What Bills Help Build Credit?

You may know that failing to pay bills can ding your credit, but the opposite can also prove true — simply paying your bills on time may build your credit. According to FICO®, the single largest factor influencing your credit score is your payment history, which can now include your monthly bills.[1] This article addresses which bills can help build credit and what to watch out for along the way.

Key points

- Traditional credit products, such as mortgages, auto loans, student loans, and credit cards, may help build credit when reported.

- Rent and utility bills may help build credit when reporting to credit bureaus using a rent reporting service.

- Medical bills don't typically build credit. However, unpaid medical debt over $500 can negatively impact your credit if it is sent to collections.

What bills impact your credit score?

Traditionally, credit reports included payments on two types of accounts: revolving credit (such as credit cards), installment loans (such as car loans and mortgages), and collection accounts. Recently, however, some credit scoring models have begun to incorporate payments on other types of bills — as long as service providers report that information. While not all companies share positive payment data with the major credit bureaus, you can take steps to have your history of on-time bill payments included.[2]

Utility bills

Paying your monthly utility bills — water, gas, trash, electric, streaming services, and internet — can help you build your credit if those payments are paid on time as agreed and are reported to the credit bureaus. Unfortunately for consumers who pay on time, utility companies generally don’t report payment information to the credit bureaus (unless your account is charged off or sent to a collections agency, which could then hurt your credit). However, you can register for services like utility bill reporting for a monthly fee with the Self utility service that helps you add positive utility payment histories to your credit file, potentially benefiting your credit score.[3]

Rent payments

Like utility bills, on-time rent payments may build your credit if the credit bureaus receive that information. However, like utility companies, landlords and rent management companies rarely report rent payments. Although you can’t submit this information yourself, you can hire third parties to report your rental payment history to the credit bureaus. Some third-party services help you report rent, utilities, cell phone bills, and more.

Self offers a rent reporting service that reports positive rent payments to help tenants build credit. Only on-time payments are reported, which may help renters build credit without the risk of negative marks.

Keep in mind that not all scoring models include rental information in their calculations. Although VantageScore® plus FICO® 9 and FICO® 10 do consider it, these are not commonly used scoring models.[4]

Mortgage payments

While taking out a new loan may temporarily drop your credit score, responsibly managing a large account like a mortgage can play an important role in helping you build credit. In addition to contributing to your credit mix, typical home loans often have long repayment periods that can eventually build your credit history if you pay on time as agreed.[5] Of all credit scoring factors, payment history has the biggest impact. Making on-time mortgage payments can likely bump up your credit score, while missing payments or paying late can cause it to fall.[1]

Medical bills

Medical bills won’t build your credit because medical providers typically don’t report to the credit bureaus. However, unpaid medical debt can hurt your credit.

Unpaid medical bills over $500 that have gone into collections appear on your credit report. The three major credit reporting agencies made changes to medical debt reporting in 2022 and 2023 to help consumers. As of July 1, 2022, paid medical collection debt no longer appears on credit reports. Additionally, the time period before unpaid medical collection debt appears on a consumer's report increased from six months to one year, giving consumers more time to work with insurance and healthcare providers to address their debt. As of April 2023, medical collection debt with an initial reported balance under $500 has been removed from credit reports, eliminating nearly 70 percent of collection accounts from consumer credit files.[6]

Student loan payments

Like any other loan, student loans can affect your credit both positively and negatively. Although making late payments or defaulting on your account can damage your credit, student loans can also help your credit score. As you make your monthly on-time payments, the amount owed goes down and your credit score should be positively impacted. Managing your student loan responsibly may have long-term benefits — as long as you make on-time monthly payments and pay off your loan on or before by the final due date, your student loan can appear on your credit report for 10 years after payoff.[7]

Auto loan payments

Auto loan payments can also potentially impact your credit score. Along with student loans and mortgage loans, auto loans are a type of installment loan — a type of credit that requires regular payments over a set period. Assuming you make your on-time monthly payment each month, you may eventually see a bump in your credit score. However, because payment history gets factored heavily into your credit score, if you don’t make regular timely payments, you could see a negative impact on your credit score.[1]

Credit card payments

Credit cards offer one of the more popular ways to build credit, and credit cards can provide benefits to consumers with a wide range of credit scores. If you have a strong credit history, you may qualify for multiple credit card options, and card issuers may offer you a lower APR than typically available to those with a bad credit score. Consumers with poor credit might look into a secured credit card — secured cards require a security deposit to open.[8]

In either case, paying your credit card bills on time can affect your payment history, and keeping credit card accounts open as well as keeping your credit card balance low can both help to maintain a low credit utilization rate. All of these factors play a part in improving your credit.[1]

Cell phone bills and financing

Financing a cell phone can potentially impact your credit score if you go through phone manufacturers like Apple and Samsung which use banks for the financing. Because wireless carriers generally don’t furnish data to credit reporting agencies, however, financing a cell phone through your carrier won’t likely affect your credit. For the same reason, paying your monthly phone bill probably won’t impact your credit either (unless you don’t pay your bill and eventually your account gets sent to collections).

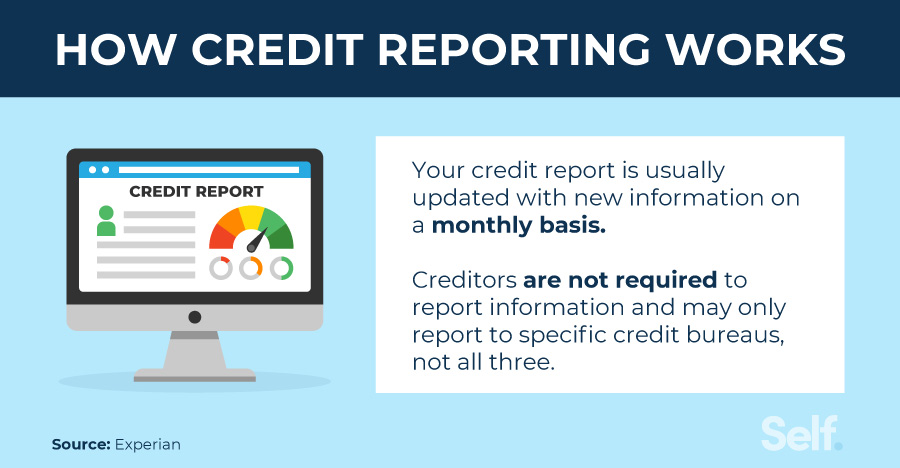

How credit reporting works

A credit report contains a myriad of information including personally identifiable information like your name and social security number, how you have managed your credit accounts, how many credit inquiries you have and their type, and public record and collections information.[9] Three major credit bureaus — Experian, Equifax, and TransUnion — compile data submitted by lenders and debt collectors and that information is then used to calculate a credit score. Your FICO® credit score takes the following factors into consideration:[10]

- Payment history (35%): The single biggest factor in your credit score, your history of payments — both positive and negative — makes up over a third of your score.

- Amount of debts owed (30%): The second most important factor calculates the amount of available credit that you are currently using. Using too much of your available credit can be interpreted by lenders that you’re overextended.

- Credit history (15%): This category considers the age of your accounts — oldest account, newest account and average age of all accounts — in calculating your credit score. In general, more established credit histories can help build your credit score in this category.

- Credit mix (10%): A good credit score often shows a diverse mix of credit types, from credit cards and retail accounts to mortgages and installment loans.

- New credit accounts (10%): Opening several new accounts — or even applying for them — might have a negative impact on your credit score, especially if you have a limited credit history.

[1]

How to build credit

If you have a poor credit history, or no credit history at all, you may need to take steps to prove to lenders, landlords, insurers and other parties that you will pay your bills. This concept of creditworthiness could impact your ability to take out loans, open credit cards or obtain a mortgage to buy a house, as well as the interest rate and other terms related to your account.

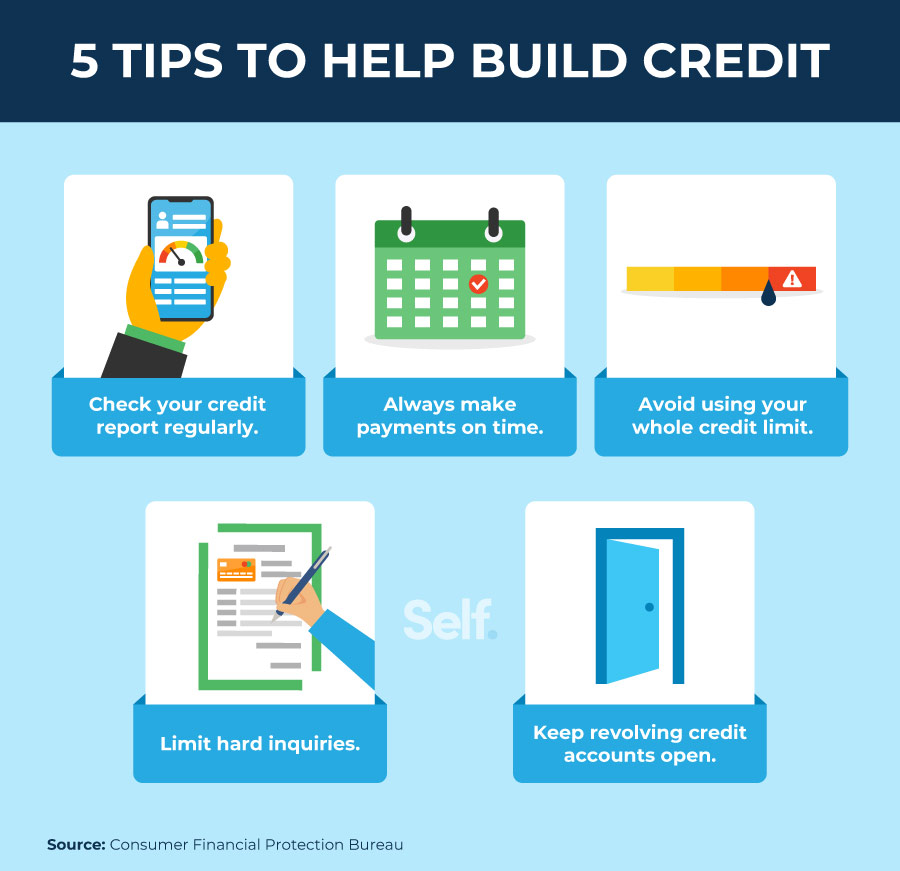

The following tips can help you build or rebuild credit:

- Check your credit report regularly: Knowing what’s in your credit report enables you to keep tabs on financial issues, take steps to correct errors and establish a baseline for your credit-building efforts.

- Always make payments on time: Since payment history counts for over one third of your credit score, you should prioritize making on-time payments.

- Avoid using your whole credit limit: To maintain a healthy credit score, avoid using over 30% of your total available credit.

- Limit hard inquiries: Applying for new credit accounts may result in hard inquiries, which might temporarily ding your credit score.

- Keep revolving credit accounts open: Both open and closed accounts on your credit report can affect your score, but closed paid accounts generally drop off by the 10-year mark. Sometimes it makes sense to close an account (to avoid an annual fee, for example), but sometimes it doesn’t: since your credit score includes the average age of accounts, credit mix and current credit utilization ratio (CUR), keeping accounts in good standing open may actually benefit you more. Having a credit card open with a zero or low balance offers you a higher total credit limit across all accounts. So when you calculate your CUR (your total revolving debt divided by your total credit limits), having a higher total credit limit may help lower your CUR.[11]

Credit building takes time and consistency

You can’t build credit overnight — bettering your score and improving personal finance takes time, patience, effort and responsible financial management. If you have no credit history or low credit scores, Self’s Credit Builder Account offers an ideal starting point to build or rebuild credit. Making on-time loan payments each month helps build positive payment history, a crucial ingredient in a good credit score.

*Results vary. You may not receive an improved credit score. Not all lenders use scores impacted by rent/utility payments.

Sources

- MyFICO. “What's in my FICO® Scores?,” https://www.myfico.com/credit-education/whats-in-your-credit-score.

- Experian. “What Kinds of Bills Affect Credit Scores?” https://www.experian.com/blogs/ask-experian/what-kinds-of-bills-affect-credit-scores.

- Credit.com. “How to Add Rent and Utilities to Your Credit Report,” https://credit.com/blog/how-to-add-rent-and-utilities-to-your-credit-report.

- U.S. News & World Report. “How Can You Get Credit for Paying Rent?” https://money.usnews.com/credit-cards/articles/how-can-you-get-credit-for-paying-rent.

- Rocket Money. “Does Buying a House Help Your Credit Score?” https://www.rocketmoney.com/learn/debt-and-credit/buying-house-help-credit-score.

- Equifax. “How Does Medical Debt Impact Your Credit Score?,” https://www.equifax.com/personal/education/credit/score/articles/-/learn/can-medical-debt-impact-credit-scores/.

- Experian. “Do Student Loans Help Build Credit?” https://www.experian.com/blogs/ask-experian/do-student-loans-help-build-credit.

- Experian. “How to Use a Credit Card to Build Credit,” https://www.experian.com/blogs/ask-experian/how-to-use-a-credit-card-to-build-credit.

- MyFICO. “What’s in Your Credit Report?” https://www.myfico.com/credit-education/whats-in-my-credit-report.

- Consumer Financial Protection Bureau. “Consumer Reporting Companies.” Consumer Tools – Credit Reports and Scores, updated March 13, 2025. https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/consumer-reporting-companies/companies-list/.

- MyFICO. “How to Build Credit,” https://www.myfico.com/credit-education/credit-scores/how-to-build-credit.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.