How to Raise Your Credit Score by 200 Points

Reviewed by: Ana Gonzalez-Ribeiro, AFC®

Published on: 10/06/2022

Last Updated: 10/06/2022

FICO® and VantageScore® create many of the credit scores that lenders use in the United States. Most of those credit scores range from 300-850. The higher your credit score climbs on this common numerical scale, the better. Good credit scores can help you qualify for financing (like loans and credit cards), lock in better interest rates, and perhaps even save money on your auto insurance premiums.

If your credit score is on the lower end of the range above, you may need to see a lot of improvement before you’ll be eligible for the best deals lenders have to offer. Bad credit scores might even disqualify you from certain loans altogether—and that could be a problem if you’re trying to purchase a home, a vehicle, or finance another major expense.

On the bright side, if you’re unhappy with your current credit score, you can take actions to try to improve it. You might even be able to raise your credit score by 200 points or more with the right plan.

Of course, a 200-point credit score increase isn’t something that will happen overnight for most people. Depending on your situation, it could take months or even years to bring about such a significant credit score shift. Yet each step in the right direction could have a positive impact on your financial life.

What’s the impact of a 200-point credit score increase?

Improving your credit score by 200 points has the potential to be life changing. The previous statement might sound dramatic, but it’s true. Here are two examples to illustrate how much a 200-point credit score increase could benefit you.

From 450 to 650

Imagine that you have a 450 FICO® Score. This credit score range is considered to be “very poor” by lenders and others who may review your credit information.

With a bad credit score, you will probably have trouble qualifying for many types of financing such as auto loans, credit cards, and personal loans. And although it’s sometimes possible to buy a house with bad credit, with a 450 FICO Score you’ll most likely be ineligible for a home loan. In fact, you might have trouble renting an apartment with a low credit score.

Now, let’s assume that you work hard to improve your credit score to 650. In this scenario, you’re moving from a score in the “very poor” range to a “fair” credit score.

Improving your credit score from bad to fair means that you’re a better risk in the eyes of lenders and others. With fair credit, you should have an easier time qualifying for some types of financing. But since lenders may still consider you to be a subprime borrower at a 650 FICO Score, higher interest rates and fees are common.

From 550 to 750

Gaining a 200-point credit score increase could be even more impactful if your starting credit score is a bit higher. Taking a 550 FICO Score and improving it to 750, for example, has the potential to save you thousands of dollars or more when you obtain financing.

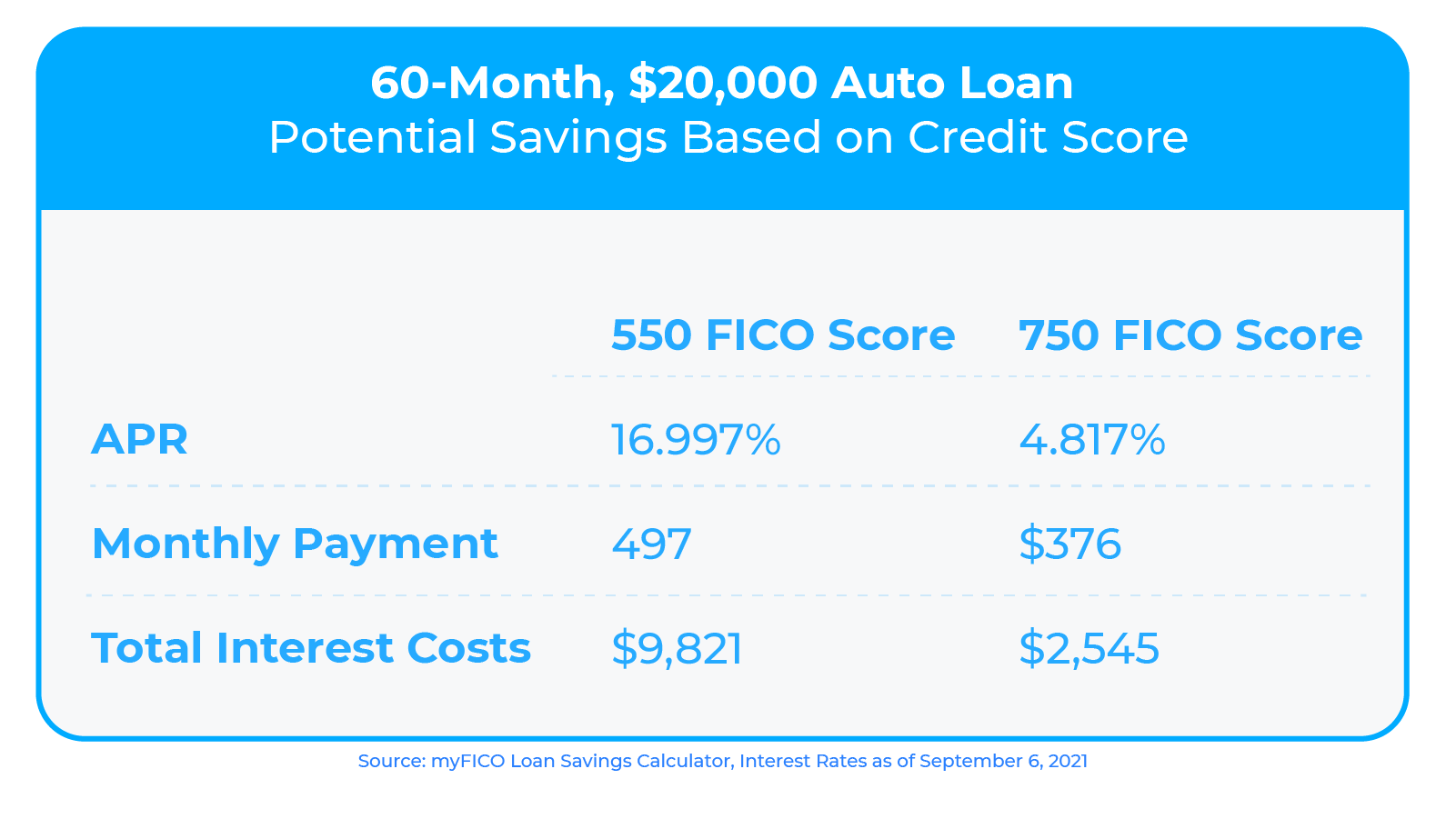

Consider the idea of applying for a car loan with a “poor” FICO Score of 550. Let’s imagine that you decide to finance a new $20,000 vehicle using a 60-month auto loan. Based on current estimated rates, you might pay $497 per month for that car loan with a 550 FICO Score. But if your FICO Score increased to 750—a score FICO classifed as “very good”—the monthly payment for that same vehicle could potentially drop to $376. Over a 60-month loan, the 750 FICO Score could save you more than $7,276 in interest fees.[1]

Below is a deeper look at the hypothetical loan savings you might enjoy in this situation with a credit score increase from 550 to 750.

How long does it take to improve your credit score?

If you’re working hard to improve or build your credit score, it’s natural to wonder how long the process will take. However, there’s no one-size-fits-all answer to the question.

In certain situations, you might be able to see some credit score improvement in 30 days or less. Yet for a significant credit score increase, patience tends to be required. It’s not unusual for months or years to pass before a credit score can climb hundreds of points.

The amount of time it takes for your credit score to improve will depend on two primary details:

- The factors that are holding your credit score back.

- The steps you’re able and willing to take to address those issues.

No one can know ahead of time the exact length of time needed to improve their credit score. There are too many variables at play. But your credit score is based on the information on your credit report. So, if you become familiar with the details on your report and how credit scoring models may interpret that information, you can have a better idea of how to achieve your desired results.

What factors affect your credit score?

When you read your credit report, you’ll find that it contains many details about your credit obligations—both past and present. Information such as the date your account was opened, your payment history, account balances, credit limits, and more can impact your credit score to varying degrees. If you want to raise your credit score by 200 points, try focusing on factors that impact your score and try to improve in those areas.

Payment history

The purpose of a FICO Score is to predict the likelihood that you’ll default on a credit obligation (aka go 90 days late or more) in the next 24 months.[2] So, it makes sense that your past payment history has the biggest influence over your FICO Score.

Thirty-five percent of your FICO Score is based on your payment history. This credit score category considers details like:

- The number of accounts you’re paying as agreed.

- The number of past-due items on your credit report.

- How much you owe on delinquent accounts (including collection accounts).

- The severity of past or present late payments (e.g., 30-days, 60-days, 90-days late, etc.).

- How long it’s been since a late payment, collection account, or public record showed up on your credit report.

If you want to earn the best credit score possible within this category, focus on paying your credit obligations on time. There should be no exceptions. Even an occasional late payment could set back your credit improvement efforts.

Late payments and most other negative items may stay on your credit report for up to seven years. On a positive note, however, any past delinquencies on your credit report should affect your credit score less with the passage of time.

Amounts owed

The debt you owe, especially your credit card debt, can also have a meaningful impact on your FICO Score. There are several factors that play a role in this area of your credit score, but the most important is your credit card utilization rate.

Credit utilization describes the percentage of the credit card limits you are using. If you have a total of one credit card with a $1,000 limit and you’re using half of that limit (aka you have a $500 balance), your credit utilization rate is 50%. In terms of your credit score, a lower credit utilization rate of 30% or less is ideal.

Aside from your credit utilization rate, other factors that impact your FICO Score in this category include:

- The amount you owe on all credit obligations.

- How much you owe on different types of accounts (e.g., credit cards, installment loans, etc.).

- The number of accounts with balances on your credit report.

One of the most actionable ways to try to improve your credit score is to pay off your credit card balances. Doing so might boost your credit score in two ways—by lowering your credit utilization rate and reducing the number of accounts with balances on your credit report. And, of course, paying down credit card debt can save you a great deal of money in the process.

Length of credit history

The longer you pay your credit obligations on time, the more potential there is for you to see improvement in your credit score. Those who are newer to credit, by comparison, are more likely to have problems in this area. Because your length of credit history can help lenders predict your future credit risk, it’s worth 15% of your FICO Score.

Some of the details a FICO scoring model will consider in this category are as follows.

- The age of the accounts on your credit report (e.g., oldest account, newest account, and average account age).

- The amount of time that has passed since you last used an account on your credit report.

Time is your friend when it comes to this part of your credit score. But if you have a friend or family member with an older credit card account, you might consider asking for a favor. If your family member or friend adds you as an authorized user onto a credit card that was opened years ago, there’s a chance it could help to increase the average age of accounts on your report, and perhaps your credit score as a byproduct. (Of course, it’s important that the credit card has on-time payment history and low credit utilization as well.)

New credit

Opening too many credit accounts in a short period of time, or even simply applying for too much new credit, could damage your credit score. Only 10% of your FICO Score is based on these details, but it’s still important to understand that hard credit inquiries could impact your credit score in a negative way.

Certain hard inquiries, however, will not affect your credit score at all. For example, you can rate shop for mortgages, auto loans, and student loans and if you keep your credit inquiries contained to a 14-45 day window they should only factor into your FICO Score once.

If you hope to improve your credit score in this category, avoid applying for new credit in excess. As far as any hard inquiries that are already on your credit report, they have a short shelf life in terms of credit score calculation. Once a hard credit inquiry is 12 months old, it will no longer affect your FICO Score.

Credit mix

The final category of information you want to pay attention to in terms of credit scoring is the mixture of accounts on your credit report. This area of your credit report accounts for 10% of your FICO Score.

A healthy credit mix can benefit you. But if you lack diversity where accounts types are concerned, you might miss out on potential points.

Within this credit report category, FICO will consider factors like:

- Whether you have experience managing revolving accounts (e.g., credit cards, lines of credit, etc.).

- Whether you have experience managing installment accounts (e.g., student loans, auto loans, mortgages etc.).

Adding missing account types could potentially benefit you within this credit score category, but you should proceed with caution. Opening a new credit builder loan because you lack installment accounts might be a good move. Taking out an expensive car loan and going into debt for the sole purpose of building credit, on the other hand, is probably a bad idea.

Summary of credit improvement tips

Below is a summary of the credit improvement tips from each of the five categories above.

- Avoid any future late payments that could damage your credit score.

- Pay down credit card debt in an effort to reduce your credit utilization rate.

- Consider asking a friend or family member to add you as an authorized user to a well-managed, older credit card account.

- Don’t apply for an excessive amount of new credit in a short period of time.

- Consider whether you should open new, positive credit accounts.

Smart credit management habits can often lead to higher credit scores over time—perhaps even eventually a 200-point increase.

Is there a quick fix for repairing credit?

In most cases, repairing your credit is a process that will require time and consistent effort. Disputing credit reporting errors aside, there’s no quick fix for repairing legitimate, damaged credit history.

Still, you can take steps with the potential to impact your credit score for the good. Paying down credit card balances, strategically opening new accounts, and avoiding future late payments may all fall into this category depending on your situation. But while these positive moves might counteract previous credit score damage, they won’t erase past credit mistakes from your credit history.

The good news is that you don’t need to improve your credit score by a full 200 points before you can start enjoying the benefits of your hard work. A much smaller credit score increase could be extremely valuable if it’s enough to help you qualify for financing or get a better interest rate than you would have previously.

Sources

- https://www.myfico.com/credit-education/calculators/loan-savings-calculator/

- https://www.ficoscore.com/ficoscore/pdf/Frequently-Asked-Questions-About-FICO-Scores.pdf

About the author

Michelle L. Black is a leading credit expert with over 17 years of experience in the credit industry. She’s an expert on credit reporting, credit scoring, identity theft, budgeting and debt eradication. See her on LinkedIn and Twitter.