Rent to Own A Home When You Have Bad Credit

Rent-to-own is an arrangement where you move into a home and lease it for an agreed period of time, with the option to buy it at the end. It can be an option for people who are not yet in a position to qualify for a mortgage, giving them time to work on factors such as credit, savings, or debt before applying for a home loan. But before entering into an agreement, it is important to understand how the process works, what the qualification requirements look like, and what the benefits and drawbacks are.

Below, we look at how rent-to-own works, who it may suit, how to qualify, and the pros and cons to consider.

Key findings

- Rent-to-own gives you the option to move into a home before qualifying for a mortgage, with an agreed period of time to work on your finances.

- There are costs involved with rent-to-own agreements, including an option fee and higher-than-average monthly rent payments.

- Rent-to-own agreements are not automatically reported to credit bureaus.

What is a rent-to-own contract?

A rent-to-own contract, also known as rent-to-buy or lease-to-own, is a real estate agreement that allows you (the tenant) to lease a property for a set period of time. Then you have the option to purchase the home if you desire to do so before the lease expires.

In general, you can expect the monthly rent payment on a rent-to-own home to be more than the fair market value of the property. In other words, you could probably rent a comparable property for less money without adding on the option to buy.

Many rent-to-own contracts also include a feature called an “option fee.” An option fee is an upfront deposit that often costs a percentage of the future purchase price of the property.[1] The fee essentially locks in a property so the owner doesn’t sell it to any other party while you’re leasing it. If you follow through and buy the property before the end of your lease, the option fee may go toward your down payment or purchase price.

How does a rent-to-buy contract work?

Most rent-to-own contracts are broken down into two sections:

- Standard lease agreement

- Option to purchase (or commitment to purchase)

If you’re signing a lease-option contract, it will typically lease with the option to buy the property at any time before the lease period ends. A lease-purchase agreement, by comparison, may contain a commitment that obligates you to buy the property at the end of your lease.

In either scenario, you should treat a rent-to-own contract as seriously as you would treat a contract to purchase a property outright. Therefore, it’s wise to hire a reputable real estate attorney to represent you and review the contract before you sign or make any deposits. Finding an experienced real estate agent that is familiar with rent-to-own agreements could also be beneficial.

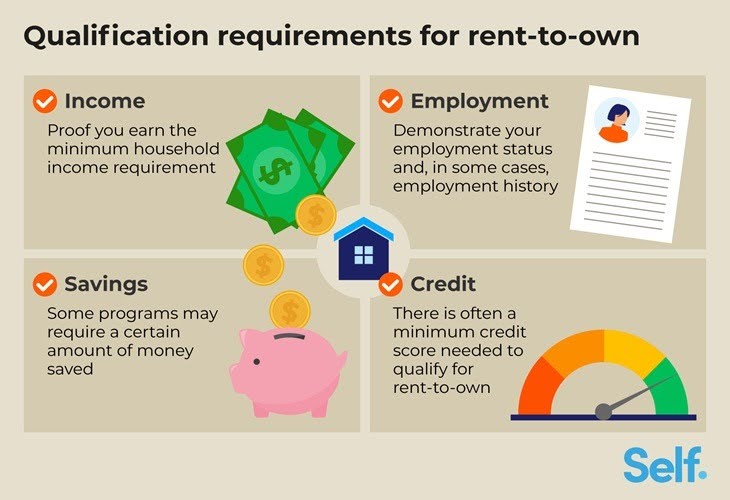

What are the qualification requirements for rent-to-own?

Many of the people who consider rent-to-own agreements do so because they're not in a position to qualify for a mortgage. Yet although it tends to be easier to enter a rent-to-own agreement than qualify for a mortgage outright, there are still requirements you may need to meet. Below are some examples of what you could face when you rent a home with the option to buy it later. [2]

- Credit: Rent-to-own programs typically have a minimum credit score requirement. Some well-known programs set minimums. Divvy requires a minimum credit score of 550. [3]

- Income: Programs will generally have requirements around income and your debt-to-income ratio. Your rental period can give you time to shore up your finances before applying for a mortgage.

- Debt: Your debt levels are likely to be assessed alongside your income as part of any rent-to-own application.

- Savings: Some programs have requirements around savings. Your rental period gives you time to build your reserves before you need to apply for a mortgage.

Source: [2]

Can I do rent-to-own if I have bad credit?

One of the main reasons buyers consider rent-to-own agreements is due to credit challenges. In many cases, you may still qualify with a lower credit score or without a large upfront payment. However, eligibility is not guaranteed, and sellers or rent-to-own companies may still require minimum credit scores or financial checks.

For example, some providers accept applicants with FICO® Scores as low as 550. [3] Rent to own agreements often cater for those with credit challenges or lack of large down payment. [4]

Credit issues that may exclude you from lease-to-own

There are also certain types of credit issues that might disqualify you from a rent-to-own opportunity, such as:

- Active or pending bankruptcy filings

- Evictions or foreclosures on your credit report

- Credit history that shows you’re currently (or recently) past-due on financial obligations

Each owner and rent-to-own program is different, of course. So, your best bet is to find out the specific requirements of the seller or program you are considering to see if you meet the eligibility requirements to participate. Don’t rule out a rent-to-own house if you have bad credit as there are plenty of options.

What are the benefits of doing rent-to-buy?

Below are some of the benefits that a lease-purchase agreement could offer you:

- You won't have to move twice. Rent-to-own means your housing plans are in place all at once. You move in once and, if you proceed with the purchase, you're already home. [4]

- You can save for a down payment while you live there. A portion of your monthly rent payments will likely be funneled into an escrow account, providing a pool of cash to put toward your down payment. [2]

- You have time to prepare your finances. When you apply for a mortgage at the end of your rental period, the lender will consider your credit score, debt-to-income ratio, income and savings. The rental period gives you time to shore up all of these. [2]

- You could build your credit history while renting. Rent-to-own could be a good option for people who have recent credit trouble that they need a few years to repair. Your credit score plays a significant role in the mortgage rate you'll receive and whether you qualify at all. [4]

- You can lock in your purchase price. You'll likely agree on a purchase price with the current owner upfront, which could save you money if home prices increase during your rental period. [2]

What are some disadvantages of the rent-to-own model?

There are also downsides involved with renting a home with the option to buy, including the three obstacles below:

- You'll likely pay higher-than-average rent. Your monthly rent will be higher if a portion of your payment is going into an escrow account. This extra amount is called a rent credit or a rent premium. [2]

- You can expect a nonrefundable option fee. This typically ranges from 2% to 7% of the home's value, due upfront. On a $350,000 home, that could work out to $7,000 to $24,500. You'll lose that amount if you choose not to buy the home. [2]

- You could be responsible for repairs and maintenance. Some contracts may require you to maintain the property and pay for repairs, obligations that usually fall to the landlord when you're renting. Make sure you understand what you're getting before you sign anything. [4]

- Your choice of homes is limited. Most homes for sale are not rent-to-own, so you'll be shopping from a smaller pool. If you need to move before buying, you could also lose your down payment. [4]

- Financing is not guaranteed. If you don't qualify for a mortgage at the end of the rental period, you'll forfeit your option fee and any rent credits paid. If you agree to a lease purchase instead of a lease option, failure to meet the obligations outlined could leave you facing costly legal proceedings. [4]

Does rent-to-own affect your credit score?

Rent-to-own agreements are not reported to credit bureaus so they will not affect your credit score. However, it is possible to use your rent-to-own agreement to help you build credit.

How does rent-to-own build your credit history?

In general, rent-to-own agreements do not show up on your credit reports. And if an item doesn’t show up on your credit with at least one of the major credit bureaus (Equifax, TransUnion, or Experian), then it won’t help you build credit history nor will it have an impact on your credit score—positive or negative.

However, some landlords may be willing to report your rent payments through a third-party service. If you find a landlord who is open to sharing your positive payment history with the credit bureaus (via a third party), your monthly rent payments could have the potential to help you build your credit history and score.[5]

This is one example of how a rent-to-own agreement could help you if you have bad credit and you’re looking for a way to lift your score.

Can rent-to-own hurt your credit history?

Rent-to-own works the same way as a standard rental when it comes to credit. Rent payments do not automatically build credit unless your payments are reported to a credit bureau by you or your landlord through a rent reporting service. However, if payments are being reported, late or missed payments can hurt your score. And if your landlord passes unpaid rent to a collection agency, that debt could appear on your credit report and damage your score further.

It is also worth being aware of how late payments could affect the rent-to-own agreement itself. A lease-option agreement could have conditions under which you lose the option to buy, such as if you are late on a payment or miss deadlines for notifying the seller of your intent to purchase. [4]

On the flip side, if your payments are being reported on time, rent-to-own could be an opportunity to build your credit history during the rental period before you apply for a mortgage.[4]

How do I know if rent-to-own is right for me?

Deciding to rent a home with the option to purchase it down the road is risky. There are many ways for the process to go wrong, and you could lose a lot of money if it does.

For many people, it may be best to consider saving a down payment on your own and working on your credit or other issues that are stopping you from qualifying for a mortgage. Opting for a traditional rental until you’re in a position to qualify for a mortgage is often the safer choice.

However, if you decide that you want to give rent-to-own a try, remember that the terms of the agreement are negotiable—just like when you purchase a home. You can ask the seller to adjust the sales price, the amount of rent that goes toward your down payment, and many other aspects of the agreement. There’s no guarantee that the seller will honor your requests (especially if there is high demand for the property), but you won’t know unless you ask.

Finally, make sure that you hire an attorney to represent you from the start. You may want to find a real estate agent to represent you as well—someone who does not also represent the sellers of the property you’re considering. Renting to own is a big investment, even if it is broken down over time. It’s important to make sure that you have the right people in your corner to protect you.

Sources

- Rocket Mortgage. “Rent-To-Own Homes: What Are They, And How Do They Work?” https://www.rocketmortgage.com/learn/rent-to-own. Accessed on April 29, 2026.

- Experian. “Rent-to-Own Homes: How the Process Works.” https://www.experian.com/blogs/ask-experian/rent-to-own-homes/. Accessed on April 29, 2026.

- Divvy. “How It Works.” https://www.divvyhomes.com/how-it-works. Accessed on April 29, 2026.

- Zillow. “What Is Rent-to-Own?” https://www.zillow.com/learn/rent-to-own/. Accessed on April 29, 2026.

- InCharge.org. “What Are The Pros and Cons of Rent-To-Own?” https://www.incharge.org/housing/rent-to-own-pros-cons/. Accessed on April 29, 2026.

About the Author

Michelle L. Black is a leading credit expert with over 17 years of experience in the credit industry. She’s an expert on credit reporting, credit scoring, identity theft, budgeting and debt eradication.

About the Reviewer

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.