How Much Will Paying Off Credit Cards Improve Credit Score?

When it comes to raising your credit score, lowering your debt is a good idea. Paying off a credit card is a step in that direction because the amount you owe counts for 30% of your FICO® score.

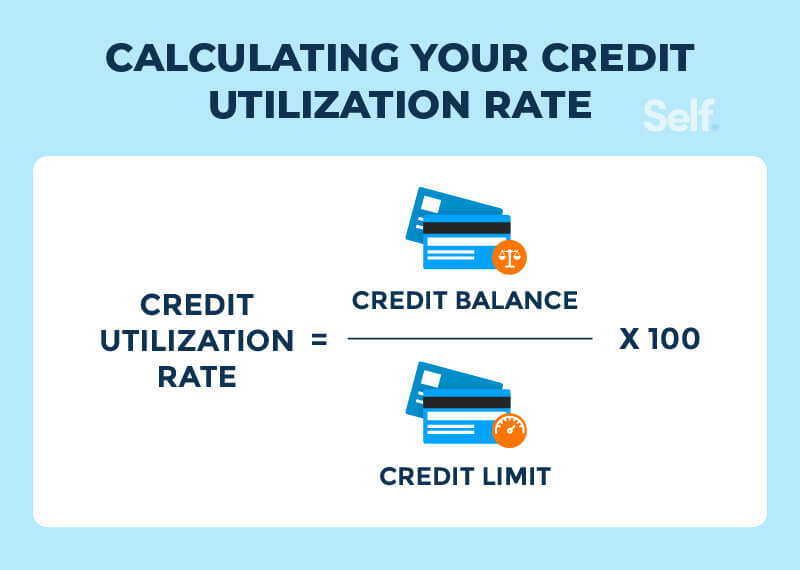

However, it’s not simply the amount you owe that matters. It’s how much you owe in relation to your total credit limit. This is known as your credit utilization ratio.

The simplest way to put it is: Paying off your credit card, or lowering your balance, will decrease your credit utilization rate, which can help increase your credit score.

What impacts my credit score?

The FICO® system and the VantageScore system weigh five factors in determining your credit score, but they evaluate each factor slightly differently.

FICO®’s method is widely used by lenders when determining credit risk, so we’ll look at how credit scores are calculated below.

- Payment history (35%): Your payment history reflects your on-time payments and any missed or late payments.

- Amounts owed (30%): Your credit utilization ratio is how much you owe compared to your overall credit limit.

- Credit history length (15%): The longer you maintain good payment history, the better this category will look.

- Credit mix (10%): The variety of credit you have in your credit profile. For example, since installment loans and credit cards work differently, having both in your credit history may indicate you’re better able to manage credit.

- Recent activity (10%): If you apply for too much credit during a short period, this could indicate you’re a greater credit risk.

What happens to my credit score when I pay off my credit card in full?

Your credit score will likely rise if you pay off your credit card because your credit utilization ratio decreases. However, how much your credit utilization ratio drops depends on where it began. For example, it’s more significant to pay off $1,000 in debt when your credit limit is $1,200 than when your limit is $10,000.

Say your credit utilization rate is high, and you pay off a high-limit credit card. That would help your credit score more than paying off a high-limit card when you don’t owe much.

Let's revisit our earlier example of three credit cards with a total credit limit of $3,000 and combined debt of $1,200. Imagine you owe $500 on a card that has a $1,000 credit limit, and you pay it all off. That reduces your total debt to $700 and brings your credit utilization ratio down to 23%, which is a significant drop from where it first was (40%).

Imagine, however, that you decide to close that credit card after you paid it off. Then, you'd have an overall credit limit of $2,000 but the same total debt of $700. In that case, your credit utilization ratio would be 35%.

It's better, therefore, to keep your credit accounts open as long as you can use your credit cards responsibly.

How much will my credit score increase after paying off my credit card?

This depends on how much your credit utilization ratio changes. Experts agree that it's best to shoot for a credit rate below 30%[1]. But don't stop there because borrowers with the best credit scores have a credit utilization ratio below 10%[2].

Although your credit utilization ratio counts for 30% of your credit score, any steps to improve it don't happen in isolation. You're also lengthening your credit history, for example. And if you miss a payment, it's likely to offset improvements made by paying off a card.

All these factors work together in determining your credit score. How much your credit score goes up after paying off a credit card depends on how much it changes your credit utilization. But what you're doing to maintain and build your credit in other areas matters, too.

How long will it take for my credit score to improve after paying off my credit cards?

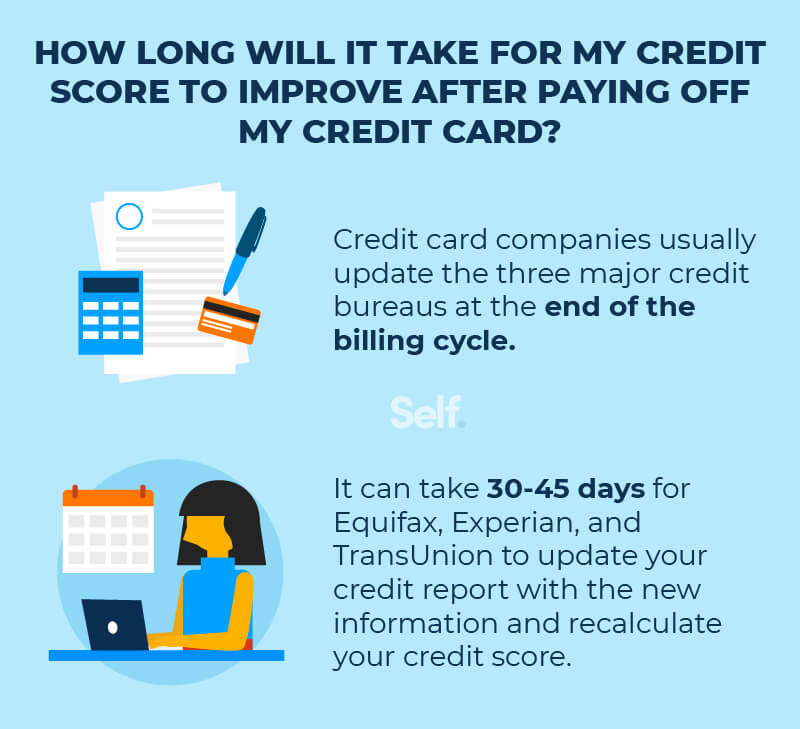

Lenders report your activity to three main credit bureaus: Experian, Equifax, and TransUnion. This typically occurs at the end of each billing cycle.

Payments don’t become late or delinquent until they’re more than 30 days past due. By the same token, it will take 30 or 45 days for any positive activity, such as paying off a credit card, to appear on your credit report. FICO® and VantageScore use these credit reports in their credit scoring models.

Reasons why my credit score would go down

There are many reasons why a credit score might drop. Here are just a few:

- You missed a payment by more than 30 days.

- Other derogatory marks such as bankruptcy, repossession, or foreclosure.

- You applied for a new credit card, car loan, or other line of credit, triggering a hard inquiry.

- Your credit card balances have gone up, increasing your credit utilization ratio.

- You recently paid off a loan, narrowing your credit mix or reducing the average age of your accounts.

- Your overall credit limit has gone down, which could happen if:

- You closed a credit card account.

- A lender has lowered your credit limit based on factors such as a change in your income, credit history, or credit score.

Say your credit card limit is reduced, but your balance remains the same. In that case, your credit utilization rate will be higher.

Other factors include errors in your credit report and fraud or identity theft. Mistakes happen more often than you might think, with one study revealing at least one error on more than 34% of credit reports[4].

Using your credit card wisely

There are many ways to keep your credit in good standing and potentially qualify for lower interest rates.

- Make your payments on time. This is the most important thing you can do since it counts for the biggest chunk of your credit score. Creating a comprehensive budget and setting up automatic payments from your financial institution can help ensure you’re never late.

- Don’t charge more than you need. Keeping the balances on your credit cards low enables you to maintain a low credit utilization rate. This will come in handy when qualifying for loans and low interest rates on major purchases, such as a car or home or a personal loan for major repairs.

- Use your card for daily purchases. Using your credit card for everyday needs, then paying it off at the end of each month, builds your credit. Plus, you can earn rewards or cash back with your purchases.

- Don’t just pay the minimum amount. Each month, your credit card company will issue a statement with the minimum balance you owe—a percentage of your total debt on that card. Paying only the minimum can keep your debt level high because interest will continue to accrue; paying more than the minimum will reduce your principal and the amount of interest you’re paying.

- Set up transaction alerts. Getting an alert on every transaction made with your card will enable you to spot and report fraudulent transactions immediately.

- Lock cards you’re not using. Some companies allow you to do this as protection against fraud and theft. You can use it to your advantage as a way to keep your account open and preserve your credit utilization ratio rather than closing your card.

Tips to improve your credit score

Here are some ways to potentially boost your credit score:

- Start by getting a free credit report and looking for reasons why you might have bad credit. You’re entitled to a free report from each credit bureau each year under federal law, and you can study it for late payments and other negative marks.

- If you find errors or fraud, file a dispute with the credit reporting bureau where you found the error. You can do so online, by mail, or by phone.

- Limit loan applications. If you’re shopping around for a home or auto loan, then all your applications will count as just one hard inquiry—as long as they’re done within a short time. Try to complete this process within 30 days to avoid multiple hard pulls. Learn more about credit inquiries here.

- Resolve late payments immediately. In a perfect world, you’ll make all your payments on time. If you miss one, don’t delay paying it off. Each 30-day period that you’re late counts as a negative mark against your credit.

- Be cautious about moving debt around. There are advantages to consolidating loans, such as simplifying and potentially reducing the size of your payments. However, consolidating debt can hurt your FICO® score by narrowing your credit mix. Besides, it doesn’t eliminate debt and may actually keep you in debt longer. Balance transfers with low APRs (annual percentage rate) are attractive, but be sure you can pay the balance before the interest rate increases.

- Open at least three accounts. People with high credit scores tend to have an average of three open cards.[5] While having more open credit cards increases your total credit limit, you still need to manage them well as described above. Don’t apply for them all at once in order to avoid the appearance that you won’t be able to pay what you owe.

- If you have poor credit, look for ways to re-establish it. Two ways to do that are becoming an authorized user on another person's account or depositing a few hundred dollars to open a secured credit card.

- Get help from a nonprofit credit counseling group. Such groups can help you assess where you stand and develop a strategy for budgeting and debt management.

Remember multiple factors affect your credit score

Improving your credit score isn’t as simple as paying off one or more of your credit cards. You want to keep your credit utilization rate low without losing sight of the other factors that play a part in building good credit.

Develop a comprehensive strategy that involves making on-time payments, maintaining a good credit mix, resolving any late payments immediately, and applying for new credit mindfully. As a result, you can build a more robust credit profile and access the loans you need at the interest rates you want.

Sources

- CNBC. “22% of millennials used their stimulus check to pay off credit card debt—here’s how that could improve your credit score”, s://www.cnbc.com/select/paying-off-credit-card-debt-boosts-credit-score. Accessed September 8, 2021.

- CNBC. “Here’s how much you should really spend on your credit card to get the best credit score”, https://www.cnbc.com/select/how-to-get-the-best-credit-score. Accessed September 8, 2021.

- Equifax. “How Long Does Information Stay on My Equifax Credit Report?”, https://www.equifax.com/personal/education/credit/report/how-long-does-information-stay-on-credit-report. Accessed September 8, 2021.

- Consumer Reports. “More Than a Third of Volunteers in a Consumer Reports Study Found Errors in Their Credit Reports”, https://www.consumerreports.org/credit-scores-reports/consumers-found-errors-in-their-credit-reports-a6996937910. Accessed September 8, 2021.

- CNBC. “Here’s how many credit cards people with excellent credit scores have,” https://www.cnbc.com/2018/07/11/how-many-credit-cards-should-you-have.html. Accessed October 25, 2021.

About the author

Lauren Bringle is an Accredited Financial Counselor® with Self Financial – a financial technology company with a mission to help people build credit and savings. See Lauren on Linkedin and Twitter.