What Are the 5 C’s of Credit

Reviewed by: Lauren Bringle, AFC®

Published on: 07/29/2021

Last Updated: 07/29/2021

Good credit is a smart goal to work toward. But most people don’t want a good credit score simply to earn bragging rights. Although earning stellar credit scores can feel great, there’s probably a deeper reason why you want to improve your credit rating.

Perhaps you want to buy a house or a new vehicle. Or maybe the reason you want good credit is so you can qualify for an attractive rewards credit card. Whatever your motivation for improving your credit, it’s important to understand that credit isn’t the only factor that lenders consider when you apply for financing.

Believe it or not, credit is just one of five details that lenders commonly use to evaluate potential borrowers. Together, these factors make up the 5 Cs of credit.

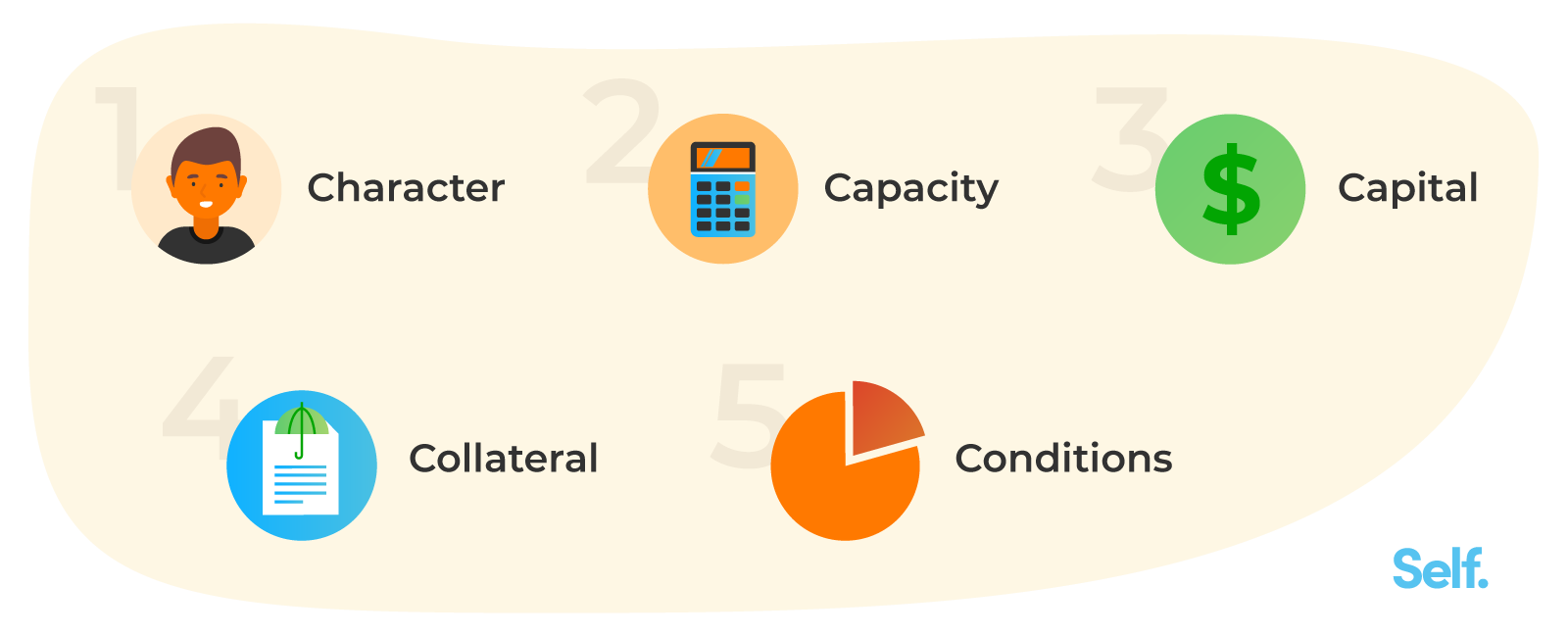

What Are the 5 C’s of Credit?

If you’re curious as to how to raise your credit score by 100 points or how to get a 720 credit score in 6 months, first, you’ll need to know what factors credit bureaus look at.

Whenever a lender or financial institution issues credit in the form of a loan, credit card, or some other financial product, there’s a risk that the borrower won’t repay the lender as promised. This failure to repay can cost the lender a substantial amount of money. And if enough borrowers default on their debts, it could seriously undermine the lender’s profitability.

To help avoid this problem, a lender carefully evaluates each credit application it receives to determine the credit risk level of new applicants. During the evaluation process, the lender considers factors that can help it predict your creditworthiness and your capacity to repay the money you wish to borrow.

There are five common categories of information that lenders may consider when you apply for financing:

- Character

- Capacity

- Capital

- Collateral

- Conditions

Understanding the 5 C’s of Credit

Here’s a deeper look at each of the 5 C’s of credit to help you understand the information that lenders care about most when applying for financing.

Character

When a lender considers your character, it’s examining the likelihood that you will pay back your loan as promised. Your credit history and credit score (or multiple credit scores) are the key details that come into play here.

The purpose of a consumer credit score is to predict how likely you are to become 90 days delinquent or worse on any credit obligation within the next 24 months1. By looking at your credit score and the way you’ve managed your credit obligation in the past, a lender can gain insight into how you might handle your debt in the future.

Capacity

In addition to credit, a lender will generally examine your ability (aka capacity) to repay a new debt based on your income and debts. A lender may calculate your debt-to-income (DTI) ratio (the ratio of your debt obligations to your income) to make this credit risk assessment.

If you’re a small business owner or borrowing money for a business, a lender may also consider your company’s cash flow. Cash flow describes the funds that cycle in and out of your business bank account in a given period.. If you have several loans already, you may also need to figure out what debt to pay off first to raise your credit score and improve your DTI.

Capital

Capital describes the amount of money you’re willing to chip in toward the loan. In other words, it’s a down payment.

On the consumer side, down payments are common when you take out a mortgage or even an auto loan. (Although, you may be able to qualify for a home or auto loan without a down payment in some cases.) With business loans, down payments are perhaps even more routine.

Supplying a down payment can show a lender that you have skin in the game. As a result, you may be less likely to default on your debt.

Collateral

Collateral is a term that describes the assets you pledge to secure financing. In the event you default on the loan, the lender can seize (or repossess) the collateral to help offset its losses.

Some loans are secured by the asset for which you borrowed money to purchase. A mortgage, for example, is secured by your home. When you take out an auto loan, the vehicle serves as collateral.

Other types of collateral might include:

- Business Equipment

- Inventory

- Cash or Cash Equivalents (i.e., Savings, Certificates of Deposit, etc.)

- Real Estate

- Vehicles

Conditions

The final risk category that a prospective lender may consider when you apply for financing involves a number of factors that lie outside of your control. For example, the economy and pending legislative changes could affect you here.

If you qualify for financing, a lender will also calculate the type of interest rate and terms it should offer you based on your risk level.

If you apply for a business loan, demonstrating that your company is growing and thriving could benefit you. Finally, a business lender may also consider the industry you operate in, along with your experience and success managing a business in that space.

Does Every Lender Use the 5 C’s?

There are no universal rules when it comes to a lender’s evaluation process. One bank might be comfortable loaning you money with a FICO® Score of 640. Another financial institution, by comparison, might have a minimum score requirement of 660 for the same type of loan.

In the same regard, some lenders won’t use all 5 C’s of credit to evaluate your financing application. Many credit card issuers, for example, won’t require you to supply collateral when you want to open a credit card. But if you have bad credit, you might need to put down a cash deposit to open a secured credit card to rebuild your credit.

Nonetheless, many lenders rely on the 5 C’s of credit to determine the risk of loaning you money. So, it’s in your best interest to work toward looking good to a prospective lender in each of these five categories.

Why Do the 5 C’s Matter?

From a lender’s standpoint, the 5 C’s (or at least some portion of them) are essential to running a profitable business. Evaluating these areas of risk can help lenders avoid making bad investments. If a large number of a lender’s customers borrow money and default, it could cost the lender a lot of money, or even drive it out of business.

From a consumer’s perspective, the five C’s are important because they impact your ability to borrow money. And if you do qualify for a credit builder loan or credit card, the same factors can influence the price you’ll pay for financing.

How to Use the 5 C’s to Achieve Your Goals

You can use the 5 C’s as a guide to help you become more creditworthy in the eyes of a lender. Once you know the details that lenders care about, you can map out a strategy to:

- Establish or improve your credit score.

- Lower your debt-to-income ratio.

- Save a big down payment.

- Strengthen your assets (i.e., savings, investments, etc.)

When you reduce your risk as a borrower, it could improve the chances you’re approved the next time you apply for financing. And perhaps best of all, understanding the 5 C’s can help you save money on interest rates and fees.

Article Sources

- https://thescore.vantagescore.com/article/119/did-you-know-how-do-late-payments-impact-credit-scores

About the author

Michelle L. Black is a leading credit expert with over 17 years of experience in the credit industry. She’s an expert on credit reporting, credit scoring, identity theft, budgeting and debt eradication. See Michelle on Linkedin and Twitter.

About the reviewer

Lauren Bringle is an Accredited Financial Counselor® with Self Financial– a financial technology company with a mission to help people build credit and savings. See Lauren on Linkedin and Twitter.

Editorial Policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).