How to Get Approved for a Car Loan

If your goal is to finance a new or used vehicle in the near future, it’s important to understand how to get approved for a car loan. Find out how to qualify for an auto loan.

Read through our guides and information related to car financing across the U.S. We explore everything from bankruptcy to loan options and trade-ins.

Demystifying interest rates, costs, and financing options

If your goal is to finance a new or used vehicle in the near future, it’s important to understand how to get approved for a car loan. Find out how to qualify for an auto loan.

Before buying a car, it’s important to understand how car loan interest works. Learn about auto loan interest rates and payments here.

Want to know how much a car loan will cost in interest based on your credit score? Find out how much you’ll pay, plus what you could save.

Unsure if you're being offered a good interest rate on a car loan? We break down APRs and interest rates so you’re ready to negotiate for the best deal.

Analyzing the lifetime ownership expenses of electric and gasoline vehicles

After 10 years, the ownership costs for the vehicles we analyzed are as follows:

This includes the purchase price of each vehicle which is split over the first 6 years.

Read full articleFrom transportation expenses to post-bankruptcy financing

This study uncovers the cost per mile for transportation across America. From car travel, to cab rides and public transportation, how do cities compare?

The price of electric cars vs gas cars can be confusing. We’ve taken hundreds of data points to give you an accurate state-by-state comparison.

There’s no specific minimum credit score requirement to lease a car. Your approval requirements can vary from dealership to dealership.

If you're considering trading in a car with an outstanding loan balance, here's what you need to know to make sure you protect your finances and credit.

Unpack the jargon: tap to reveal straightforward definitions

Equity is the difference between a car’s current market value and the outstanding loan balance.

The Annual Percentage Rate (APR) is the additional cost you pay for borrowing money each year, including fees, expressed as a percentage.

Depreciation is a reduction in the value of an asset, like a car, over time, typically due to wear and tear.

A co-signer is someone who takes on the responsibility of paying back a loan on your behalf if you do not. This could be a parent, close family member, or friend.

A down payment is an initial, upfront payment that you make towards the total cost of a car. The higher the down payment you put down, the less money you’ll need to borrow with a loan.

The interest rate on a car loan is the cost you pay each year to borrow money expressed as a percentage. Unlike APR, the interest rate does not include other fees.

An electric vehicle is any vehicle that is powered by an electric motor that draws electricity from a battery and can be charged from an external source.

A gas vehicle is a motor vehicle that is powered by a spark-ignited internal combustion engine, fuelled by gasoline.

A loan term or duration is the whole length of an auto loan which you will make repayments for, typically expressed in months.

If your car is worth less than the amount you still have left to pay on your auto loan, then you have negative equity. For example, if your car is only worth $6,000 but you still have $7,000 left to pay on your auto loan, you have negative equity of $1,000.

The loan-to-value ratio (LTV) is the total value of your loan divided by the actual cash value (ACV) of your car, usually expressed as a percentage. For example, if your car is worth $7,000 and your loan balance is $5,000, your LTV would be 71%.

A car’s fuel efficiency is the measure of how much a car will convert energy from fuel into kinetic energy to travel. The more energy contained in the fuel, the greater the fuel efficiency of the car. Cars with greater fuel efficiency require less gas to travel a given distance.

Demystifying car financing and ownership: your questions answered

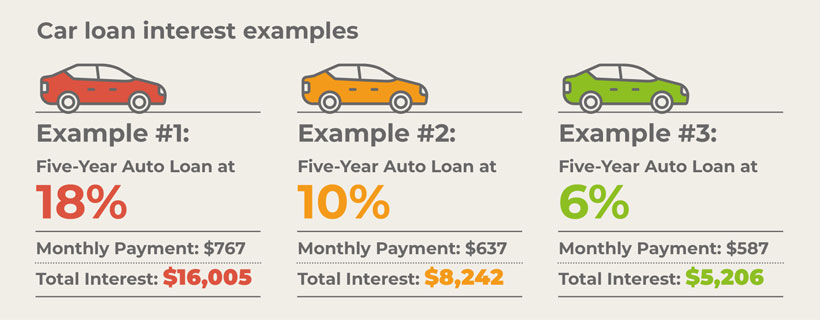

Interest rates on car loans can be impacted by several factors including your credit score, the down payment you make, the loan term, and external economic factors like inflation.

Paying for car insurance doesn’t directly build credit as these payments are not reported to credit bureaus. However, if you used a credit card to pay for your car insurance and paid it off on time, you could indirectly help build your credit by using your credit card and paying it off.

Typically, people with higher credit scores might be able to get lower interest rates on their car loans, while people with lower credit scores might pay more interest. Your credit score can also impact whether a lender will approve you for a car loan at all.

You can still get a car loan if you have bad credit, but you might pay more interest on your loan. There are some steps you can take to increase your chances of being approved for a car loan such as making a larger down payment, trading in an old vehicle, or asking someone you trust to co-sign the loan.

Yes, you can get a car loan after declaring bankruptcy, but getting approved might be difficult. Your credit score is one of the main factors lenders consider when deciding to accept you for a loan and bankruptcy can negatively impact your credit.

Some things you can do to improve your chances are to try to lift your credit score where possible, pay a higher down payment, and consider getting a cosigner for the loan.

If you’re struggling to make the payments on your auto loan, a voluntary repossession means you inform your lender that you can no longer make the payments and return your car. The lender can then sell the car and put the money towards your outstanding balance.

A repossession, even if it’s voluntary, counts as a default on your auto loan, and this may have a negative impact on your credit score and can remain on your credit report for up to seven years.

Yes, you can pay off your car loan in a shorter time than your loan term by paying slightly more than your monthly repayment, making one-off large payments or via bi-weekly half payments instead of monthly ones.

Consider your financial situation before paying off your auto loan early, as it may benefit you more to pay off other debts with higher interest rates instead.

Minimizing your auto financing costs

Get to know the talented minds crafting our content

Explore our tools and calculators, designed to simplify your financial decisions and provide clarity

Own a car and hoping to get a loan? Using your car as collateral to borrow is certainly possible. Find out everything you need to know here.

Getting approved for a loan after bankruptcy can be difficult. Despite this reality, it may be possible to get a car loan after bankruptcy by following these tips.

Trying to figure out how to finance purchasing a car? Here's everything you need to know from credit score to loans.

How to Get a Credit Card with No Credit

It’s possible to get a credit card with no credit, but you need to know which types of accounts to apply for (and which applications to avoid as well).

Download