What Is an Outstanding Judgment and How Does It Work?

An outstanding judgment occurs when a creditor wins a court case against you because you have not paid your debt. When you receive notice by mail of an outstanding judgment against you, it can cause worry and stress. If you have an outstanding judgment against you, you may be wondering what to do. In this post, we explain what exactly an outstanding judgment is, how it can affect you financially, and what steps you can take to handle the situation.

Table of contents:

- What is an outstanding judgment

- What happens if you can’t pay a judgment against you?

- How long do judgments last?

- Can you dispute a judgment?

- How does a judgment affect your credit score

- What to do if you have an outstanding judgment

- Handling a judgment

What is an outstanding judgment?

A judgment is a court order indicating the official result of a lawsuit. If you are sued over a debt you owe, a court may issue a money judgment specifying that you owe a certain amount of money to a creditor or collection agency. Prior to the lawsuit commencing, you must receive official notice of the lawsuit (“service”). If you ignore this notification, you could lose your chance to dispute your debt, and the court will likely issue a default judgment against you. In addition, the court could order that you pay additional fees such as collections costs, attorney fees and interest. So if the court issues a judgment against you and you haven’t paid it, it is referred to as an outstanding judgement.[1]

Outstanding judgments for money owed can be for any kind of debt you haven’t paid, from credit card debt to delinquent accounts with service providers like utility companies or medical bills. However, this post focuses more on outstanding judgments from debts you owe to lending institutions and credit card companies.

What happens if you can’t pay a judgment against you?

When a creditor wins a lawsuit against you, they have much stronger tools to collect the money you owe. While state laws and individual situations vary, the debt collector may be entitled to utilize the following methods to retrieve their money:[1]

- Wage garnishment: Wage garnishment occurs when creditors take a portion of your earnings directly from your paycheck. Federal and state laws regulate how much can be garnished, and federal laws exempt certain income from wage garnishment. Because each state varies in how it treats garnishment, seek advice from an attorney who specializes in collections. Local Legal Bar Associations can help you with recommendations.[2]

- Place a lien against your personal property and real estate: In the case of non-payment of debts, courts can place judgment liens on your assets which gives creditors legal claims to your personal property (your car, for example) as well as real property (your house or land you own, for example). Your real estate and assets affected by the lien can then be seized and sold to repay your debts.[3]

- Collect the funds from your bank accounts: A court order may allow debt collectors to take the money you owe them from your bank account or freeze your account entirely. In addition to the original judgment indicating the total debt, the court may later stipulate how much can be garnished from your wages. [1],[2]

State and federal laws establish limits, exemptions and other protections that apply to debt collection methods. If a creditor is attempting to collect a debt against you, you need to seek the advice of an attorney specializing in debt collections, consult with your local legal bar association, a local legal aid office or contact a JAG office (if you are a service member).[2]

How long do judgments last?

How long creditors have to collect on a judgment varies by state law. Because each state has its own statutes regarding collections, check with your state or local law firm that specializes in debt collection cases to see how long creditors have to collect on outstanding judgments in your state.

Can you dispute a judgment?

Because a judgment is an official court order, only courts can change them. Getting a judgment changed or set aside after the fact can prove very difficult. For that reason, you have a better chance of fighting your debt if you show up in court to defend yourself. In addition, creditors and debt collectors may be willing to negotiate a payment plan with you before the court reaches a decision.[1]

How does a judgment affect your credit score?

Although court judgments can have serious financial implications, you may feel relieved to know the actual judgment no longer appears on your credit report, but that doesn’t mean it won’t affect your credit score. The original credit account that led to the lawsuit may still be on your report for up to seven years from the date on which you were first late with your payment. This negative information can still impact your credit score although its impact lessens over time.[4] However, judgments don’t become invisible. Since lenders can still search public records, judgments issued against you in collection lawsuits may still impact your ability to qualify for credit.[5] Judgments may also show up on your credit report in error, in which case you may need to request that they be removed.[6]

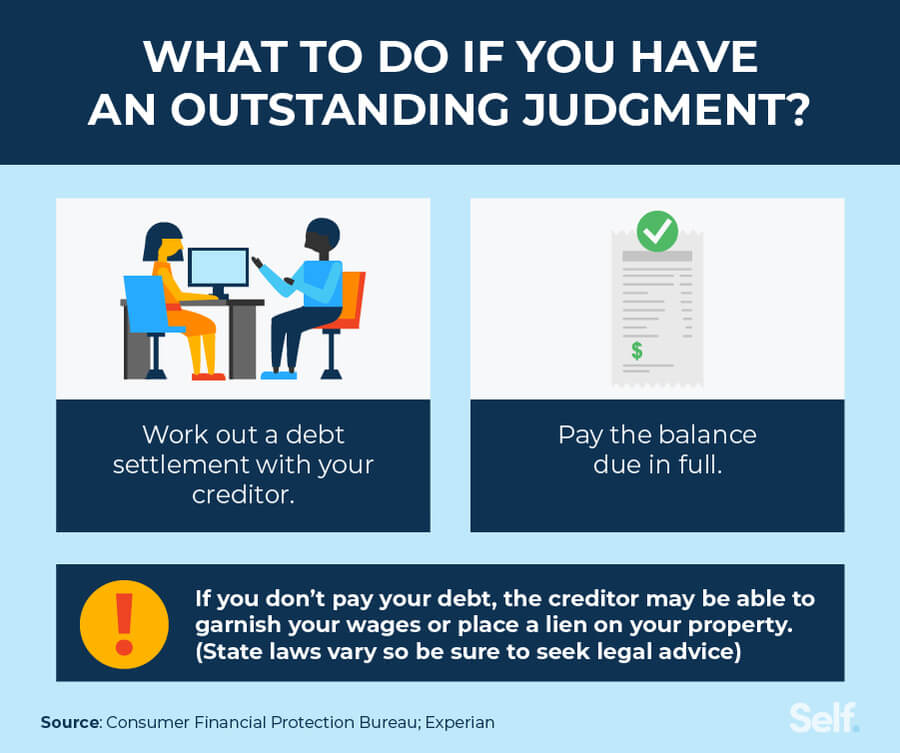

What to do if you have an outstanding judgment

If you have an outstanding judgment against you, consider your options before you proceed.

Work out a debt settlement with your creditor

Creditors might agree to negotiate with you on your outstanding judgment, if you can’t pay the entire amount of what you owe at one time. You can reach out to the collections agency or creditor and try to negotiate a payment plan so that you pay by installment.[7] If you want to negotiate a settlement, consult with an attorney to determine how best to handle and document your negotiations.

Pay the judgment in full

While the best action you can take for your credit is to pay your balances in full before you have a judgment against you, if you do end up being sued by a creditor and have a judgment for debt against you, you may want to pay your judgment in full.[8] If you don’t have the resources to pay in full, find an attorney specializing in collections who can give you legal advice and help you evaluate your options. Failing to pay the judgment in full may result in the court authorizing garnishment of your wages.[1]

Handling a judgment

Because credit reporting agencies no longer include information about judgments, that information will not appear on your credit report. If you haven’t paid a debt to a creditor and are concerned that you may have a judgment for debt against you, you can call your state court or search your public records. If you do discover a judgment, handling it responsibly can play an important role in helping you get your personal finances back on track.

Sources

- Consumer Financial Protection Bureau. “What should I do if a creditor or debt collector sues me?” https://www.consumerfinance.gov/ask-cfpb/what-should-i-do-if-a-creditor-or-debt-collector-sues-me-en-334. Accessed on July 11, 2022.

- Consumer Financial Protection Bureau. “Can a debt collector garnish my bank account or my wages?” https://www.consumerfinance.gov/ask-cfpb/can-a-debt-collector-garnish-my-bank-account-or-my-wages-en-1439. Accessed on July 11, 2022.

- Experian. “What is a Lien?” https://www.experian.com/blogs/ask-experian/what-is-a-lien. Accessed on July 11, 2022.

- MyFICO. “Chapter 7 & 13:How long will negative information remain on my credit report?” https://www.myfico.com/credit-education/faq/negative-reasons/how-long-negative-information-remain-on-credit-report. Accessed October 27, 2022.

- Experian. “Judgments No Longer Appear on a Credit Report,” https://www.experian.com/blogs/ask-experian/judgments-no-longer-included-on-credit-report. Accessed on July 11, 2022.

Experian. “Collections on Your Credit Report,” https://www.experian.com/blogs/ask-experian/credit-education/report-basics/how-and-when-collections-are-removed-from-a-credit-report/. Accessed on July 13, 2022. - Experian. “How to Dispute Credit Report Information,” https://www.experian.com/blogs/ask-experian/credit-education/faqs/how-to-dispute-credit-report-information/. Accessed on July 15, 2022.

- UFCU. “How to Handle a Post-Judgment Debt.” https://www.ufcu.org/personal/learn/tools-advice/financial-advice/conquer-financial-challenges/how-to-handle-a-post-judgment-debt. Accessed October 27, 2022.

- Experian. “Is It Better to Pay Off Debt or Settle It?” https://www.experian.com/blogs/ask-experian/is-it-better-to-pay-off-bad-debt-or-to-settle-it/. Accessed on July 11, 2022.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).