all due at once. This simplifies your debt by consolidating different payments into one and can help you avoid missing a due date. Ideally, you’ll consolidate your debt into a loan with lower interest charges than what you’re paying now.

If you are struggling to make payments on all your credit accounts, it is important to keep in mind you should be paying more important debt first. For instance, you don't want to fall behind on your mortgage payment and risk foreclosure or fall behind on your car payment and risk repossession. If you are feeling overwhelmed by all of these payments and not sure which are most critical, you might want to consider credit counseling.

Learn how credit cards work

Understanding credit cards and how to make payments can be a bit confusing, especially if you’re just getting your first card. Even if you’ve had credit cards for a while, it can seem complicated if you find yourself juggling several payments as you try to stay current and maintain your credit.

Keeping your credit card balances paid can be easier if you take the time to understand how credit cards work and make a plan to manage your debt carefully as part of your overall budget. If you do so, you’re likely to be rewarded with greater financial security.

Sources

- CapitalOne. “How to Pay Your Credit Card Bill,” https://www.capitalone.com/learn-grow/money-management/how-to-pay-credit-card-bill/. Accessed April 28, 2022.

- Experian. “What Is the Difference Between ACH and Wire Transfer?” https://www.experian.com/blogs/ask-experian/what-is-the-difference-between-ach-and-wire-transfer/. Accessed May 4, 2022.

- Bank of America. “Credit Card Payments & Statements FAQs,” https://www.bankofamerica.com/credit-cards/credit-card-payments-statements-faq/. Accessed September 15, 2022.

- Chase. “Paying Bills at the ATM,” https://www.chase.com/digital/customer-service/helpful-tips/personal-banking/atm/pay-bills. Accessed September 15, 2022.

- CNBC. “Making on-time payments has the biggest impact on your credit score — here’s how automating them can help,” https://www.cnbc.com/select/automate-credit-card-payments/ Accessed April 28, 2022.

- Forbes. “Automatic Bill Payment: What It Is And How It Works,” https://www.forbes.com/advisor/banking/how-automatic-bill-payment-works/. Accessed April 28, 2022.

- Forbes. “When Is The Best Time To Pay My Credit Card Bill?” https://www.forbes.com/advisor/credit-cards/when-is-the-best-time-to-pay-my-credit-card-bill/. Accessed April 28, 2022.

- Consumer Financial Protection Bureau. “What is a grace period for a credit card?” https://www.consumerfinance.gov/ask-cfpb/what-is-a-grace-period-for-a-credit-card-en-47/. September 15, 2022.

- U.S. News. “What Happens When You Stop Making Credit Card Payments?” https://money.usnews.com/credit-cards/articles/what-happens-when-you-stop-making-credit-card-payments. Accessed April 29, 2022.

- Forbes. “Does Carrying A Balance On A Credit Card Hurt Your Credit Score?” https://www.forbes.com/advisor/credit-cards/carrying-credit-card-balance-hurt-credit-score/. Accessed April 29, 2022.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).