Does Getting A Mortgage Preapproval Hurt Your Credit Score?

Getting a mortgage preapproval can hurt your credit score slightly because it is a hard inquiry, but the advantages of having one may outweigh this slight negative. If you are considering applying for a mortgage loan, this guide helps you determine what impact getting preapproved may have on your credit and whether you should obtain a preapproval letter during your homebuying process.

How does a mortgage preapproval work?

The mortgage preapproval process is similar to that of getting any kind of loan. You submit a mortgage application to a lender, who reviews it to determine if you qualify for the mortgage. The loan officer looks at your credit score, finances, income history, debts, assets and anything else relevant to your qualifications for a loan.[1]

Some of the documents you may need to provide include a proof of identity, income verification such as pay stubs and bank statements, and a record of debts and assets. You will also give the lender authorization to pull your credit report. You may also need to prove that you have enough money for a 5% to 20% down payment. Some community banks and certain government backed loans like FHA may have lower down payment requirements.[1]

Keep in mind that preapproval differs from being prequalified for a mortgage. Being prequalified means you have a ballpark estimate of what you can borrow so that you know what price range to stick to. Being preapproved details a specific amount and interest rate.[1]

How mortgage preapproval affects your credit

A mortgage preapproval activates a hard credit check that can reduce your credit score by a few points.[1] You may see inquiries referred to as credit checks or credit pulls, but they all mean the same thing. Credit bureaus define two types of credit inquiries and each have different impacts on your credit:

A hard inquiry occurs when a lender evaluates your credit before making a decision to lend you money, whether it be for a home loan, credit card, or other extension of credit. Although a hard inquiry can lower your credit score by a few points, the damage from just one is generally temporary. A hard inquiry typically falls off your credit report in two years.

A soft inquiry is triggered when a person or company checks your credit to prequalify you for a new credit offer or to run a background check. Soft credit inquiries won't affect your credit score.[2]

You can shop around for the best rate and get multiple preapprovals for a mortgage. As long as your rate shopping for a mortgage loan occurs within a specific window it will only be counted as a single inquiry in your credit score. The length of time you can rate shop depends on the FICO® scoring model used by the lender.[3] This way potential homeowners and first-time homebuyers can find the best mortgage rates available without risking their own credit.[4]

Prequalified vs. preapproved mortgages

Being prequalified and preapproved for a mortgage impacts borrowers in different ways. So understand the aspects of each so that you know which type you should seek from different lenders:

A prequalified mortgage offers a general estimate of what you may be able to borrow based on your financial situation. However, a prequalification does not involve a full investigation into your credit history, which means that a prequalification generally does not affect your credit score

A preapproved mortgage provides specifics on what the prospective homebuyer can qualify for in terms of loan amount and interest rate and generally speeds up the buying process. This option involves a full application and inquiry into your credit history, which because a hard inquiry is made can lower your score temporarily.[2] [5]

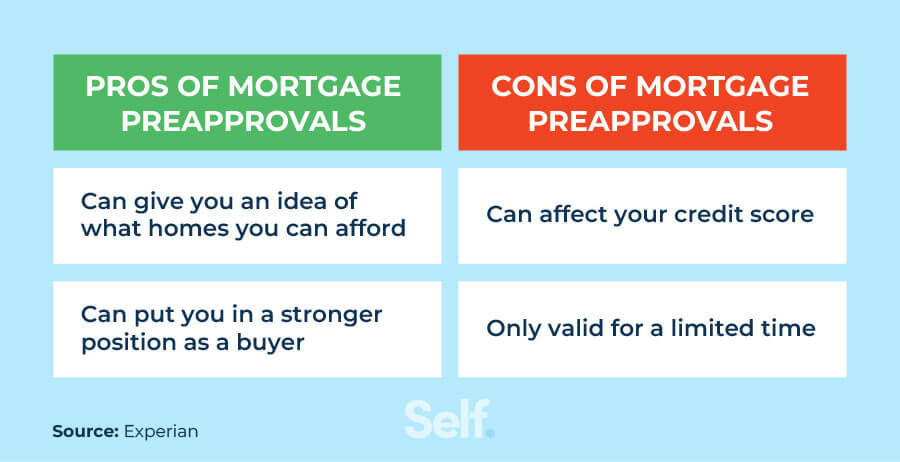

Pros of mortgage preapproval

A mortgage preapproval gives you a few clear advantages.

It can give you an idea of what homes you can afford

A preapproval tells you in specific terms how large of a loan you would qualify for, what your monthly payments would be and how much would be required for a down payment. This may give you some idea of how much home you can afford so you can better target your search. Be aware of your financial situation and consider the complete overall cost of a home.[2]

It can put you in a stronger position as a buyer

Being preapproved puts you at a strong position as a buyer because it indicates you are ready to buy and already well-advanced in the buying process. It shows that a lender has reviewed your creditworthiness and income and has determined that you are ready to purchase a home and will have the finances to do it.[6]

Cons of mortgage preapproval

While you gain advantages with a mortgage preapproval, you may also experience some drawbacks worth considering.

It can affect your credit score

A mortgage preapproval triggers a hard inquiry on your credit, which may lower your credit score temporarily. Keep in mind, however, that one or two hard inquiries typically won’t have a big impact on your credit score. Plus, you have a 45-day timeframe with newer FICO® scoring models to apply to numerous mortgage lenders with it only counting as one hard inquiry.[1]

Only valid for a limited time

Preapprovals won’t last forever. Your financial situation can change significantly over the course of a few months, which is why a preapproval is typically only valid for about 90 days — in some cases only 30 days. You can request an extension on the preapproval if you need more time, but be aware you may have already paid fees. Typically, mortgage preapprovals include an application during this process, which can cost you hundreds of dollars — and it may cost you again to restart that application process if your preapproval letter expires.[1]

Should you get preapproved?

Although a mortgage preapproval is not required, it can indicate how serious you are about buying a home. Prior to starting the process, however, evaluate your personal finances before future lenders do. Check what your credit report says and try to resolve any issues to maximize your chances of success. You don’t want any surprises preventing you from purchasing a home. With a preapproval letter in hand, your odds of landing that dream home may increase in your favor. However, don’t just rely on the preapproval letter. Evaluate your finances, specifically your current budget and any ongoing debt responsibilities. This helps you determine whether you can add the expense of a new home to your current financial situation.

Sources

- Experian. "When Should You Get Preapproved for a Mortgage?" https://www.experian.com/blogs/ask-experian/when-to-get-preapproved-for-mortgage. Accessed June 20, 2022.

- Experian. "What Are Inquiries On Your Credit Report?" https://www.experian.com/blogs/ask-experian/credit-education/report-basics/hard-vs-soft-inquiries-on-your-credit-report. Accessed June 20, 2022.

- FICO®. “Credit Checks: What are credit inquiries and how do they affect your FICO® Score?” https://www.myfico.com/credit-education/credit-reports/credit-checks-and-inquiries. Accessed October 17, 2022.

- Consumer Financial Protection Bureau. "What exactly happens when a mortgage lender checks my credit?" https://www.consumerfinance.gov/ask-cfpb/what-exactly-happens-when-a-mortgage-lender-checks-my-credit-en-2005. Accessed June 20, 2022.

- Experian. "How Can I Get Prequalified for a Mortgage Loan?" https://www.experian.com/blogs/ask-experian/how-do-i-prequalify-for-a-mortgage. Accessed June 20, 2022.

- Experian. "What Is a Preapproval Letter?" https://www.experian.com/blogs/ask-experian/what-is-a-preapproval-letter. Accessed June 20, 2022.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).