How to Check Your Credit Score with an ITIN Number

To check your credit information with an ITIN (Individual Taxpayer Identification Number) rather than a Social Security Number (SSN), you will need to contact one of the three major credit bureaus directly. You are unable to get your three-digit credit score or your credit report at annualcreditreport.com with an ITIN. However, you can request a free credit report from each of the three credit bureaus using an ITIN by mailing the required documents. If you’re using an SSN, you can request a free credit report at annualcreditreport.com.

You should receive a copy of your credit report after submitting the required identification information, which may differ depending on whether you choose Experian, Equifax or TransUnion.[1]

What is an ITIN number?

The Internal Revenue Service (IRS) issues ITINs to people who need a U.S. taxpayer identification number, but who do not have and cannot get a SSN. ITINs help people comply with U.S. tax laws and provide a way to file and process taxes without an SSN.

ITINs do not authorize people to work in the U.S., qualify them for Social Security benefits, or serve any purpose other than federal tax reporting.[2] While both numbers count as Taxpayer Identification Numbers for tax purposes, SSNs are issued by the Social Security Administration and ITINs are issued by the IRS.[3]

Who qualifies for an ITIN number?

An ITIN is for those that aren’t eligible for a Social Security Number but need to meet federal tax filing or obligations.

You may qualify for an ITIN if you fall into the following categories:

- A resident alien

- A non-resident alien

- Spouse or dependent of either a resident or non-resident alien

ITINs are for tax purposes and do not authorize employment or provide social security benefits, if you are unsure if you are eligible then be sure to check the official IRS guidelines.[2]

How to get your credit score with an ITIN

You may not be able to get your credit score with your ITIN but you can submit a request to the three nationwide consumer credit reporting companies by mail for your credit report.[1]

Read on for more details on how to request your credit report.

How to get your credit report with an ITIN

You can request a credit report from each credit bureau (Experian, TransUnion and Equifax) by using your ITIN. While credit reports do not typically contain your credit score, they do form the basis for calculating your credit score.

How to get your credit report from Experian

To get a copy of your credit report with an ITIN from Experian, you can submit a request with specific required information in writing.[4]

If you have an ITIN rather than an SSN, Experian will rely on other identification elements to compile your credit history. If you need help, call Experian at (888) 397-3742. Otherwise, when submitting a written request for an Experian credit report with an ITIN, you will need to provide the following information:

- Government-issued ID (like a driver’s license or state ID card)

- Copy of bank statement, utility bill or similar documentation with your name

- Your full legal name

- ITIN

- Your date of birth

- Your current address and all addresses you’ve lived at over the past two years

Mail your letter and information to:

Experian

P.O. Box 9701

Allen, TX 75013

How to get your credit report from TransUnion

You can contact the company directly by mail to request a credit report with an ITIN.[5] If you need help, call Transunion and speak to a representative at (800) 916-8800. Otherwise, just write to them asking for a free credit report and provide the following information:

- Government-issued ID (like a driver’s license or state ID card)

- Your full legal name

- Your current address

- Previous addresses in the past 2 years (if they were different to your current address)

- Social Security number (SSN) / Individual Taxpayer Identification Number (ITIN)

- Phone number

- Signature

Mail your letter and information to:

TransUnion LLC

Consumer Disclosure Center

P.O. Box 1000

Chester, PA 19016

How to get your credit report from Equifax

If you’re using an Individual Taxpayer Identification Number (ITIN), you can request your credit report by mail.[1]

To get your credit report from Equifax, mail the following address:

Annual Credit Report

P.O. Box 105281

Atlanta

GA 30348-5281

[6]

Your legal rights with credit reporting agencies

You can get a free credit report every 12 months from each of the three major credit bureaus. Since the pandemic the credit reporting agencies have been offering a free credit report on a weekly basis at annualcreditreport.com.[1] This weekly access may not apply to requests made by mail, so contact the individual credit bureaus to check how often you can request a report.

Certain specific circumstances entitle you to an additional free copy of your credit report, such as:[7] [8]

- Your information is inaccurate due to fraud: If you believe your credit file contains inaccurate information due to fraud, you may request a free credit report.

- You are unemployed and seeking work: If you are out of work and plan to apply for a job within 60 days, you also qualify for a free credit report.

- You are using public welfare assistance: Recipients of any public assistance, such as welfare, may receive a free credit report.

- You are requesting reports due to identity theft: If you have suffered identity theft or other fraud, you may request a free credit report.

How to check your credit status

“Credit invisible” consumers — a term that describes an estimated 11% of adults in the U.S. in 2021 — have no credit history or credit reports at any of the three major credit bureaus. Without a record of having used consumer credit, you may find it difficult to qualify for personal loans, receive credit card approval or even get a credit score.[9]

Whether a young person just starting your credit journey or a new immigrant without a U.S.-based credit report, your lack of credit history may render you “credit invisible.”[10] You can check your credit status by ordering a copy of your credit report and reviewing the information contained within.[4]

How do credit scores work?

When you apply for new credit, credit scores give potential lenders (and sometimes landlords or employers) an idea of how responsibly you manage your credit. When checking your credit score, lenders use either FICO® scores or VantageScore® models. The factors that impact your credit score from the two models vary slightly, but both include things like payment history, length of credit history and how much debt you have outstanding relative to credit limits.

Your score may be one factor that credit providers use when reviewing your credit or loan application.

What information is on your credit report?

Your credit report summarizes how well you have handled credit accounts in the past. Financial institutions and credit card companies may use this information to decide whether to offer you credit and what terms will apply. Credit reports generally contain the following information: personal identifying data, details about your credit accounts (including current balances and payment history), and any negative financial events such as bankruptcies or collections accounts. Credit reports also reflect “hard inquiries,” which happen when you apply for a loan or other credit and gave permission for lenders to look at your credit history.[11]

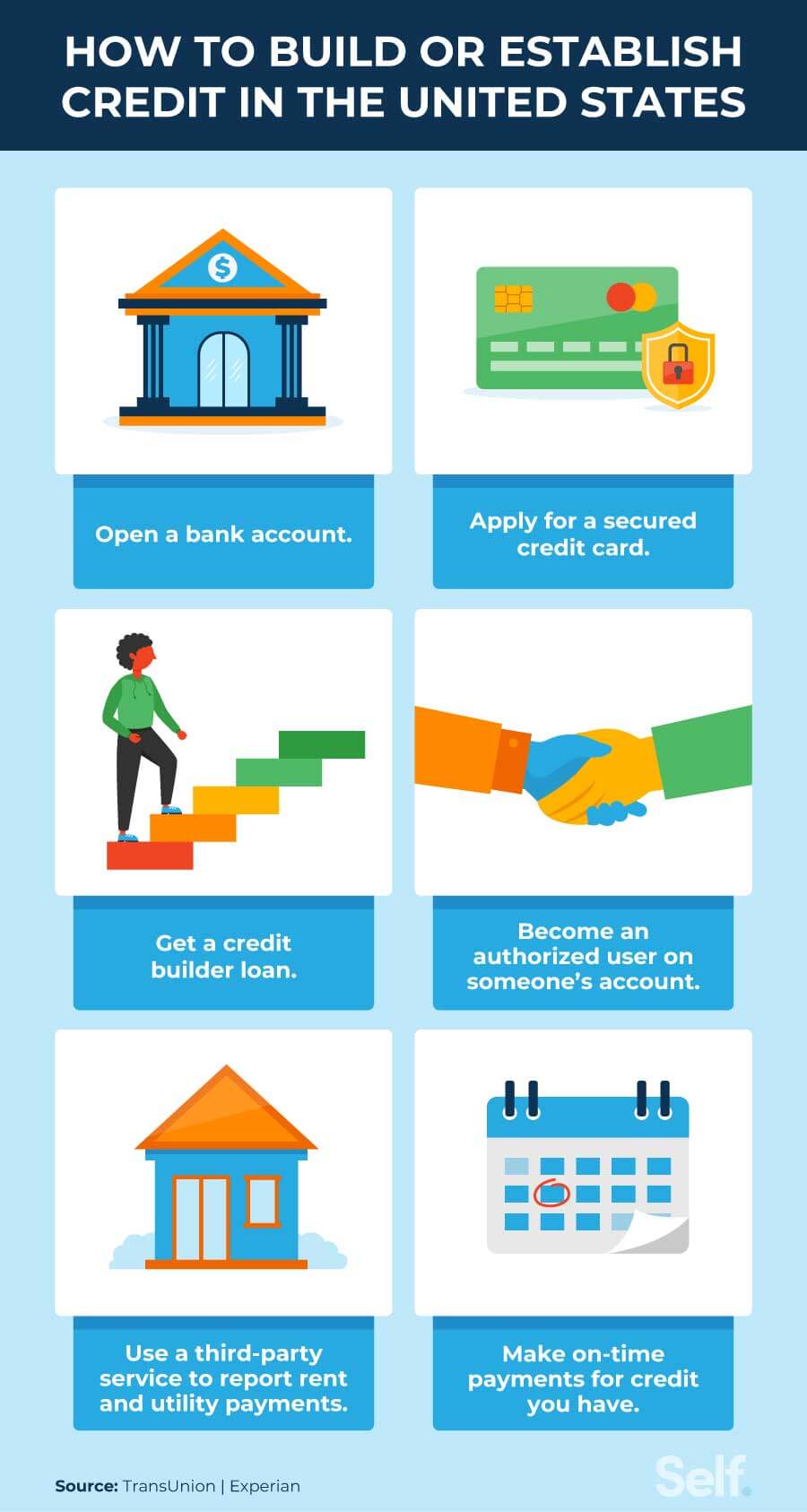

How to establish credit with an ITIN

If you find yourself actually “credit invisible,” you may want to check to see whether the bank you used in your home country will open an account or issue you a credit card with a U.S. branch. [10]

You could also try the following options to establish credit with an ITIN:

- Apply for a secured credit card. If you need to start building credit from scratch, you may want to consider a secured credit card. Specifically designed to help build credit, secured credit cards require a cash security deposit, typically in a savings account or certificate of deposit, to open — and may not require a credit check. Your security deposit typically matches your credit limit, and you can use your card as you would any other credit card. As you pay your monthly bill, those payments — both late and on time — get reported to the credit bureaus. So be sure to pay at least your minimum monthly payment on time to avoid having late payments reported.[10] [12]

- Get a credit builder loan. A credit builder loan helps you to build credit history, but it works differently than traditional installment loans. Instead of receiving a lump sum, your loan proceeds are deposited into a certificate of deposit or savings account, and once you make all your monthly payments you will receive your funds (minus the interests and fees).

- Become an authorized user on someone’s account. Another way to build credit involves becoming an authorized user on a friend or family member’s credit card. When looking for someone to add you as an authorized user, be sure that person pays the account as agreed, has had the account open for a while and maintains a low credit utilization ratio (CUR; the total revolving debt on the account divided by their credit limit). If so, the individual’s good credit habits may positively impact your credit score.Otherwise, becoming an authorized user could hurt your credit.[10]

- Use a rent reporting service to report rent payments. Even if you don’t have credit accounts, you probably have monthly bills like rent, cell phone service and utilities. If you pay your bills on time, you could put that positive payment history to work for you by using a paid service, such as building your credit with free rent reporting.* [10]

- Make on-time payments for credit you have. No matter how you choose to start building credit, remember to always pay your monthly loans and credit card payments by the due date. Since payment history counts for 35% to 41% of your credit score (depending on which model is used), it can play an important role in helping better your credit.[10]

Check your credit report and score frequently

Monitoring your credit report and score regularly helps you keep tabs on your credit-building efforts, find out where you fall on the credit score range, identify errors that may harm your credit and even spot identity theft fraud.

*Results vary. You may not receive an improved credit score. Not all lenders use scores impacted by rent/utility payments.

Sources

- AnnualCreditReport.com. “Frequently asked questions,” https://www.annualcreditreport.com/generalQuestions.action.

- Internal Revenue Service. “Individual Taxpayer Identification Number,” https://www.irs.gov/individuals/individual-taxpayer-identification-number.

- Internal Revenue Service. “Taxpayer Identification Numbers,” https://www.irs.gov/individuals/international-taxpayers/taxpayer-identification-numbers-tin.

- Experian. “Can You Check Your Credit Score Without a Social Security Number?” https://www.experian.com/blogs/ask-experian/can-you-check-your-credit-score-without-a-social-security-number.

- TransUnion. “Get your credit report by mail or phone,” https://www.transunion.com/get-credit-report/mail-or-phone.

- Equifax. "How to Get Your Free Credit Report," https://www.equifax.com/personal/education/credit/report/articles/-/learn/how-to-get-your-free-credit-report/.

- Consumer Financial Protection Bureau. “How do I get a copy of my credit reports?” https://www.consumerfinance.gov/ask-cfpb/how-do-i-get-a-copy-of-my-credit-reports-en-5.

- Federal Trade Commission. “Free Credit Reports,” https://consumer.ftc.gov/articles/free-credit-reports.

- Experian. “What Does It Mean to Be Credit Invisible?” https://www.experian.com/blogs/ask-experian/what-does-being-credit-invisible-mean.

- Experian. “5 Ways Immigrants Can Build Credit in the United States,” https://www.experian.com/blogs/ask-experian/how-can-immigrants-build-credit.

- Experian. “Hard inquiry vs. Soft Inquiry: What’s the Difference?,” https://www.experian.com/blogs/ask-experian/hard-inquiry-vs-soft-inquiry.

- Citizen Path. “New U.S. Immigrants with No Credit Can Establish Good Credit and Obtain a Loan,” https://citizenpath.com/credit-building-immigrants-with-no-credit.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).