Does Debt Consolidation Hurt Your Credit?

Debt settlement companies often tout debt consolidation as a way to get out of debt, and it sounds appealing on the surface. Who wouldn’t like to replace several credit card accounts and other debts with one new account that wants just a single payment each month? It should be easier to keep track of, and that’s a big selling point.

But does consolidation really equal debt relief? Or will it wind up actually hurting your credit in the long run? To answer those questions, we'll need to take a deeper dive into debt consolidation. First, we'll look at what might make it a good — or not-so-good — idea if you're looking to establish and maintain good credit.

What is debt consolidation?

The definition is pretty simple: Debt consolidation is the process of taking out a new loan that you use to pay off all your other outstanding debts. It can be used to combine various sources of debt — such as credit cards and other high-interest debt, and perhaps student loans as well — into one monthly payment.

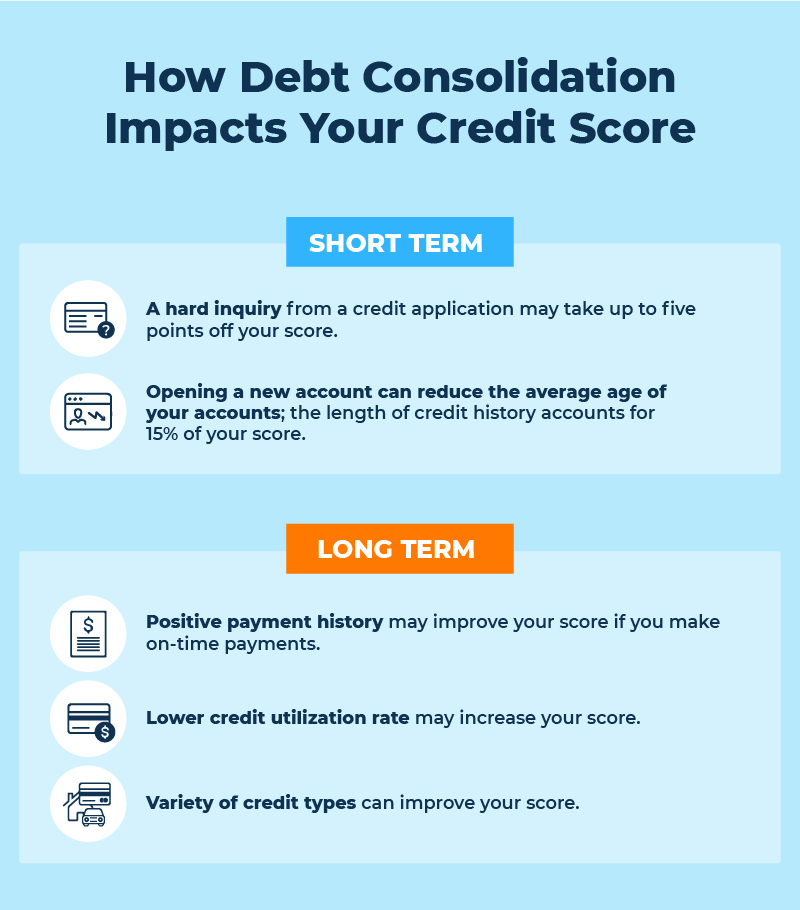

Will debt consolidation hurt my credit score?

Debt consolidation can affect your credit in different ways, depending on how you go about it. Initially, it may lower your credit score. The goal, however, is to pay down your debt more efficiently and improve your credit score in the long run.

Applying for a consolidation loan will trigger a hard inquiry on your credit report by the prospective lender to make sure you're a reasonable risk. A hard credit inquiry can cost you about five points on your credit score when the inquiry is reported to the credit bureaus. (A hard credit inquiry is sometimes called a "hard pull.")

In addition, opening up a new account reduces the average age of your accounts, which is another factor used to determine your credit score.[1] Under the FICO© system, the length of your credit history accounts for 15% of your score. A longer credit history — with older accounts in good standing — is better for your credit score.

On the other hand, under the right circumstances, debt consolidation can work to improve your credit score over the long term. It can do so by:

- Letting you improve your payment history: A history of on-time payments accounts for 35% of your FICO score, more than any other single factor. If consolidating your debt helps you make your payments on time, this will improve your credit.

- Reducing your credit utilization. A consolidation loan can be used to replace credit card loans. When you're close to maxing out your credit cards (i.e., if you have very little available credit left), your credit utilization rate is high, which can hurt your credit score. Keeping your credit utilization below 30% is a best practice. So reducing this credit card debt (and your credit utilization as a result) through a consolidation loan could help your credit score.[2]

- Improving your credit mix. A varied credit mix, or the number of different types of credit you have, also helps your credit. If you only have revolving credit (like credit cards), adding a personal loan to the mix may improve your credit score.

Common debt consolidation methods

Debt consolidation loan

A debt consolidation loan is a personal loan you can use to pay off several smaller loans. It can be used to obtain more favorable terms, such as a lower interest rate or monthly payment, on existing debt such as credit card balances or other high-interest obligations.[2]

The idea is to simplify the process and save you money by taking out the new loan at a lower interest rate. You typically disperse the funds yourself once you receive the loan, but you might be able to have it sent directly to the lenders you owe.

If you choose to pursue debt consolidation, it’s a good idea to check that the debt consolidation company is legitimate. Some scammers may tell you that they are sending money to lenders on your behalf when they are actually pocketing the funds. Check with the Better Business Bureau and online reviews to help ensure you’re dealing with a legitimate company. Also, check online ratings from reputable sources like Forbes and U.S. News, which regularly publish updated lists of the best consolidation loans.[3][4]

Balance transfer credit cards

You may have received offers for balance transfer credit cards in the mail. They’re the ones that offer you a 0% introductory rate, which continues over a given period (“six months, no interest!”).

During this time, whether it’s six months or 18 months, you don’t pay any interest on the balance you carry. This will, in theory, give you more time to pay off debt without accumulating more interest and putting yourself deeper into debt. But there are a few things you need to be aware of before taking advantage of a balance transfer offer:

- Such cards often carry balance transfer fees, which can amount to 3% to 5% of the balance you transfer.[5] The larger the balance you’re carrying on a high-interest card, the greater your incentive to switch — and the higher your balance transfer fee is likely to be. Calculate what you might save and compare it to what the fee will cost you.

- Once the introductory period is over, the interest rate may jump to a level as high or higher than the card you used the transfer to pay off. So unless you’re sure you’ll be able to pay your debt during the introductory period, it may not be worth it.

- Introductory rates, especially 0%, on transfers typically apply only to people with excellent credit. Those with poor credit may not qualify and may get charged higher introductory rates, which might negate any advantage of making a transfer and even add to the costs incurred.

- And if you're thinking of trying another balance transfer once the interest rate resets, there are reasons not to. First, your credit score will suffer each time you apply for new credit (known as a hard inquiry), and as a result, you’ll be less likely to get approved for a new loan. You’ll be seen as trying to juggle credit you can’t afford to pay.

Home equity loans

Drawing on the equity in your home can give you a sizable amount of cash you can use to pay off high-interest loans.

A home equity loan, often called a second mortgage, is money you borrow against the equity in your home. Like your initial mortgage, you pay it off over a period that ranges from 10 to 30 years. Such loans usually come with a fixed interest rate.

This shouldn’t be confused with a home equity line of credit, a revolving line of credit against which you can borrow for any purpose. First, the lender will establish a credit limit (usually no higher than 85% of the equity in your home). Then, you can borrow up to that limit initially and again if you pay a portion of it down, just as you would with a credit card.

Unlike a home equity loan, a home equity line of credit usually has a variable interest rate. That means you could end up paying more depending on the market index.

Keep in mind that with either of these options, you’re using your home as collateral. Unlike credit card debt, which is a form of unsecured debt, if you cannot handle the payments on a home equity loan or home equity line of credit, the lender can repossess your home.

401(k) or retirement loan

You may be able to borrow against your 401(k) plan if you have one through your employer; it depends on the plan.

Be sure of your job security before you think about pursuing this option because if you leave or lose your job, the entire loan is due immediately. If you can’t repay it, you’ll owe a 10% penalty on top of the balance due if you’re younger than 59½. Suppose your job isn't secure, or you don't want to feel tied to your current employer. In that case, you should think twice about borrowing against your 401(k).

There’s no similar penalty for borrowing the principal in your Roth IRA. But reducing the amount in that account will cost you not just the principal you draw upon but the interest it would accrue toward your retirement.

Debt settlement company

A debt settlement company is a business that offers to settle or renegotiate the terms of a debt you owe. Such services are often described as debt relief or debt management plans. However, these companies often charge fees and may not be able to change your loan terms at all. In fact, you may choose a specific company only to find that your creditors won’t work with the one you’ve selected.[6]

As a result, the company may resolve some but not all of your debt. So, unlike debt consolidation, where all your loans are rolled into one, debt settlement will only be a partial solution.

The company may even tell you to deposit money into a bank account that's managed by a third party, which takes it out of your hands. Such third-party accounts often carry still more fees. So by the time everything is said and done, the fees you pay may offset (or surpass) any savings you achieve using the service. As a result, you may end up deeper in debt than when you started, which can hurt your credit even more.

Another factor to consider is possible damage to your credit if a debt settlement company successfully reduces what you owe. For example, suppose the company gets a lender to agree on accepting an amount less than what you owe. In that case, it will go on your credit record as "settled for less than the full balance." This will result in a negative mark that can stay on your credit history for seven years.

Reputable debt management and credit counseling organizations are available, but they don’t work miracles. If you’re interested in going this route, check with your state attorney general’s office and the Better Business Bureau to ensure the credit counselor you’re considering is on the level.

Debt consolidation example

Suppose you have three credit cards that are close to maxed out, with interest rates around 25% and with limits of $3,000, $5,000, and $7,000. It would be to your advantage if you could get a deal on a single debt consolidation loan at 21% interest. In that case, you would reduce your interest rate, lower your credit utilization ratio, and possibly save hundreds of dollars in interest.

As long as you make your payments on time and don’t apply for any new credit, you’ll save money on this hypothetical loan and improve your credit at the same time.

If, however, you roll those same three credit card loans into a consolidated loan at 30% interest, you could be costing yourself more money.

Origination fees are worth considering, as well, as these could increase your costs. Plus, it’s possible that you may risk hurting your credit by drawing the process out longer and increasing your debt load.

But there are still factors that might weigh in favor of debt consolidation. For instance, how interest accrues is important, too. Even at a higher rate, if interest accrues monthly on a consolidated loan, you might be able to save money in comparison to credit card debt, where interest typically accrues daily. It’s helpful to look at the whole picture before making a decision.

Another easy mistake to make is taking loans with different APRs and consolidating them into a single loan. This is one reason to prioritize your debt payments.

For instance, student loans typically carry lower interest rates than credit cards or payday loans. If you’re paying 7% on your student loan and 24% on a credit card, it doesn’t make sense to roll them both into a consolidated loan at 20%. Only include loans where the interest rate is more than what you’ll be paying when you consolidate.

What are the benefits of debt consolidation?

The most obvious benefit of debt consolidation is that it can streamline your debt, making it easier to keep track of payments. And that makes it less likely you'll miss a payment.

Getting a consolidation loan with a lower interest rate than the loans you're paying off means you could pay less overall. And you may be able to pay the debt off faster.

What are the risks of debt consolidation?

Debt consolidation isn’t a magical solution to wipe away your debt. You won’t suddenly become debt-free because you refinance under a new line of credit. In fact, the opposite can happen.

When you consolidate debt, you’re not eliminating any portion of it. You’re still on the hook for the same amount; you’re just hoping for a lower interest rate that will make it easier to manage.

Just because you're putting it all in one place, that doesn't mean you'll be getting a better deal: In fact, it could make your situation worse. There's no guarantee you'll get a low interest rate, and you may even end up with a higher one — which could keep you in debt longer and further damage your credit.

Consolidation loans may contain origination fees of 1% to 5% of the loan amount, so weigh that against any savings you may achieve. In addition, some lenders charge a penalty if you pay off your loan early. Since your goal is to get out of debt, such a clause definitely will not help.

Also, you may succeed in lowering your payments at the cost of dragging your payments out longer, which may increase the balance you owe over the total length of the loan.

The bottom line

Loan consolidation can be a good way to get a handle on high-interest debt, but only under certain conditions. Make sure you aren’t drawing out the loan further or paying more overall just for the convenience of making a single monthly payment.

Before committing to loan consolidation, make sure you’re not:

- Increasing your monthly payment

- Taking on new debt that’s more burdensome than what you’re already paying

- Significantly lengthening your term of repayment

- Increasing your chances of making late payments, thereby putting your credit at risk

- Putting your home or other assets at risk through equity loans you’re not sure you can repay

If you can be confident you’re not doing any of these things, it may be helpful to pursue debt consolidation. Once you do, a good next step is to create a plan to stay out of debt once your current debt is consolidated, so you don’t find yourself back in the same position again.

Sources

- Experian. “Will Consolidating Debt Damage My Credit?” https://www.experian.com/blogs/ask-experian/will-consolidating-debt-damage-my-credit/. Accessed Aug. 2, 2021.

- Experian. “Is a Debt Consolidation Loan Right For You?” https://www.experian.com/blogs/ask-experian/is-a-debt-consolidation-loan-right-for-you/. Accessed Aug. 2, 2021.

- Forbes. “Best Debt Consolidation Loans Of October 2021,” https://www.forbes.com/advisor/personal-loans/best-debt-consolidation-loans/. Accessed Oct. 11, 2021.

- U.S. News. “Best Debt Consolidation Loans of October 2021,” https://loans.usnews.com/debt-consolidation. Accessed Oct. 11, 2021.

- Bankrate. “Balance transfer fees: What they are and how to avoid them,” https://www.bankrate.com/finance/credit-cards/what-is-a-balance-transfer-fee/. Accessed Aug. 2, 2021.

- Consumer Financial Protection Bureau. “What are debt settlement/debt relief services and should I use them?” https://www.consumerfinance.gov/ask-cfpb/what-are-debt-settlementdebt-relief-services-and-should-i-use-them-en-1457/. Accessed Aug. 2, 2021.