What Credit Score Is Used for Car Loans?

You’ve shopped for cars, gone on test drives, and found the perfect vehicle. But will you qualify for an auto loan? Before you’re approved, the lender pulls your credit report to determine your creditworthiness. Your credit report and credit score help them decide whether to grant you a loan and at what interest rate.

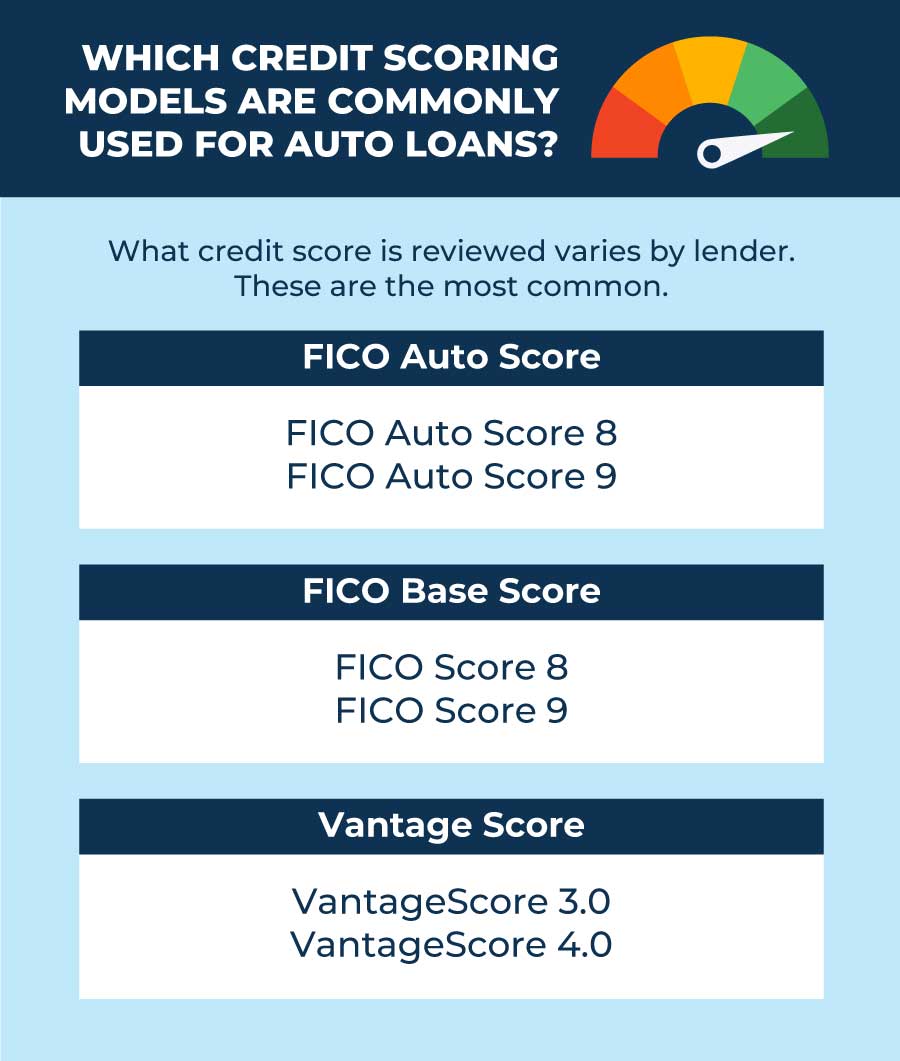

Lenders can choose between many credit scoring models and multiple credit bureaus. So which credit score do car dealers commonly use?

What credit scores do car dealers use?

When you apply for an auto loan, a lender is likely to use one version of the following credit scores: FICO® Auto Score, Base FICO® Score, or VantageScore®. FICO® scores are used by 90% of top lenders and VantageScore® credit scores are used by nine of the 10 largest banks.[1][2]

FICO auto score

FICO® Auto Scores are industry-specific scores that focus on how likely you are to repay an auto loan late. For example, late payments (or other negative information) on past auto loans could damage your FICO® auto score more than other derogatory items.

Instead of the traditional 300-850 credit score range, FICO® Auto Scores feature a scale of 250-900. A higher FICO® Auto Score indicates less credit risk — just like a higher score means less risk under other credit scoring models. With a higher score, you’re more likely to qualify for car financing and get a better interest rate based on each auto lender's criteria. Each individual lender also determines what other financial information they will consider in their credit review process.

Which FICO score do auto lenders use?

Auto lenders use multiple versions of the FICO® Auto Score. (Think about the many versions of smartphone software, and how some users will update their operating systems while others continue to use older options.)

The newest version (as of this writing) is FICO® Auto Score 10, introduced in 2020. However, many auto lenders still use FICO® Auto Score 2, FICO® Auto Score 4, FICO® Auto Score 5, and FICO® Auto Score 8.

Here is a list of which FICO® auto scores are most commonly used by auto lenders for each credit bureau.[3]

- Experian- Auto Score 2, Auto Score 8, Auto Score 9

- Equifax- Auto Score 5, Auto Score 8, Auto Score 9

- TransUnion- Auto Score 4, Auto Score 8, Auto Score 9

FICO score (base model)

Base FICO® scores predict the likelihood that you’ll make a late payment on any credit obligation within the upcoming 24 months. They feature the traditional score range of 300-850.

Lenders use numerous versions of base FICO® Scores. FICO® Score 10 is the most recent (as of this writing). Yet FICO® Score 8, introduced in 2009, remains the most widely used version.[3]

VantageScore

In 2006, a new credit scoring option became available — VantageScore®. The VantageScore® credit score was born out of a collaboration among the three major credit bureaus.

The two most recent versions of the VantageScore® credit score (3.0 and 4.0) feature the industry-standard credit score range of 300-850. Older VantageScore® models had a scale of 501-990.[4]

VantageScore® is becoming increasingly popular among auto lenders. Data shows that the use of VantageScore® in the automotive sector grew by more than 34% in 2023, with captives making up more than 17% of total auto lending usage.[5]

Your credit score will vary depending on the credit scoring model and credit bureau. Under Federal law you can get a free copy of your credit report each year from Experian, TransUnion, and Equifax, and you can now access these credit reports for free weekly at annualcreditreport.com.[6] VantageScore provides free credit score reports from certain providers as well.[7]

FICO® offers an “advanced” plan that provides multiple FICO® Scores, including auto, mortgage and credit versions, as well as a three-bureau credit report and other services for $29.95 a month.[8] FICO® also offers other plans so be sure to check out the pricing page to determine the best option for you, if you believe you need the service.

Even if you don’t know which model your lender is using, it’s important to understand approximately what your credit score is and how that will impact your interest rate.

Which credit bureau is used for auto loans?

There are three major credit bureaus that compile your credit history into credit reports: Equifax, Experian and TransUnion. Lenders can use any credit bureau to determine your loan eligibility.

There isn’t a definitive answer about which credit bureau is used most for auto loans and it could vary by several different factors of how each lender reports to each credit bureau. While most do, lenders are also not required to report to every credit bureau, which may mean that there’s no guarantee your credit information will be the same across all three credit bureaus.[9]

How does a low credit score affect your car loan?

Lenders will look at your credit score to help determine whether to approve a car loan application, but it isn’t the only factor. They’ll also consider your debt-to-income ratio; personal information such as how long you’ve been at your current address or working for your current employer; and the size of the down payment you’re willing to make.[10]

You may still be able to buy a new car with bad credit, but if you’re approved, the factors above will likely affect your loan terms, the size of your monthly payment, and your interest rate. Remember to be mindful of your budget and evaluate used car options. While a luxury car may look appealing, a functional used model may better fit your budget and credit rating.[11]

Higher interest rates

According to the Consumer Financial Protection Bureau (CFPB), your credit score is one of many other factors that can affect your interest rate. Your interest rate may fluctuate based on your credit history, the loan amount, the type of car you’re purchasing, and the length of the loan.[12]

If you’re in the “fair” or “very poor” credit score range, you may want to try to increase your score before applying for a car loan. Borrowers with fair credit may be considered subprime borrowers and aren’t likely to receive the best terms if their loan is approved. Those with very poor credit may be denied altogether or may face high loan rates and additional fees even if they are even approved.

This chart details the average interest rate by credit score for a new or used auto loan. You can see it classifies borrowers in five risk categories by their credit score: deep subprime, subprime, nonprime, prime, or super prime, according to the latest data from Experian for Q2 of 2024.[13]

Disclaimer: All rates are subject to change and lenders may have different categories and scoring models. Please use this strictly as a guide.

|

Credit Score Range |

New Car APR |

Used Car APR |

|

Super prime (781 or above) |

5.25% |

7.13% |

|

Prime (661 — 780) |

6.87% |

9.36% |

|

Near prime (601 — 660) |

9.83% |

13.92% |

|

Subprime (501 — 600) |

13.18% |

18.86% |

|

Deep subprime (500 or below) |

15.77% |

21.55% |

Larger down payments

A lender may see a borrower with a low credit score as a higher risk and may ask for a higher down payment. This can work to your advantage, though, because you’ll have a smaller loan to pay off. If you can afford a large down payment, you might be able to save some money by paying less in interest overall, even at a higher rate.

Ways to improve your credit before buying a car

Before you decide to buy a car, it’s helpful to understand the factors that go into calculating your credit score. You can then tailor your financial activity to help you build credit.

Pay your bills on time

Your payment history is the most important factor in your credit score, making up 35% of your FICO® Score.[14] Making loan payments on time — whether they’re personal loans, student loans or payments to credit card issuers — is an important step to take in building your credit score.

Pay down credit card balances

Your credit utilization ratio is the second-largest factor in calculating your FICO® Score, counting for 30%. This is the amount of credit card debt you have on all your credit cards divided by their combined credit limit.

If you had $2,000 in debt on three credit cards with a total limit of $5,000, your credit utilization would be 40%; experts suggest keeping it below 30%. . Although there is no set point when your credit utilization goes from good to bad, at 30% it will start to have a more pronounced impact on your credit score. Having a higher credit utilization may negatively affect your credit score and lenders may see you as a potentially risky borrower.[15]

Dispute any errors on your credit report

Errors occur on credit reports more often than you might think. Numbers can be transposed; accounts may be incorrectly reported as open, late or delinquent; balances may be off; and fraud can occur. One Consumer Reports study found that 44% of consumers found at least one error on their credit reports, and 27% found serious errors that could affect their score.[16]

Fortunately, you can dispute any errors that are inaccurate. To check for any suspicious entries, you can order a free copy of your credit report at annualcreditreport.com.

Hold off on any new loans

Applying for new loans or new credit can affect your credit score. When applying for new credit, an inquiry is placed on your credit report by one of the three major credit bureaus. Depending on which bureau the lender uses, and on the other factors in your report, this inquiry may lower your score by a few points. However, according to FICO®, if you apply for multiple car loans within a short period (usually 45 days) it will count as just one hard inquiry; this principle also applies to shopping for a mortgage loan.[17]

Build your credit over time

If you think you’re going to be in the market for a car, it’s a good idea to build your credit ahead of time. Focusing on general credit habits can be more helpful than trying to achieve a specific score. Building credit takes time, so be patient and diligent about maintaining good budgeting practices, making payments on time, and keeping your credit utilization low.

If you establish a solid payment history and make on-time monthly car payments, you can build credit and obtain lower rates on financial products such as auto loans or other types of loans.

Disclosure: FICO® is a registered trademark of Fair Isaac Corporation in the United States and other countries. VantageScore and its logo are trademarks of VantageScore. All other trademarks are property of VantageScore unless otherwise designated or clearly implied herein as belonging to third parties.

Sources

- FICOScore. “FICO Scores Are Used By 90% of Top Lenders,” https://www.ficoscore.com/about.

- VantageScore. “Lenders,” https://vantagescore.com/lenders/.

- MyFICO. “FICO Score Versions,” https://www.myfico.com/credit-education/credit-scores/fico-score-versions.

- Experian. “The Difference Between VantageScore® Scores and FICO® Scores,” https://www.experian.com/blogs/ask-experian/the-difference-between-vantage-scores-and-fico-scores/.

- VantageScore. “Auto lenders’ use of VantageScore grew more than 34 percent overall in 2023” https://www.vantagescore.com/auto-lenders-use-of-vantagescore-grew-more-than-34-percent-overall-in-2023-automotive-news/.

- Federal Trade Commission. “You now have permanent access to free weekly credit reports” https://consumer.ftc.gov/consumer-alerts/2023/10/you-now-have-permanent-access-free-weekly-credit-reports.

- VantageScore. “Get Your Free Credit Score,” https://vantagescore.com/consumers/tools/free-credit-scores/.

- MyFICO. “FICO® Advanced,” https://www.myfico.com/products/ultimate-three-bureau-credit-report.

- Consumer Financial Protection Bureau. “What is a credit report?” https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-report-en-309/.

- Forbes. “How To Get A Car Loan With Bad Credit,” https://www.forbes.com/advisor/auto-loans/car-loan-with-bad-credit/.

- Kelley Blue Book. “Can I Buy a Car with Poor Credit History?” https://www.kbb.com/car-advice/can-i-buy-a-car-with-poor-credit-history/.

- Consumer Financial Protection Bureau. “How Does A Lender Decide What Interest Rate To Offer Me On An Auto Loan?” https://www.consumerfinance.gov/ask-cfpb/how-does-a-lender-decide-what-interest-rate-to-offer-me-on-an-auto-loan-en-765/.

- Experian. “Average Car Loan Interest Rates by Credit Score” https://www.experian.com/blogs/ask-experian/average-car-loan-interest-rates-by-credit-score/.

- MyFICO. “How Payment History Impacts Your Credit Score” https://www.myfico.com/credit-education/credit-scores/payment-history.

- Experian. “What Should My Credit Card Utilization Be?” https://www.experian.com/blogs/ask-experian/what-should-my-credit-card-utilization-be/.

- Consumer Reports. “More Than a Quarter of People Find Serious Mistakes in their Credit Reports” https://www.consumerreports.org/money/credit-scores-reports/serious-mistakes-found-in-credit-reports-a1061511185/.

- MyFICO. “Credit Checks: What are credit inquiries and how do they affect your FICO® Score?” https://www.myfico.com/credit-education/credit-reports/credit-checks-and-inquiries.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial Policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).