Credit Report Example: How To Read and Understand Yours

Monitoring your credit report can help you build your credit score and spot inaccurate information or identity theft.

A section of federal law called the Fair Credit Reporting Act (FCRA) entitles you to a free copy of your credit report once a year.[1] But once you have that in hand, what then? This article will share a credit report example and help you understand how to read your free credit report.

Our sample credit report provides tips on how to read each section. Whether you want to check on the status of a car loan or student loans, identify negative items on your credit report, see whether you have any liens against you, or find information to help you deal with a collection agency, this is a good place to start.

Key points

- Your credit report contains four main sections: personal information, public records (bankruptcies only, since tax liens and civil judgments stopped being reported in 2018), account information, and inquiries (both hard and soft).

- You can access free credit reports weekly from all three major credit bureaus at annualcreditreport.com, which is the only federally authorized site for free credit reports.

- Hard inquiries from loan applications stay on your credit report for 24 months and affect your FICO score by 10%, but multiple inquiries for the same loan type within 14 to 45 days typically count as just one inquiry.

Table of contents

- Sample credit report

- Sections of your credit report

- How to access your credit report

- What is a credit report used for?

- What if there is an error on your credit report?

- What is the difference between a credit report and a credit score?

- Check your credit report regularly

Sample credit report

Three major credit reporting agencies (Equifax, Experian and TransUnion) track and compile your credit history into a credit report that includes: personal information, public records, account information, and inquiries.

Sections of your credit report

Here is a closer look at what you can expect to see in each section and what you should keep your eye on. Your credit report may look a little different than this example, depending on your individual credit history.

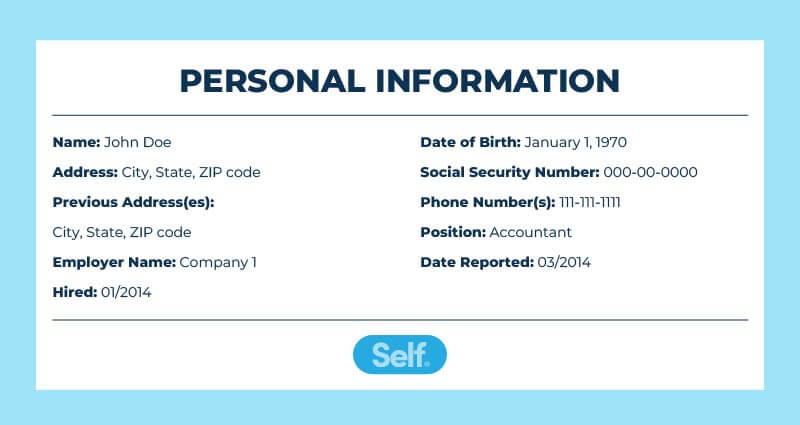

Personal information

This section details who you are, providing basic information that specifically identifies you, including contact information. While this section does not factor into your credit score, it’s important to check that all information is current, otherwise you might be missing important correspondence or be a victim of identity theft. Identifying information can be such things as:

- Your name

- Date of birth

- Social security number

- Current address

- Previous address(es)

- Telephone numbers

- Employment information

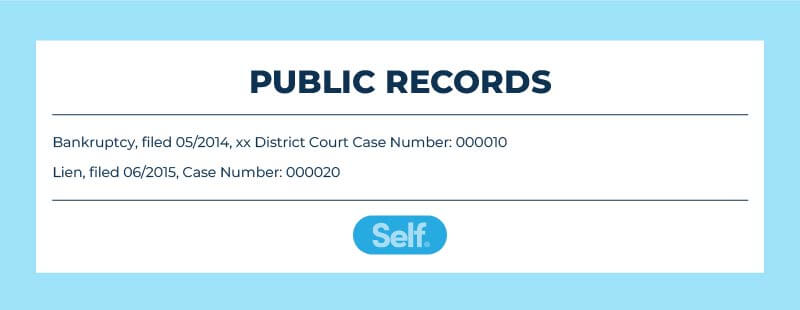

Public record information

Public records that appear on your credit report are limited to financial records: things that could impact your creditworthiness. They don’t include criminal records, speeding tickets or other non-financial data.

Bankruptcy is the only type of public record that appears on credit reports from the three major credit bureaus.[2] Previously, civil judgments and tax liens were also included on credit reports, but the credit reporting agencies stopped including them in 2018.

If you don’t have any negative public records, this section may not appear on your report.

If you do have a bankruptcy on your record in the past seven to 10 years, you can expect to see the following information on your report in this section:

- Bankruptcy type (Chapter 7 or 13)

- Status

- Date filed

- How filed (individually or jointly)

- Reference number

- Closing date

- Court with jurisdiction

- Remarks (either from you or the court)

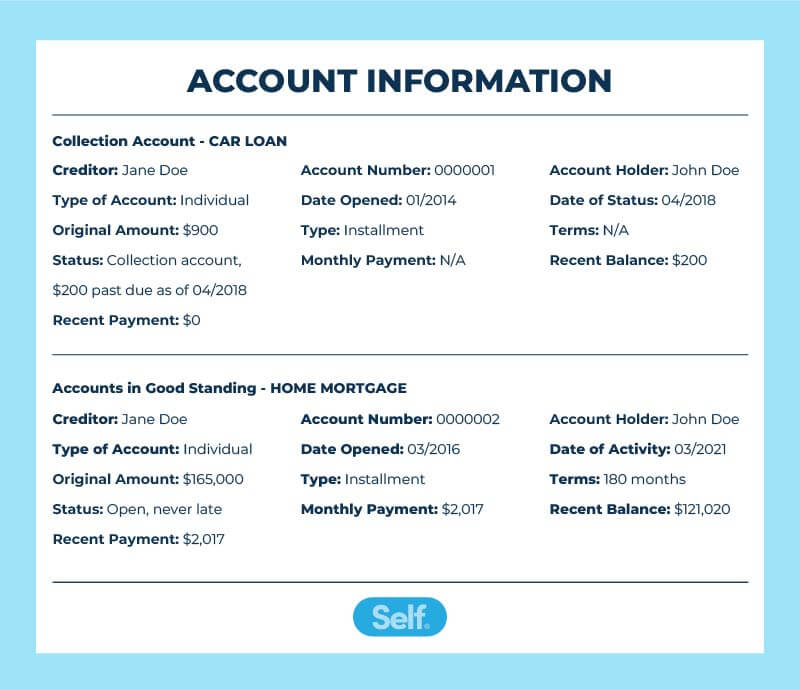

Account information

This section includes your credit history for different accounts, with details on each one. This may include the following information:

- Name of creditor

- Account number (truncated, showing the last few digits)

- Type of account/person(s) responsible (individual or joint)

- Date opened

- Date of most recent activity

- Credit limit or amount of loan

- Status, which can include any of the following:

- Open

- Closed/never late

- Closed; was paid as agreed

- Paid and closed

This section will also show the type of account for each entry, whether it’s an installment loan like a home loan, or a revolving account, like a credit card.

You can scan this section to determine whether you have late payments, or whether anything appears that seems suspicious. Charges you don’t recognize may be the result of fraud or identity theft; if so, disputing them as soon as possible may help you avoid further damage to your credit.

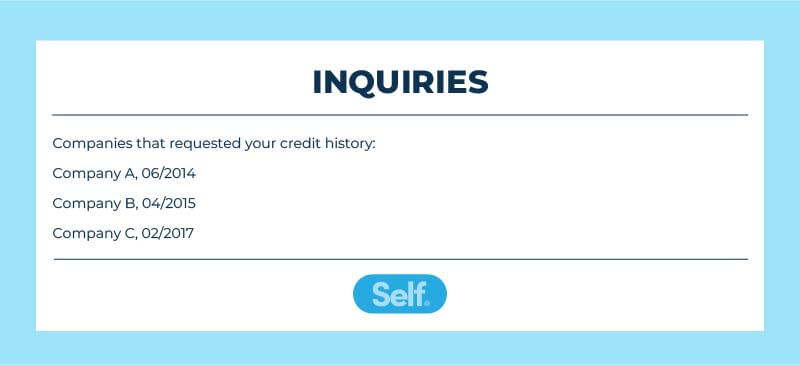

Inquiry information

Credit inquiries fall into two categories: hard and soft pulls. A hard inquiry is recorded whenever you apply for credit, whether it is a credit card account, car loan, mortgage, or another type of credit. Lenders will “pull” your credit report to check your credit information and see whether you qualify for a loan.

Each time this happens, a record of the hard inquiry goes on your credit report and affects your credit score. Hard pulls, also called “new credit,” account for 10% of your FICO® score. [3] If you apply for the same kind of loan several times in a short period of time (within a 45-day window depending on the credit scoring model and loan type), it will typically count as just one hard inquiry, to reflect the fact that you were shopping around for the best rate on a car loan, for example. These multiple hard pulls should not detrimentally impact your credit.[4]

Soft inquiries will appear on your credit report, as well. These include:

- Credit checks by prospective landlords seeking to determine whether to rent to you.

- Checks by potential employers (with your permission they may be able to view your report).

- Your own request for your credit report.

- Requests made for marketing purposes, such as to extend offers of pre-approved credit.

- Credit checks made by current creditors to monitor your recent activity.

Both hard and soft inquiries remain on your credit report for 24 months, but only hard inquiries are reflected in your credit score.

How to access your credit report

First, you need access to your credit report to know it's there. The three major credit bureaus now permanently offer free weekly credit reports, which you can access by visiting annualcreditreport.com.

You can also order a copy of your credit reports by calling (877) 322-8228 or by downloading a form from annualcreditreport.com and sending it to Annual Credit Report Request Service, PO Box 105281, Atlanta, GA, 30348-5281.[5]

You can get a copy of all three credit bureaus’ reports at the same time, or you may request them separately at different times to monitor them.

What is a credit report used for?

Your credit report provides a comprehensive overview of your credit history that you can use to monitor where you stand and lenders can use to determine your creditworthiness.

A credit report can be used to evaluate whether or not to extend you credit, and if so, at what rate of interest. Businesses can use it as a factor in weighing whether to extend a job offer or offer you insurance, and landlords can consider its contents in deciding whether to rent to you.[1]

Credit reports are also used to determine credit scores compiled by Fair Isaac Corporation (FICO®) and VantageScore, which use slightly different methods to compile their figures. [4]

What if there is an error on your credit report?

If you do find errors in your credit report, it is important to dispute them so they do not damage your credit score and affect your ability to obtain loans and/or favorable interest rates.

Errors can come in many forms, in addition to the transposed numbers and personal identity issues already discussed. Account balances may be off, closed accounts may still appear as open, accounts may be duplicated (so you get dinged twice for late payments, for example), payments may not have been recorded, or a bankruptcy may not be marked as discharged.

If you find an error in your credit report, you can dispute it yourself by contacting the credit bureau where the error appears. It is helpful to gather supporting documentation, such as letters from creditors showing correct amounts and account statuses, bankruptcy discharge papers, deferment or forbearance agreements, or police reports and FTC identity theft reports in the case of fraud.

You can file a dispute online or by mail. Once you’ve made your report, it’s a good idea to follow up with creditors and credit bureaus to ensure the errors have been fixed.

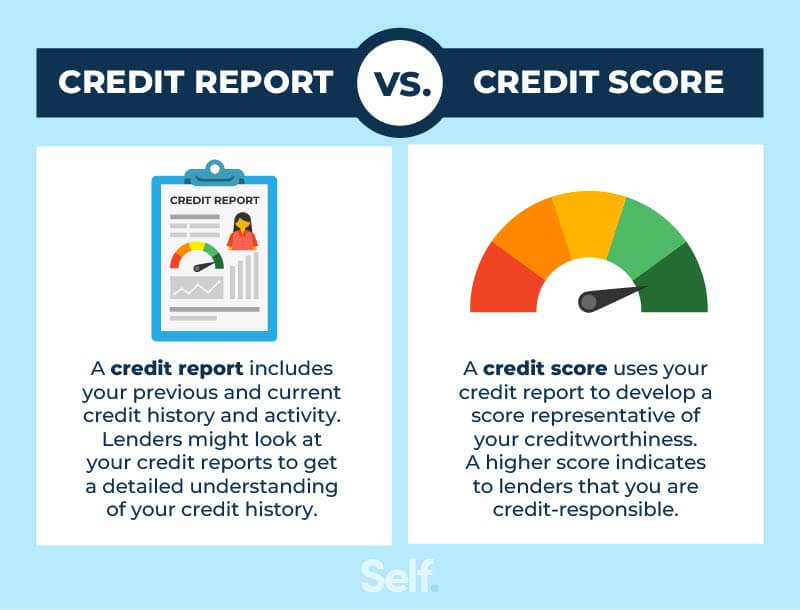

What is the difference between a credit report and a credit score?

It’s common to confuse your credit report with your credit score, but they are two different things. A credit report is a comprehensive record of your credit history. Your credit score, by contrast, is simply a three-digit number that measures how well you manage your credit.

Check your credit report regularly

Obtaining a copy of your credit report is a good first step to understanding where you stand and what you need to address in your personal finances. The next step is understanding your report so you can know what issues to address and which ones to dispute, if necessary.

Sources

- Federal Trade Commission. “Free Credit Reports,” https://www.consumer.ftc.gov/articles/free-credit-reports. Accessed December 31, 2021.

- Experian. “Public Records That Can Appear in Your Credit Report,” https://www.experian.com/blogs/ask-experian/public-records-that-appear-on-your-report/. Accessed December 31, 2021.

- MyFICO. “New Credit.” https://www.myfico.com/credit-education/credit-scores/new-credit. Accessed January 22, 2026.

- Experian. “The Difference Between VantageScore and FICO Scores,” https://www.experian.com/blogs/ask-experian/the-difference-between-vantage-scores-and-fico-scores/. Accessed on January 7, 2026.

- Consumer Financial Protection Bureau. “How do I get a copy of my credit reports?” https://www.consumerfinance.gov/ask-cfpb/how-do-i-get-a-copy-of-my-credit-reports-en-5/. Accessed December 31, 2021.

About the author

Jeff Smith is the VP of Marketing at Self Financial. See his profile on LinkedIn.

About the reviewer

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.