How Credit Works

If you monitor your credit score on a regular basis, you may notice changes from time to time. Sometimes the reason your score changed is obvious. Other times it’s not. It can be frustrating to see your credit score drop if you don’t know what caused it. You may feel like you’ve been doing everything you can to build credit, only to see your score decline.

So why did your credit score go down when nothing obvious changed? We’ll explain what factors affect your credit score and why you may have seen it decline.

Your credit score is updated once every 30 to 45 days and it can change every time it’s updated. While your payment history makes up the largest portion of your credit score, there are other factors to consider—such as your credit utilization rate—that might be more difficult to track. Here are a number of reasons why your credit score can drop.

In addition, your credit score can be affected—for the better—when negative information falls off your credit report. Many negative marks stay on your credit history for seven years, but Chapter 7 bankruptcies can stay on your credit report for 10 years and credit inquiries disappear after just two years.

Both FICO® and VantageScore® rate credit on a scale from 300–850 and consider five factors when determining your credit score, but they define and weigh those factors differently. Your payment history accounts for 35% of your FICO® score, which is more than any other factor, so it’s important that you make on-time payments. Missed payments or those that are more than 30 days late can greatly affect your credit score.

Your credit utilization rate is the second-biggest factor in determining your FICO® score, accounting for 30% of the total. It’s calculated based on the ratio of how much you owe on all your credit cards to your total credit limit on those cards. So, if you have three cards with a total credit limit of $5,000 and you owe a balance of $1,000, then your credit utilization ratio would be 20%.

Experts advise you to keep your credit utilization ratio below 30%, so if you have high credit card balances in relation to your credit limits on your credit card accounts, it may lower your credit score. If you recently made a large purchase on one of your credit cards, it might affect your credit utilization, although paying the balance in full by your next due date may result in just a temporary impact. One good way to know whether this factor is impacting your score is to track your monthly statements and see how big your overall balances are compared to your total credit limit.

If you paid off and closed a credit card account, your credit utilization may increase and could cause your score to drop.[2]

However, paying off debt is a good thing and ultimately it should help your credit score more than hurt it.

Closing an account that has been open for several years can hurt your credit score in another way as well. The length of your credit history counts for 15% of your FICO® score, so keeping an old account open can be to your advantage. If you have a short credit history, this is probably more important than an older, more established credit history with multiple accounts.

In a 2021 Consumer Reports survey of 6,000 people, 34% of respondents found at least one error on their credit reports, with 29% finding errors related to their personal information. In addition, one in 10 found it difficult or very difficult to access their reports.[3]

Fortunately, there are steps you can take to fix these errors and remove inaccurate information on your credit profile.

A hard credit inquiry, on the other hand, can affect your credit score. Hard inquiries are credit checks for activities you initiate, such as applying for a credit card, car loan, or mortgage. Hard inquiries fall under the category of new credit (new accounts you applied for and/or opened), which counts for 10% of your FICO® score.

By changing passwords frequently, being on guard against phishing attempts, not giving out personal information over the phone, and monitoring your credit reports regularly, you can help ensure you’re not a victim of identity theft.

From making on-time payments to monitoring your credit score and paying down debt, there are a number of things you can do to keep your credit score from dropping—and make it move in the right direction.

If you choose to access your credit report from the three major credit bureaus (Experian, TransUnion, or Equifax), you’ll be able to see all your lines of credit, the age of your accounts, credit history, fraud alerts, etc. You may need to purchase your credit score separately.

Disclosure: FICO® is a registered trademark of Fair Isaac Corporation in the United States and other countries. VantageScore® and its logo are trademarks of VantageScore®. All other trademarks are property of VantageScore® unless otherwise designated or clearly implied herein as belonging to third parties.

So why did your credit score go down when nothing obvious changed? We’ll explain what factors affect your credit score and why you may have seen it decline.

Why did your credit score change?

Credit card issuers and other lenders typically report your activity to credit bureaus every 30 days. This is because, in most cases, you have 30 days after your due date to make a monthly payment before your account is listed as delinquent. (You may, however, incur late fees even if your payment is just one day late.)Your credit score is updated once every 30 to 45 days and it can change every time it’s updated. While your payment history makes up the largest portion of your credit score, there are other factors to consider—such as your credit utilization rate—that might be more difficult to track. Here are a number of reasons why your credit score can drop.

1. Negative information

Negative information is a term that applies to items such as bankruptcies, charge-offs, delinquent accounts, and derogatory marks like late payments, tax liens, foreclosures, lawsuits, etc. While you may be aware of these when they occur, you may not know how many points they will cost you on your credit score.In addition, your credit score can be affected—for the better—when negative information falls off your credit report. Many negative marks stay on your credit history for seven years, but Chapter 7 bankruptcies can stay on your credit report for 10 years and credit inquiries disappear after just two years.

2. Missed payments

Credit scores are compiled by private companies such as the Fair Isaac Corporation (FICO®) and VantageScore®, with 90% of top lenders using the FICO® score as their gauge.[1]Both FICO® and VantageScore® rate credit on a scale from 300–850 and consider five factors when determining your credit score, but they define and weigh those factors differently. Your payment history accounts for 35% of your FICO® score, which is more than any other factor, so it’s important that you make on-time payments. Missed payments or those that are more than 30 days late can greatly affect your credit score.

3. High credit utilization

How you use credit is also important. Even if you made all your payments on time, high credit usage (known as credit utilization) can affect your credit score.Your credit utilization rate is the second-biggest factor in determining your FICO® score, accounting for 30% of the total. It’s calculated based on the ratio of how much you owe on all your credit cards to your total credit limit on those cards. So, if you have three cards with a total credit limit of $5,000 and you owe a balance of $1,000, then your credit utilization ratio would be 20%.

Experts advise you to keep your credit utilization ratio below 30%, so if you have high credit card balances in relation to your credit limits on your credit card accounts, it may lower your credit score. If you recently made a large purchase on one of your credit cards, it might affect your credit utilization, although paying the balance in full by your next due date may result in just a temporary impact. One good way to know whether this factor is impacting your score is to track your monthly statements and see how big your overall balances are compared to your total credit limit.

4. Paid off debt

When you pay off a debt, the loan account may close and affect the average age of all your other opened accounts. This may also cause a less diverse credit mix if you paid off an installment loan, like a student loan, and you only have revolving lines of credit open.If you paid off and closed a credit card account, your credit utilization may increase and could cause your score to drop.[2]

However, paying off debt is a good thing and ultimately it should help your credit score more than hurt it.

5. Closed account

Closing an account can potentially hurt your credit utilization rate. For example, if your total balance on all credit cards is $1,500 and your total credit limit across all cards is $4,000, then you have a credit utilization rate (CUR) of nearly 38% ($1,500 divided by $4,000). However, if you close a credit card you never use that had a $500 credit limit with a zero balance, then your overall credit utilization will go up—in this case, your CUR would increase to nearly 43% ($1,500 divided by $3,500). If you haven’t used your card for an extended period, then some companies may close your account without notifying you, and this can be reflected in your credit score, too.Closing an account that has been open for several years can hurt your credit score in another way as well. The length of your credit history counts for 15% of your FICO® score, so keeping an old account open can be to your advantage. If you have a short credit history, this is probably more important than an older, more established credit history with multiple accounts.

6. Reported error on a credit report

Sometimes, a change in your credit score might not make sense to you because you didn’t do anything to affect it. Errors on credit reports can impact your credit score, too. They can take a number of forms, including incorrect reporting, transposed numbers, the same debt being listed twice, and debts being listed with incorrect balances. Fraud and identity theft are also risks.In a 2021 Consumer Reports survey of 6,000 people, 34% of respondents found at least one error on their credit reports, with 29% finding errors related to their personal information. In addition, one in 10 found it difficult or very difficult to access their reports.[3]

Fortunately, there are steps you can take to fix these errors and remove inaccurate information on your credit profile.

7. Recent credit inquiries

Companies, like lenders, landlords and insurance companies may pull your credit report to review your creditworthiness and depending on the circumstances it could result in a hard inquiry or soft inquiry. While a soft inquiry will show up on your credit report, it will not affect your credit score. Soft inquiries include things like a lender checking on whether to make you a pre-approval offer, a potential employer or landlord examining your credit, or you checking your own credit.A hard credit inquiry, on the other hand, can affect your credit score. Hard inquiries are credit checks for activities you initiate, such as applying for a credit card, car loan, or mortgage. Hard inquiries fall under the category of new credit (new accounts you applied for and/or opened), which counts for 10% of your FICO® score.

8. Identity theft

Identity theft is more common than you may realize, even if you keep up on the headlines. One in 20 Americans are affected by identity theft each year, with 13 million consumers reporting total fraud losses of almost $17 billion in 2019. Thieves can steal your identity, and your money, through unauthorized credit/debit card use by taking over someone’s account, by using it to open credit accounts or take out loans, or to commit tax fraud.[4]By changing passwords frequently, being on guard against phishing attempts, not giving out personal information over the phone, and monitoring your credit reports regularly, you can help ensure you’re not a victim of identity theft.

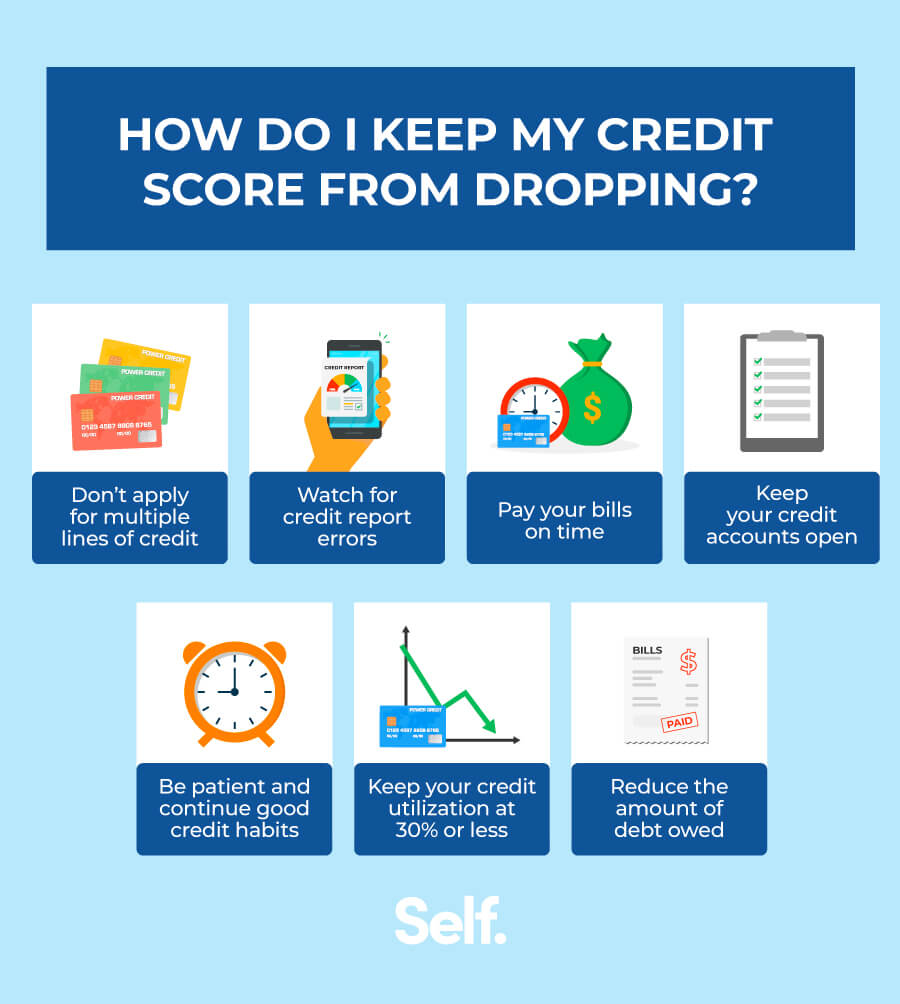

How do I keep my credit score from dropping?

From making on-time payments to monitoring your credit score and paying down debt, there are a number of things you can do to keep your credit score from dropping—and make it move in the right direction.

Don’t apply for multiple lines of credit

Applying for multiple new credit cards or loans within a short period of time can hurt your credit score. Trying to open too many new accounts can be a red flag to lenders that you may be having trouble with your bills and might not be a good credit risk. However, multiple applications for a car loan within a short period of time will only count as one application (hard inquiry) because it is a sign you are comparing deals. The specific time period depends on the credit model used and can be anywhere from 14 to 45 days.Make on-time payments

Paying your credit accounts on time has the biggest impact on your credit score. As mentioned above, your FICO® score is determined by five factors: payment history, amounts owed, age of credit accounts, credit mix (having a variety of credit products), and new credit (not just new accounts you opened but also applications for credit and inquiries). Because your payment history counts for more than any other single factor, you can potentially do more to maintain good credit by making on-time payments than by any other single action.Keep your credit utilization at 30% or less

A good rule of thumb is to keep your total outstanding balance at 30% or less of your credit limit. Paying off your revolving credit balances can help you do so. In fact, in order to achieve an excellent credit score, many experts recommend that you keep your credit utilization at 10% or less.[5]Reduce the amount of debt owed

High outstanding debt such as credit card debt can negatively affect your credit score. It’s better to pay it off than simply moving it around. Applying for a credit card with a six-month or one-year introductory rate of low or zero interest can be helpful if you use the opportunity to pay down debt. However, repeatedly applying for such cards to avoid interest for as long as possible without paying down the balances might be a sign that you’re unable to pay what you owe.Watch for any credit report errors

Do credit monitoring periodically and check for any credit fluctuations. You’re entitled to receive a free credit report from each of the three credit bureaus, Transunion, Experian and Equifax once a year from annualcreditreport.com. However, you can also get copies of your credit report more frequently from credit agencies to monitor it more closely, and it doesn’t cost all that much. A credit reporting company can’t legally charge you more than $13.50 for a credit report.[6]If you choose to access your credit report from the three major credit bureaus (Experian, TransUnion, or Equifax), you’ll be able to see all your lines of credit, the age of your accounts, credit history, fraud alerts, etc. You may need to purchase your credit score separately.

Keep your credit accounts open

Open accounts can be a good thing if you have low credit utilization. It’s a good idea to keep unused credit cards open so you benefit from longer average credit history and larger amounts of available credit. A long-term account may have a positive impact on your credit score.Be patient and continue good credit habits

You won’t be able to achieve an excellent credit score overnight. Building credit takes time, so be patient. Make your payments on time, pay down your debts, and your credit score may start to climb.Learn how credit works

Your credit is an important part of your personal finance. The more you know what goes into compiling your credit score, the better you’ll be able to make sense of it and know how to raise it. Monitoring your credit reports for errors, keeping up on payments, paying down debt, building a strong credit history, and maintaining low credit utilization are all steps you can take to improve or maintain a good credit score.Disclosure: FICO® is a registered trademark of Fair Isaac Corporation in the United States and other countries. VantageScore® and its logo are trademarks of VantageScore®. All other trademarks are property of VantageScore® unless otherwise designated or clearly implied herein as belonging to third parties.

Sources

- FICO® Score. “FICO® Scores are Used by 90% of top lenders,” https://www.ficoscore.com/about. Accessed January 26, 2022.

- Experian. “Why Credit Scores Could Drop After Paying Off Credit Cards,” https://www.experian.com/blogs/ask-experian/why-credit-scores-could-drop-after-paying-off-credit-cards/. Accessed January 26, 2022.

- Consumer Reports. “How the Credit Reporting System Fails Consumers and What to Do About It,” https://advocacy.consumerreports.org/wp-content/uploads/2021/06/A-Broken-System-How-the-Credit-Reporting-System-Fails-Consumers-and-What-to-Do-About-It.pdf. Accessed January 26, 2022.

- Experian. “How Common Is Identity Theft?” https://www.experian.com/blogs/ask-experian/how-common-is-identity-theft/. Accessed January 26, 2022.

- CNBC. “Does a $0 balance on your credit card make your score go up?” https://www.cnbc.com/select/what-is-a-good-credit-utilization-ratio/. Accessed January 26, 2022.

- Consumer Financial Protection Bureau. “How do I get a copy of my credit reports?” https://www.consumerfinance.gov/ask-cfpb/how-do-i-get-a-copy-of-my-credit-reports-en-5/. Accessed January 26, 2022.