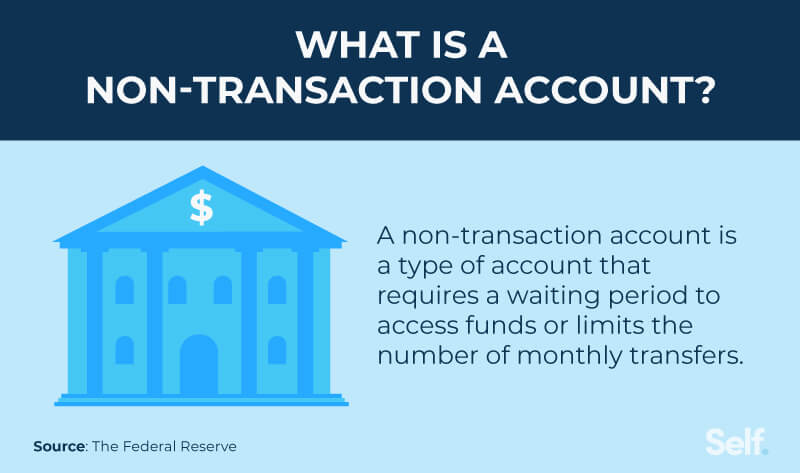

What Is a Non-Transaction Account?

A non-transaction account, also known as a non-payment account, is an account that is not designed to handle frequent transactions. Non-transaction accounts typically limit monthly transfers or have waiting periods before you can withdraw funds.

If you’ve had a payment returned because it was from a “non-transactional account,” it likely means the bank account you used does not allow (or only allows limited) transactions from non-transaction accounts, such as savings accounts, bonds, CDs or IRAs. This article covers the limitations of non-transaction accounts and the difference between non-transaction and transaction accounts.

Key points

- Non-transaction accounts are not designed for frequent transactions and typically have limits on monthly transfers or waiting periods before withdrawals can be made.

- Non-transaction account types include savings accounts, CDs, money market accounts, and retirement accounts such as IRAs.

- Banks may still maintain withdrawal restrictions on non-transaction accounts despite the Federal Reserve eliminating the six-transaction limit in 2020.

How money is transferred to and from accounts

Money is often transferred between accounts through ACH transactions. ACH stands for “automated clearing house,” a network that processes bank-to-bank transfers.[1] Nacha, founded in 1974 and formerly known as the National Automated Clearing House Association, oversees these transactions, which include things such as employer direct deposits and direct electronic payments.[2]

The ACH Network can both push and pull funds to your account. An ACH push, also known as an ACH credit, allows the originator to send money to the receiver. For example, when an employer (originator) directly deposits your paycheck into your bank account (receiver).[3]

An ACH pull, or ACH debit, allows the originator of the transaction to pull money from another account with permission.[3] For example, when your internet company initiates your monthly payment.

But what if that account does not allow funds to be pulled from it or limits how many times funds can be pulled? In that case, it is identified as a non-transaction — or non-payment — account.

Types of non-transaction accounts

Non-transaction accounts are designed for purposes other than conducting regular transactions like checking accounts do:

- Fixed-term accounts only allow investors to recoup their principal investments at the end of a specific period, or fixed term. That money therefore cannot be used for transactions.[4] Examples include term deposits such as CDs and bonds, which reach maturity at a certain date.

- Retirement investment accounts such as IRAs are designed for retirement savings, not transactions. Money in an IRA typically cannot be withdrawn before age 59½ without a 10% tax penalty on the amount withdrawn.[5]

- Savings accounts are designed to build savings, not spend the money in the account. Savings accounts are therefore non-transaction accounts.

Non-transaction accounts vs. transaction accounts

The primary difference between transaction and non-transaction accounts is the degree of liquidity and how quickly you can access the cash.

Transaction accounts, such as checking accounts, are designed to facilitate payments through such means as checks and debit cards. Other types of transaction accounts include automatic transfer services (ATS); NOW accounts (negotiated order of withdrawal), which are checking accounts that earn interest; and some demand deposit accounts, from which deposited funds can be withdrawn at any time.[6]

Non-transaction accounts are less liquid: they’re designed primarily as long-term investment accounts, for savings or retirement.

Under the Federal Reserve’s Regulation D, non-transaction or time deposits must reserve the right at any time to require at least seven days written notice of the intent to withdraw funds. [7]

Regulation D and non-transaction accounts

Prior to April 2020, under the Federal Reserve’s Regulation D you were limited to six “convenient transactions” a month on non-transaction accounts, like savings or money market accounts. If an ACH payment exceeded that limit, it might have been returned.

However, the April 2020 changes to Regulation D allowed banks to suspend enforcing the six-transaction limit so that customers could access their funds during difficult financial times.

While banks can suspend the six-transaction limit, they aren’t required to do so. Check your bank’s policy to understand how many transactions are allowed for non-transaction accounts. It’s also important to understand which types of transactions are not limited. These include ATM withdrawals and in-person withdrawals.[8]

Why was my payment returned due to a non-transactional account error?

With ACH transactions, the reason for your returned payment depends a lot on the type of account you’re using.

If your payment has been returned from a non-transaction account, it likely means the payee couldn’t access the money from the account you specified. An ACH return may occur if you specified a retirement account with withdrawal limitations and penalties or a savings account where you’ve reached your limit of six withdrawals in a month. [9]

You may be able to pay from your checking account via a debit card or check, or, depending on what you are paying, you can use a credit card. (Interest-bearing checking accounts are available, although yields aren’t as high as savings accounts and other vehicles your financial institution may offer.)

Sources

- Investopedia. “ACH Transfers: What Are They and How Do They Work?” https://www.investopedia.com/ach-transfers-what-are-they-and-how-do-they-work-4590120#citation-2. Accessed January 26, 2022.

- Nacha. “ACH Almost Certainly Touches Your Life,” https://www.nacha.org/content/what-is-ach. Accessed January 26, 2022.

- Payments Innovation Alliance. “How ACH Works,” https://achdevguide.nacha.org/how-ach-works. Accessed February 4, 2022.

- Investopedia. “Fixed Term,” https://www.investopedia.com/terms/f/fixedterm.asp. Accessed January 26, 2022.

- Investopedia. “Individual Retirement Account (IRA),” https://www.investopedia.com/terms/i/ira.asp. Accessed January 26, 2022.

- Consumer Financial Protection Bureau. “What is the difference between a checking account, a demand deposit account, and a NOW (negotiable order of withdrawal) account?” https://www.consumerfinance.gov/ask-cfpb/what-is-the-difference-between-a-checking-account-a-demand-deposit-account-and-a-now-account-en-953/. Accessed February 4, 2022.

- Federal Reserve. “Regulation D Reserve Requirements,” https://www.federalreserve.gov/boarddocs/supmanual/cch/int_depos.pdf. Accessed January 26, 2022.

- Federal Reserve. “Federal Reserve Board Announces Interim Final Rule to Delete the Six-Per-Month Limit on Convenient Transfers From the ‘Savings Deposit’ Definition in Regulation D,” https://www.federalreserve.gov/newsevents/pressreleases/bcreg20200424a.htm. Accessed January 19, 2026.

- PaymentCloud. “R20 ACH Return Code: Non-Transaction Account,” https://paymentcloudinc.com/blog/ach-return-codes/r20/. Accessed January 19, 2026.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial Policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).