How Much Should I Spend On Groceries?

When it comes to budget necessities, people usually think of a few basic needs: shelter, power, transportation, health care, and, of course, food.

Food can take up almost 13% of that budget, with some of that going toward food out of the house in addition to groceries.[1]

While food prices are less volatile than gasoline costs, they can still fluctuate seasonally and with changes in supply and demand, so it can be a challenge to figure out what to spend on groceries. However, it’s not impossible. You can set up a monthly grocery budget, and an overall budget, that will help you meet your financial goals.

Planning your meals, creating a grocery list, shopping online, and using coupons are just a few ways to determine how much you should spend on groceries.

How much should I spend on groceries?

The cost of food can be divided into categories, such as money spent on your grocery bill, dining out, money you spend on growing your own healthy food, and buying food at convenience stores.

According to the U.S. Department of Agriculture, Americans spent $1.77 trillion on food in 2019, and prices at the grocery store rose 3.5% in 2020 compared to the previous year. U.S. consumers spent a national average of 8.6% of their disposable personal income on food, with 5% going to food eaten at home and 3.6% to dining out.[2]

The USDA divides spending into two categories:

Food-at-home spending, which includes food purchased at

- Supermarkets

- Convenience stores

- Warehouse club stores

- Supercenters

- Other retailers

Food-away-from-home spending, comprising food purchased at

- Fast-food businesses

- Restaurants (including takeout)

- Schools

- Other dining venues away from home

Since the Great Recession, Americans have used more of their income on away-from-home food spending every year until 2020. The COVID-19 pandemic, however, caused a reversal in this trend: During 2020, food eaten at home accounted for 51.9% of total food-related spending (the first year over 50% since 2008).

With so many restaurants and fast-food places closed or offering only takeout or delivery in 2020, that reversal made sense. It can cost a lot more to eat out than to eat at home. According to one cost comparison of 86 meals, the average price of eating out was $20.37, as opposed to just $4.31 for a home-cooked meal.[3] That’s 4.7 times higher.

But this is just one of several factors that can affect a monthly food budget as part of your overall household budget.

Food costs vary geographically, as well. In 2019, they cost between $2,400 and $2,800 from Pennsylvania across a swath of the Midwest and including some Southern and Southwest states. But they approached $4,000 in the Pacific Northwest and rose above that in Maine and Vermont.[4]

Other factors affecting food costs include age and gender. For example, feeding a 5-year-old child might cost between $27 and $42 a week, while a 55-year-old man might need to spend roughly between $41.50 and $84, and a 55-year-old woman would spend slightly less — between $40 and $75.50.[5]

So, how much you spend on groceries can fluctuate depending on a number of variables, and you’ll have to take those variables into account when creating a meal plan and making a shopping list for your weekly grocery excursion with the goal of saving money.

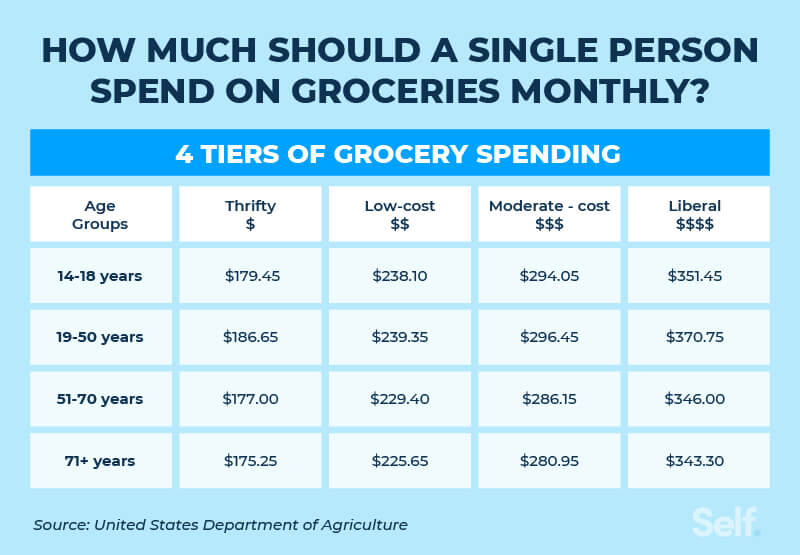

Four tiers of grocery spending

When making a budget and determining your average grocery bill, it helps to be aware of four food plans, or food tiers, as defined by the USDA.

Food plans have been in use since the 1920s. The USDA’s Cost of Food at Home plan reflects shifting food-consumption patterns based on the agency’s most recent household survey, as well as revisions in Recommended Daily Allowances.[6] It uses these to arrive at estimated costs for each of the four tiers:[5]

- Thrifty plan

- Low-cost plan (approximately 25% more than the Thrifty plan)

- Moderate-cost plan (about 50% more than the Thrifty plan)

- Liberal plan (approximately 25% more than the Moderate-cost plan)

The Low- and Moderate-cost plans offer diets that are consistent with what most people eat, while the Liberal plan includes more variety, meat, fruits, and vegetables. They don’t include household items such as paper towels, dish soap, and similar items that you may purchase at the grocery store.

Here’s a quick summary of what your meals might look like in each of the different tiers[6] as well as the average cost of food.[5]

Thrifty

This is the lowest-priced plan and is used as a basis for the Supplemental Nutrition Assistance Program.[7]

This plan will buy you a basic breakfast of orange juice, cereal, toast, and milk. You could have a peanut-butter-and-jelly sandwich for lunch, and dinner might be franks and beans with hash browns, carrots, bread, and a cookie.

As of May 2021, the Thrifty plan costs just under $95 a week for a couple ages 19-50, and a hair under $90 for a couple ages 51-70. For a family of four, the weekly cost goes up to between $138 and $158.

Low-cost

The May USDA table shows that the Low-cost plan costs $121.50 weekly for a couple ages 19-50 and $116.50 for a couple ages 51-70.

Under this plan, you could add coffee cake to your breakfast, have grilled cheese and green beans for lunch, and make yourself a roast beef dinner with potatoes, onions, carrots, and spinach.

For a family of four, the weekly cost goes up to between roughly $177 and $209. (The cost is higher for families with kids in the 6-8 and 9-11 age ranges than in the 2-3 and 4-5 age brackets.)

Moderate

In May, the Moderate-cost plan cost $150.50 a week for a couple ages 19-50 and slightly over $145 for a couple ages 51-70.

The Moderate breakfast could include scrambled eggs and an English muffin; lunch might feature a bologna and cheese sandwich with pickles and apples; the dinner menu would include baked ham and scalloped potatoes.

The price for a family of four ranges between $218 and $260 per week, depending on the children’s ages, with older children costing more.

Liberal

The levels for May showed the Liberal plan cost a little over $188 per week for a couple ages 19-50 and slightly under $176 for a couple ages 51-70.

You’d get bacon and French toast for breakfast under this plan, with cold cuts, cheeses, onion dip, strawberries, and a brownie for lunch. Dinner can be a feast of baked ham, potatoes au gratin, broccoli, salad, and biscuits, with cake and ice cream for dessert.

For a family of four, the cost was about $270 per week for a couple with younger kids and about $316 for a couple with two older children.

Weekly grocery costs by age and gender

In general, grocery costs tend to go up slightly for individuals from infancy through their teens, hitting their peak for men and women around the time they reach adulthood, with the highest costs seen in the 19-50 age range. After that, they fall just slightly for both genders.

Single person

A single adult female can expect to spend approximately the following amounts weekly (with the lower figures in the 71-and-older bracket):

- $39 to $40 under the Thrifty plan

- $49 to $51 under the Low-cost plan

- $61 to $63 under the Moderate plan

- $74 to $81 under the Liberal plan

A single adult male can expect to spend approximately the following amounts weekly (with the lower figures in the 71-and-older bracket):

- $42 to $45 under the Thrifty plan

- $55 to $59 under the Low-cost plan

- $68 to $74 under the Moderate plan

- $84 to $90 under the Liberal plan

A teenage girl can expect a weekly budget of about:

- $41 under the Thrifty plan

- $50 under the Low-cost plan

- $61 under the Moderate plan

- $75 under the Liberal plan

A teenage boy can expect a weekly budget of about:

- $42 under the Thrifty plan

- $59 under the Low-cost plan

- $73 to $75 under the Moderate plan

- $87 under the Liberal plan

Children ages 1-11 can expect weekly costs to rise in the following ranges as they get older:

- $23 to $38 under the Thrifty plan

- $31 to $51 under the Low-cost plan

- $35 to $66 under the Moderate plan

- $43 to $77 under the Liberal plan

Two adults

The cost for two adults in a household varies similarly (see above) and is generally a little more than twice the cost of the combined single cost under the different plans.

Family of four

The cost for a family of four (see above) depends in some measure on the ages of the children because older children require larger budgets. So, as children age, you’ll need to set aside more money for your grocery budget, just as you have to buy new clothes as they outgrow the ones they have.

Tips to stay within your grocery budget

It’s one thing to read a USDA plan, but it’s another to put a reasonable grocery budget into practice. Maybe you’re not the “average American household” and you don’t fit neatly into any of the tiers or household demographic groups defined by the USDA. Don’t worry: You can still create a budget that works for your bank account.

Here are a few steps you can take to get started.

Plan your meals

Start with meal planning. You can use the USDA’s guidelines as a rough outline for how you might want to structure your meals.

You’ll want to plan out balanced meals that offer you the most nutritional value for your money. According to the Harvard School of Public Health, that means devoting roughly half your plate to fruits and vegetables (minus potatoes, whose starchy, high-carb content can drive up blood sugar).[8]

Then set aside a quarter of your plate for whole and intact grains like quinoa, whole wheat, and brown rice, which are less likely to drive up your blood sugar than white and refined grains. The final portion of your plate should consist of protein sources like fish, poultry, nuts and beans. Eat red and processed meats in limited quantities.

Choose water, coffee or tea over sugary drinks, and limit (but don’t avoid altogether) milk, dairy products and juice.

Once you’ve planned out each meal of the day — breakfast, lunch, and dinner — you’re ready for the next step.

Create a grocery list

Based on the meals you’ve planned, create a grocery list of everything you’ll need to make them. Then go through your fridge and cupboards and see what you already have. Cross off those items that you find in the house so you’re not wasting money by doubling up.

Order online instead of shopping in the store

Grocery shopping doesn’t have to mean going to the store. Ordering online can help you save money in a few different ways. For starters, you’ll be saving money on the gasoline you’d be spending heading out to the store if you avail yourself of free delivery services. But that’s just the beginning.

How many times have you set a budget for yourself and tried to add it all up in your head (or on your phone) as you’re going up one aisle and down the next, searching for that elusive item? If you shop online, everything gets added up for you as you put it in your virtual shopping cart, so you can stop or reassess when you hit your pre-budgeted max.

Then there’s the ever-present danger that you’ll go shopping and see something not on your list that you just “have to have.” Shopping online reduces impulse buying, especially when you’re hungry; since you can’t get the instant gratification of eating that candy bar or drinking that soda the minute you’ve paid for it, you might choose to skip those extras altogether.

Shopping online can also help you stick to your list because you can easily compare it with what you place in your virtual shopping cart. And because you’re less likely to forget anything, you won’t need to hop back in the car for a quick trip to the store, where you may end up buying other things you don’t need.

You can even build credit by using your credit card and paying off the balance every month, further helping you stick to your budget.

Use coupons

Coupons can be great money-saving tools, and you don’t just find them in the newspaper or the mailbox anymore. There are myriad sites online that offer you discounts that can be redeemed at a number of different stores and websites.

Coupons can save you money on items on your grocery list and can help you budget because you’re paying attention to the bottom line. But it’s important to remember not to buy something just because you have a coupon. If you see a coupon that doesn’t apply to anything in your meal plan or on your list, don’t use it.

The same goes for filling out your order to get free delivery: Only do so if you’re buying something on your list. (This is a good reason not to shop in small quantities: If you do your weekly shopping all at once, you won’t have to worry about spending enough for free delivery because you’re more likely to meet the minimum amount while still sticking to your list.)

The bottom line

How much you should spend on groceries depends on your situation: things like where you live, how many people you’re buying for, your/their demographics, and what food plan you choose will all affect your budget.

Once you’ve got that figured out, you can make a meal plan, use that as a basis for a grocery list, then shop selectively, exploring your online options and using coupons where appropriate.

If you do these things, it’s more than feasible to reduce your monthly average cost of groceries and get the best nutrition possible for the least amount of money.

Sources

- U.S. Bureau of Labor Statistics. “Consumer Expenditures - 2019,” https://www.bls.gov/news.release/cesan.nr0.htm. Accessed August 6, 2021.

- USDA Economic Research Service. “Food Prices and Spending,” https://www.ers.usda.gov/data-products/ag-and-food-statistics-charting-the-essentials/food-prices-and-spending/. Accessed July 22, 2021.

- Forbes. “Here’s How Much Money You Save By Cooking At Home,” https://www.forbes.com/sites/priceonomics/2018/07/10/heres-how-much-money-do-you-save-by-cooking-at-home/?sh=1707a97135e5. Accessed July 22, 2021.

- Insider. “Here's what the average person spends on groceries annually in every state,” https://www.businessinsider.com/what-people-spend-annually-on-groceries-in-every-state-2019-7. Accessed July 22, 2021.

- USDA. “Official USDA Food Plans: Cost of Food at Home at Four Levels, U.S. Average,” https://fns-prod.azureedge.net/sites/default/files/media/file/CostofFoodMay2021.pdf. Accessed July 22, 2021.

- Purdue University. “Food Plans,” https://www.four-h.purdue.edu/foods/Food%20plans.htm. Accessed July 22, 2021.

- USDA. “USDA Food Plans: Cost of Food (monthly reports),” https://www.fns.usda.gov/taxonomy/term/415. Accessed July 22, 2021.

- Harvard T.H. Chan School of Public Health. “Healthy Eating Plate,” https://www.hsph.harvard.edu/nutritionsource/healthy-eating-plate/. Accessed July 22, 2021.

About the Author

Lauren Bringle is an Accredited Financial Counselor® with Self Financial – a financial technology company with a mission to help people build credit and savings. See Lauren on Linkedin and Twitter.

Editorial Policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).