Which Student Loans Should You Pay Off First?

If you have taken out more than one type of student loan to fund your education, and one of those loans is private, then it’s a good idea to start paying that loan off first. Loans funded by private lenders, rather than the federal government, don’t offer the same protections as a federal loan. They also typically have higher interest rates.[1]

This article will help you understand the differences between types of student loans and which ones to tackle first when student loan payments begin. It is worth keeping in mind that there are many approaches that borrowers can take to paying off student loan debt, and there’s no one-size-fits-all answer.

Here are some factors and options to consider when deciding what approach to take in managing your student loans.

Table of contents

- Understanding types of student loans

- Which loans should you pay off first?

- Methods for paying off student loans

- Moving forward

Understanding types of student loans

In order to understand which student loans to pay off first, it’s important to understand the different types. There are several differentiating factors between private and federal loans and unsubsidized and subsidized loans.

No matter which loans you choose to focus on first, it’s important to make the minimum payment on all your loans. That’s because missed payments can severely affect your credit.

Private vs. federal loans

If you have a private student loan, you’re dealing with a private lender that bases your loan on creditworthiness. Private loans may require a cosigner and may have higher interest rates and less flexible repayment plans than federal loans.

Private student loans can have fixed or variable rates, unlike federal loans, which are typically fixed-rate packages. As a result, interest on private loans can fluctuate to reflect prevailing interest rates as dictated by market conditions, reflecting an underlying index.[2]

- Federal loans are provided by the government and eligibility is calculated from information on your Free Application for Federal Student Aid (FAFSA). Federal loans tend to have lower interest rates and more flexible repayment plans. You may even qualify for an income-based repayment plan.[1]

Subsidized vs. unsubsidized loans

The primary difference between subsidized and unsubsidized loans is when interest starts accruing. With unsubsidized loans, you are responsible for the interest from the outset.

With subsidized loans, the Department of Education pays interest while you are enrolled in college. You typically won’t have to start repaying your subsidized loan and its interest until six months after you stop taking classes (whether you’ve graduated or not). The Department of Education will continue to pay interest during these six months.[3]

It’s therefore a good idea to pay off unsubsidized loans first.

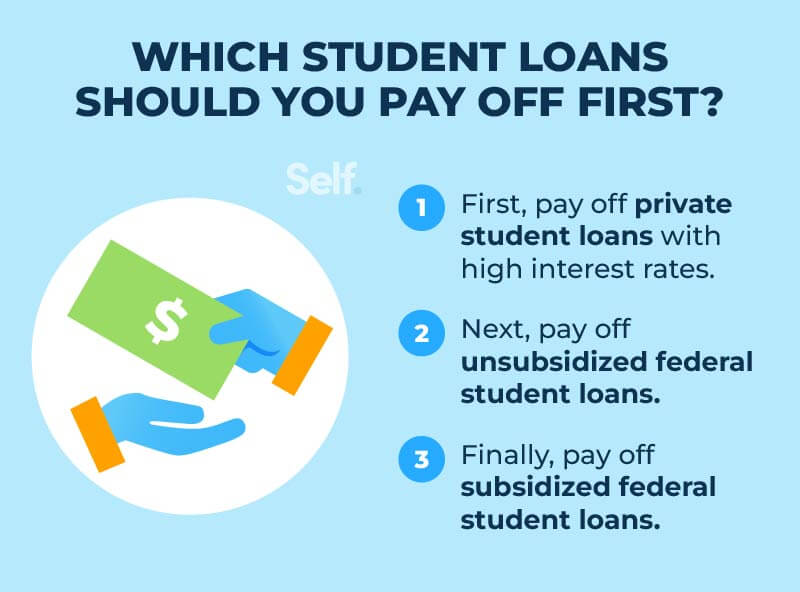

Which loans should you pay off first?

Pay off private loans with high-interest rates first

A private student loan is similar to any other kind of non-student loan you take out.[4] There are no government protections, such as deferment and forbearance options, or income-based repayment, that you get with a federal student loan. Some private loans require you to begin making payments while you’re still in school—something federal student loans don’t do.[1]

It’s a good idea to get private loans with higher interest rates off the table first. The less money you pay in interest, the better. Because of this, it can benefit you to make more than the minimum payment and pay down the principal faster, thereby reducing the interest you pay.[5]

Next, pay off unsubsidized federal student loans

Because interest accrues more quickly on unsubsidized loans than subsidized loans, it’s a good idea to pay those off first.

If you’re thinking about refinancing or loan consolidation, make sure to run the numbers. Federal student loans tend to offer lower interest rates than private loans, and rates that are far below some personal loans.[1] For instance, federal student loans for undergraduates disbursed between July 1, 2021 and July 1, 2022 carry a fixed interest rate of 3.73%.[6] Compare that to the average annual percentage rate for personal loans in 2021, which ranged anywhere from 9.30% to 22.16%.[7]

Paying a federal student loan off with money from a personal loan is likely to increase the interest rate, and you will also lose access to some of the benefits you receive from a federal loan, as mentioned above.

Finally, pay off subsidized federal student loans

This category of federal loan is subsidized because the federal government—via taxpayers—picks up the tab for the interest that accrues while you are in school. This kind of loan is only available to undergraduate students who are in financial need, so it may not apply to you. If you’ve taken out this kind of loan, then it’s the last one you should address when it comes time to pay.

Methods for paying off student loans

Once you’ve figured out which student loans to pay off first, you can determine the best method to do so. Here are four options to consider:

Avalanche method

With the debt avalanche method, you focus on the size of the interest rate, rather than the loan amount, as in the snowball method. You pay off the loan with the highest interest rate first. The advantage to this approach is that you will be spending less money on interest by paying off a high-interest rate loan before it can compound any further. As a result, you will lower your total payments and save money—perhaps a significant amount.

The disadvantage of this method lies in the psychology behind it, compared with the snowball method. You won’t be able to see progress nearly as quickly, so if you have difficulty staying motivated to pay your debts, then the snowball method is likely a better choice.

Snowball method

Under the debt snowball method, you prioritize your debts from the smallest balance to the largest, regardless of what interest rate you’re paying. Then, pay as much as you can toward eliminating the first (smallest) debt on your list, while making minimum payments on the others. This is important because a missed payment on your student loan will appear on your credit report and affect your credit score. Autopay can help you make payments on time and get you closer to paying off your debt.

Once you’ve paid off the first debt, move on to the next one. You can now take the money you would have been paying on the first loan and apply it to the second one, in addition to the minimum you were paying. This is why it’s called the snowball effect. The more loans you pay off, the more money you have to put toward the next loan’s minimum payment, and so on.

It’s important to stay focused as you pursue this method and avoid the temptation to pocket or spend any of the money once a loan is paid off, instead of putting it toward the next one. It’s not “extra money”; it’s needed to pay off your overall debt.

Income-driven repayment plans

Income-based repayment plans are a means of lowering your monthly payments on a federal student loan. These federal student loan refinance plans calculate what you pay based on your family size, as well as income, and contain an element of public service loan forgiveness.

There are four choices:[8]

REPAYE plan. This, generally, is based on 10% of your extra after-tax income. It stands for Revised Pay As You Earn repayment plan.

PAYE plan. The Pay As You Earn repayment plan is based on 10% of your discretionary income, but is never more than the 10-year Standard Repayment Plan amount.

IBR plan. Short for Income-Based Repayment, this amounts to either:

- Generally 10% of your discretionary income for a new borrower from July 1, 2014, forward, and not more than the 10-year Standard Repayment Plan amount.

- Generally 15% of your discretionary income if you are not a new borrower on or after that date, but again, never more than the 10-year Standard Repayment Plan amount.

ICR plan. The Income-Contingent Repayment option is calculated based on either 20% of your discretionary income or what you’d pay on a fixed-payment repayment plan over 12 years, adjusted for your income (whichever is less).

Once you hit the maximum payment cap for any of these plans, the remainder of your loan will be forgiven if you haven’t paid your loan by the end of the repayment term—20 to 25 years. Student loan forgiveness is a great thing. However, the length of that loan term is perhaps the biggest disadvantage of this approach: You may be paying less, but you’ll still be in debt for up to a quarter of a century.

Loan refinancing

Student loan refinancing is an option offered by private lenders that can be worth considering, depending on the terms and interest rates. Student loans generally offer relatively low interest rates, but you may be able to refinance at a lower rate or reduce your payments by taking out a longer-term loan.

See if you can reduce your payments by stretching them out or if you can get a lower interest rate on a new loan. If you have more than one student loan, refinancing can put them all together as one payment. This is similar to loan consolidation, but that term usually refers to combining federal loans into a new single federal loan. Loan refinancing, by contrast, is offered by credit unions, banks, and private companies that specialize in student loans.[9]

Moving forward

Managing student debt takes planning and prioritizing. Student loan repayment can be tricky, but if you take stock of what kinds of loans you have and adopt a strategy that will allow you to repay them as quickly as possible, then they don’t have to be as much of a burden to your personal finance.

Ultimately, knowing your loan balance, interest rates, and the kind of loan(s) you’ve taken out can go a long way toward putting you back in charge of your finances.

Sources

- Federal Student Aid. “When it comes to paying for college, career school, or graduate school, federal student loans can offer several advantages over private student loans,” https://studentaid.gov/understand-aid/types/loans/federal-vs-private. Accessed December 16, 2021.

- Concordia University Irvine. “Fixed vs. Variable Interest Rates,” https://www.cui.edu/uploadedFiles/StudentLife/FinancialAid/Undergraduate/Fixed-vs-Variable-Rate_Info-Sheet.2.pdf. Accessed December 16, 2021.

- Federal Student Aid. “The U.S. Department of Education offers low-interest loans to eligible students to help cover the cost of college or career school,” https://studentaid.gov/understand-aid/types/loans/subsidized-unsubsidized. Accessed December 16, 2021.

- Humboldt State University. “Types of Student Loans,” https://canvas.humboldt.edu/courses/27718/pages/types-of-student-loans. Accessed December 16, 2021.

- U.S. News. “How to Pay Off Student Loans,” https://www.usnews.com/education/best-colleges/paying-for-college/articles/2019-10-30/how-to-pay-off-student-loans. Accessed December 16, 2021.

- Federal Student Aid. “Understand how interest is calculated and what fees are associated with your federal student loan,” https://studentaid.gov/understand-aid/types/loans/interest-rates. Accessed December 16, 2021.

- ValuePenguin. “Average Personal Loan Interest Rates,” https://www.valuepenguin.com/personal-loans/average-personal-loan-interest-rates. Accessed January 11, 2022.

- Federal Student Aid. “If your federal student loan payments are high compared to your income, you may want to repay your loans under an income-driven repayment plan,” https://studentaid.gov/manage-loans/repayment/plans/income-driven. Accessed December 16, 2021.

- ISL Education Lending. “Beginner’s Guide to Refinancing Your Student Loans,” https://www.iowastudentloan.org/articles/college/beginners-guide-to-refinancing.aspx. Accessed December 29, 2021.

About the author

Jeff Smith is the VP of Marketing at Self Financial. See his profile on LinkedIn.

About the reviewer

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.