What Does Your Credit Score Start At?

Before you have established any credit history at all, your credit score is nonexistent. Once you start to build credit and enough information appears on your credit report, credit scoring models can generate a credit score based on your credit history.

The lowest credit score given by two of the most common credit-scoring models, FICO® and VantageScore®, is 300, and the highest is 850. But this also does not mean everyone starts at this number. You are unlikely to begin with a score as low as 300 unless your early credit activity reflects very poor financial habits.

Read on to find out more about what a credit score represents, how your unique score is calculated, and what steps to take to achieve a credit score that is sufficient for you to fulfill your financial goals. [1]

Key points

- Your credit score does not start at zero; before you establish any credit history, you typically have no credit score at all because credit scoring models require information from your credit report to generate a score.

- Once you begin using credit and enough information appears on your credit report, scoring models like FICO® and VantageScore® typically generate scores ranging from 300 to 850 based on your credit activity.

- The time it takes to receive your first credit score depends on the scoring model and your credit history, but lenders commonly use factors such as payment history, credit utilization, credit history length, new credit, and credit mix to calculate it.

What credit score do you start with?

Every person begins their credit trajectory with no credit score at all — because without a credit history, there is nothing on which to base how likely you are to repay your credit debts. Therefore, no credit score can be generated. [1] Before you secure different types of credit — such as personal loans, car loans, and other credit products — your score will be nonexistent.

Once you start building a credit history, your score will sit somewhere between the lowest, 300, which indicates very poor credit, or the highest, 850, which indicates excellent credit.

It’s also important to understand that you will not have only one credit score, but that your score will vary depending on the scoring model, credit report used and date on which it is calculated. Because lenders aren’t required to report to each of the three main credit bureaus — Experian, Equifax TransUnion — information on each credit report may differ slightly. It’s possible, for example, that one model may pull information from a credit report that shows you have limited credit history while another may pull from a credit report that has more information reported. [2]

How long does it take to get a credit score?

How long it takes to build credit and get your first credit score depends on your individual financial history. You are considered “credit invisible” until you have an active credit account.

You must have a credit report generated by the credit bureaus before you can earn a credit score because scoring models pull information from various reports to generate your score. [3] Two of the most common scoring models used to arrive at a credit score are FICO® and VantageScore®.

- FICO® generally requires that at least one credit account on your credit report has been open for six months or more before a score can be generated. [4]

- VantageScore® was designed to be more accessible and may generate credit scores for more consumers, including those with limited credit history who may not yet qualify for a FICO® score.[5] The model was created by the three major credit bureaus — Experian, Equifax, and TransUnion — and uses information from a consumer’s credit report to evaluate credit behavior and calculate a score.[5]

Can you build credit without a credit card?

Building credit does not dictate that you obtain a credit card. You may not have your first credit card yet, but you can use other ways to establish your credit history. [6] Any time you secure credit in some fashion, you can build your credit history, such as:

- Using third-party reporting services to report rent and utility payments

- Taking out a credit builder loan

- Taking out a loan with a cosigner

- Taking out a car loan

- Taking out a student loan

What is a good credit score?

With credit scores typically ranging from 300 to 850, you may be wondering what is considered a good credit score. Generally, FICO® considers a score between 670 and 739 range “good,” [7]whereas VantageScore® considers any credit score between 661 and 780 as “prime.” [8] According to Experian’s Consumer Credit Review, the average credit score in the United States was 713 as of September 2025.[9]

A credit score is an important indicator of your ability to repay credit. Your score will impact your personal finances because, while lenders consider several factors before extending credit to you, they use your score as one factor that helps them to evaluate the likelihood that you’ll pay back what you owe. These considerations may impact the terms you receive for credit, such as your interest rates. [7]

The following tables break down the credit score from poor to excellent according to both the FICO® and VantageScore® credit-scoring models.

FICO®

| Credit Score Category | Range |

|---|---|

| Exceptional | 800+ |

| Very Good | 740–799 |

| Good | 670–739 |

| Fair | 580–699 |

| Poor | <580 |

VantageScore®

| Credit Score Category | Range |

|---|---|

| Superprime | 781–850 |

| Prime | 661–780 |

| Near Prime | 601–660 |

| Subprime | 300–600 |

How is your credit score calculated?

The FICO® and VantageScore® models use data about your credit and how you pay the credit extended to you, both positive and negative, to arrive at your credit score. Each scoring model may consider information reported to any of the three main credit bureaus — Experian, Equifax, and TransUnion — to arrive at a consumer’s credit score.

The process is very individualized, so what affects your credit score and the way in which the factors are evaluated varies from person to person. [10] A score may also depend on which version of each model is being used; your FICO 8® Score may differ from your FICO 9® or FICO 10® Score.

Factors that are not considered by credit-scoring models, however, are age, geographical location, race, religion, national origin, sex, marital status, or information about your job. [11]

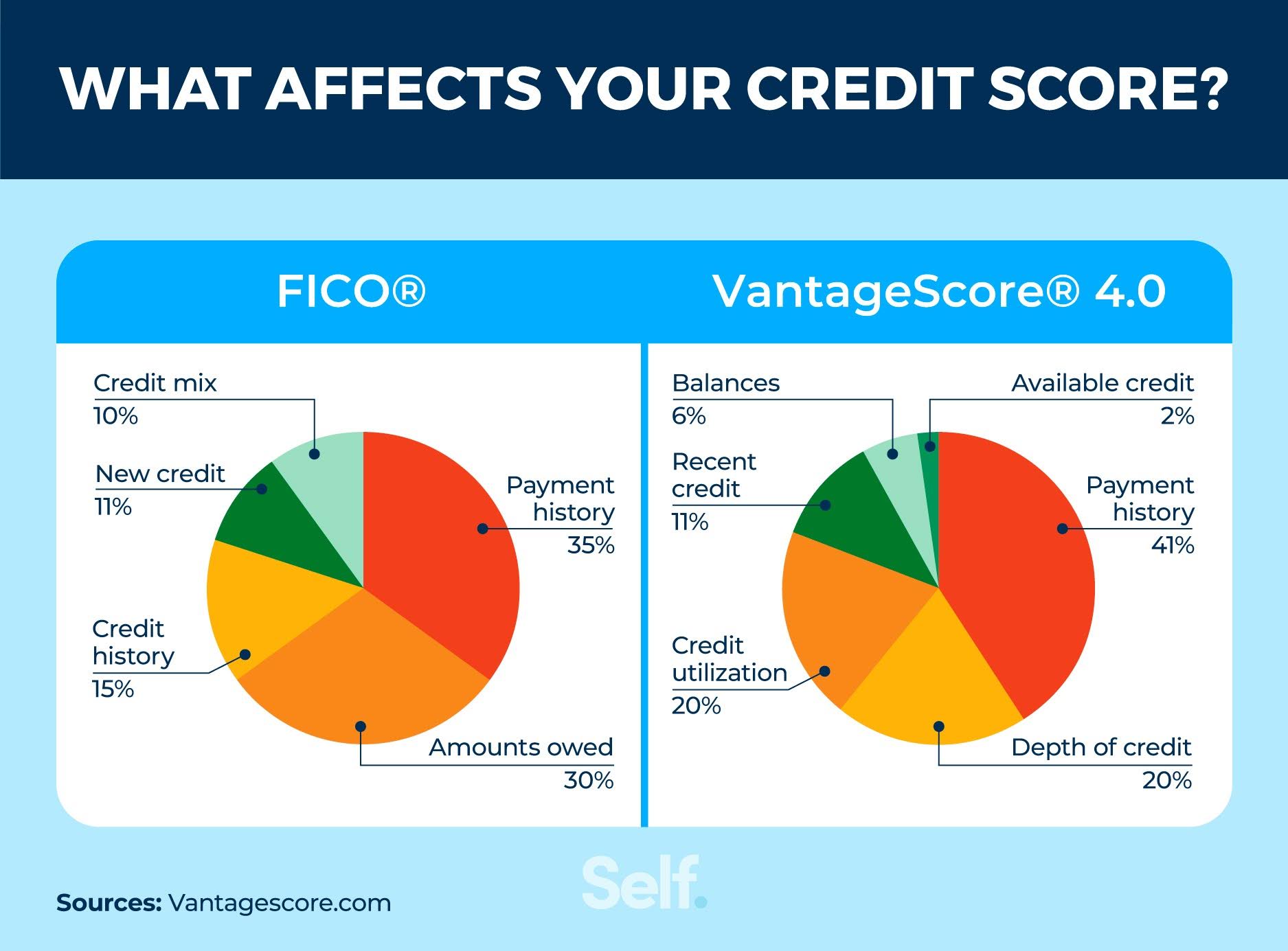

Credit Score Components

A credit score is made up of various components, which credit-scoring models categorize slightly differently but in essence represent the same information. Here are the components of a FICO® and a VantageScore® credit score.

FICO® [10]

- Payment history (35%): Because a credit score indicates to potential lenders how likely you are to pay back what you owe, your payment history influences your score the most. It will reflect whether you have a history of late or on-time payments.

- Amounts owed (30%): This component factors the total amount of debt you owe on credit cards and loans, as well as your credit utilization rate (CUR), which is the amount of revolving debt you owe divided by the total amount of your revolving credit limits.

- Length of credit history (15%): Your credit history refers to the length of your credit history, or the amount of time you have had credit.

- New credit (10%): This element factors recent credit inquiries and new types of credit.

- Credit mix (10%): For this factor, the various types of credit you have open are taken into account, and lenders can assess how well you repay different types of credit. These types may include credit cards, student loans, and a mortgage.

VantageScore® 4.0 [8]

- Payment history (41%): Just like the FICO® model, VantageScore® considers this factor to be highly influential to your score. It reflects whether you make on-time or late payments.

- Depth of credit (20%): This category considers both the age of your credit accounts as well as the type of credit accounts you use, which is known as “credit mix” for FICO® scoring.

- Credit utilization (20%): Slightly different than the credit utilization referred to with FICO® scoring, this factor looks at the relationship of credit you use and the credit you have access to. While revolving credit is the focus, installment loans are considered as well. When it comes to your credit utilization ratio (CUR), the ratio of revolving debt compared to your credit limit, VantageScore® suggests keeping this above 0% but below 30%.

- Recent credit (11%): This category weighs the number of accounts you’ve opened recently as well as the hard inquiries reflected on your credit report. All hard inquiries within a 14-day period will be considered as one inquiry by VantageScore®.

- Balances (6%): With this factor, VantageScore® evaluates the remaining balances on your current and delinquent accounts.

- Available credit (2%): As the category suggests, this factor looks into how much available credit you have on revolving accounts.

How often is your credit score updated?

Your credit score is updated to reflect any changes to your credit activity. These changes can improve or worsen your credit score or have little impact if not much has changed. Lenders typically provide new information about your credit performance to the three major credit bureaus once a month. [12]

How do you check your credit score?

If you are curious about your credit score, there are various ways you can check it. Some services offer access to your current FICO® credit score, while others may require a paid subscription, depending on the plan and level of detail provided. Some banks and credit card issuers also provide customers with their FICO® score free of charge. [13]

Similarly, some banks and credit card issuers provide customers and the public with their VantageScores free of charge, but the scores might just be from one credit bureau. You will have one score from each bureaus’ credit report. You can also purchase your VantageScore® from Experian. [14] [15]

How to check your credit report

Your credit report is not the same as your credit score. Credit scores are derived from the information in your credit report and are used by lenders to evaluate applications for products such as mortgages, credit cards, and auto loans, as well as to determine the rates you may be offered. [16]

Your credit report outlines your current credit status: what you owe, whether you make payments on time, and other items like collection accounts, for example. Monitoring your credit report regularly allows you to check for any mistakes that need to be corrected and keeps you informed of what information is appearing in your credit report. So you see what lenders can see being reported about you. You can access free credit reports from each of the three major credit bureaus — Experian, Equifax, and TransUnion — through AnnualCreditReport.com. Consumers can currently obtain free weekly credit reports from these bureaus using this service.

Effective ways to start building credit

The earlier you get started on your credit journey the better you will fare when applying for credit or a loan. Here are some first steps to take to get started.

Apply for a credit builder loan

Different from traditional loans with which you receive money upfront and pay it off over time, a credit builder loan holds your funds in a certificate of deposit (CD) or a savings account. You receive the loan proceeds once you make all your payments (minus interest and fees), and your lender reports your payments to the credit bureaus. [17]

For example, Self’s Credit Builder Account enables you to build credit history and savings. It’s a loan in a bank-held certificate of deposit (CD) that you pay off in monthly installments, and each payment is reported to all three credit bureaus. At the end of the period, you receive the money back, minus interest and fees.

Get a secured credit card

With secured cards, as opposed to unsecured cards, you are required to make an upfront deposit of cash that acts as collateral. This deposit equals your credit limit. These cards can then be used as any other credit card to make purchases. Any payments you make (or fail to make) to pay your balance are reported to credit bureaus by your credit card company. [18]

The secured Self Visa® Credit Card is one example of such a credit card. Although requirements are subject to change, you may be able to qualify for the Self Visa® Credit Card either by applying directly and providing a minimum $100 security deposit from your bank account or debit card, or by first opening a Credit Builder Account and meeting eligibility criteria.

If you’re using a Credit Builder Account, you may become eligible by keeping your account in good standing and reaching at least $100 in savings progress. Your savings can then be used as the security deposit, which sets your credit limit.

Become an authorized user

If you are not able to apply for your own credit card, you can become an authorized user. This means a friend or family member can add you to their account, enabling you to use the credit card. Though the primary cardholder is ultimately liable for making the payments, you should come to an agreement with them about if and how you must repay what you charge. Before you become an authorized user, be sure the credit card company reports the account history for authorized users so that you can build a credit history by piggybacking that account. [18]

When seeking out a trusted friend or family member to add you as an authorized user, be sure that person pays the account as agreed, has had the account open for a while and maintains a low credit utilization ratio (CUR; the total revolving debt on the account divided by their credit limit). If so, your credit score could be positively impacted by that person’s good credit habits. On the other hand, if that person doesn’t follow good credit habits, becoming an authorized user could hurt your credit.

Use third-party reporting services

Another simple way to build a strong credit record is through third-party reporting services like Self’s Rent and Bills Reporting*, which lets you get credit for payments you already make. You can use these services to add positive financial steps such as paying rent and bills on time to your credit file, which may help your credit score. While not all credit scores factor in rent and bill payments, FICO 9, FICO 10, FICO XD, and VantageScore do.

Starting your credit journey

Building credit takes time and patience, but the right tools can help along the way. Self offers products and resources to help you understand your credit and stay on track with your payments. Begin your credit-building journey by checking out Self’s Credit Builder Account, so you can start building credit and savings at the same time.

*Results vary. You may not receive an improved credit score. Not all lenders use scores impacted by rent/utility payments.

Sources

- Experian. “Does Your Credit Score Start at Zero?,” https://www.experian.com/blogs/ask-experian/what-does-your-credit-score-start-at/. Accessed March 6, 2026.

- Consumer Financial Protection Bureau. “What is a credit score?,” https://www.consumerfinance.gov/ask-cfpb/what-is-a-credit-score-en-315/. Accessed March 6, 2026.

- Experian. “What Does It Mean to Be Credit Invisible?,” https://www.experian.com/blogs/ask-experian/what-does-being-credit-invisible-mean/. Accessed March 6, 2026.

- myFICO. “What are the minimum requirements for a FICO® score?,” https://www.myfico.com/credit-education/faq/scores/fico-score-requirements/. Accessed March 6, 2026.

- Experian. “What Is a VantageScore Credit Score?” https://www.experian.com/blogs/ask-experian/what-is-a-vantagescore-credit-score/. Accessed March 6, 2026.

- Experian.“Can You Have a Credit Score Without a Credit Card?,” https://www.experian.com/blogs/ask-experian/can-you-have-credit-score-without-credit-card/.Accessed March 6, 2026.

- myFICO. “What Is a Credit Score?,” https://www.myfico.com/credit-education/credit-scores. Accessed March 6, 2026.

- VantageScore. “The Complete Guide to Your VantageScore,” https://vantagescore.com/press_releases/the-complete-guide-to-your-vantagescore/. Accessed March 6, 2026.

- Experian. “Experian Consumer Credit Review.” https://www.experian.com/blogs/ask-experian/research/consumer-credit-review/ . Accessed March 6, 2026.

- myFICO. “What’s in my FICO® scores?,” https://www.myfico.com/credit-education/whats-in-your-credit-score. Accessed March 6, 2026.

- Experian. “What Is a Good Credit Score?,” https://www.experian.com/blogs/ask-experian/credit-education/score-basics/what-is-a-good-credit-score/. Accessed March 6, 2026.

- TransUnion. “How Long Does It Take for a Credit Report to Update?,” https://www.transunion.com/blog/credit-advice/how-long-does-it-take-for-a-credit-report-to-update. Accessed March 6, 2026.

- CNBC “FICO Scores are used in 90% of U.S. lending decisions—here’s where to get yours for free,” https://www.cnbc.com/select/where-to-get-a-free-fico-score/. Accessed March 6, 2026.

- VantageScore. “Get Your Free Credit Score,” https://www.vantagescore.com/consumers/tools/free-credit-scores/. Accessed March 6, 2026.

- VantageScore. “VantageScore® The first tri-bureau credit score*,” https://www.experian.com/consumer-products/vantage-score.html. Accessed March 6, 2026.

- Consumer Financial Protection Bureau. “What is the difference between a credit report and a credit score?” https://www.consumerfinance.gov/ask-cfpb/what-is-the-difference-between-a-credit-report-and-a-credit-score-en-2069/. Accessed March 6, 2026.

- Equifax. “What Is a Credit Builder Loan?” https://www.equifax.com/personal/education/credit-cards/articles/-/learn/credit-builder-loan/. Accessed April 17, 2026.

- Experian. “How to Get Credit for the First Time,” https://www.experian.com/blogs/ask-experian/how-can-i-get-credit-for-the-first-time/. Accessed March 6, 2026.

- Equifax. “What Is an Authorized User on a Credit Card?” https://www.equifax.com/personal/education/credit-cards/articles/-/learn/authorized-user-on-a-credit-card/. Accessed March 6, 2026.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

About the author

Becca has over 10 years of experience as a content writer, working across various industries including finance, digital marketing, education, travel, and technology. Her work has been featured in publications including Forbes, Business Insider, AOL, Yahoo, GOBankingRates, and more.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).