Why Do I Have a Negative Balance on My Credit Card?

Usually, when you open your monthly credit card bill, you either owe money or have a zero balance. But there’s a third possibility: You could have a negative balance.

A negative balance on your credit card means your account has a credit balance, which may happen if you made returns, overpaid, or had fees canceled.

Key points

- A negative credit card balance means your card issuer owes you money rather than the other way around.

- It can occur for several reasons, including overpayments, refunds on returned purchases, statement credits, waived fees, or disputed charge reversals.

- You can request a refund, leave the balance to offset future purchases, or do nothing as it will not affect your credit score or credit limit.

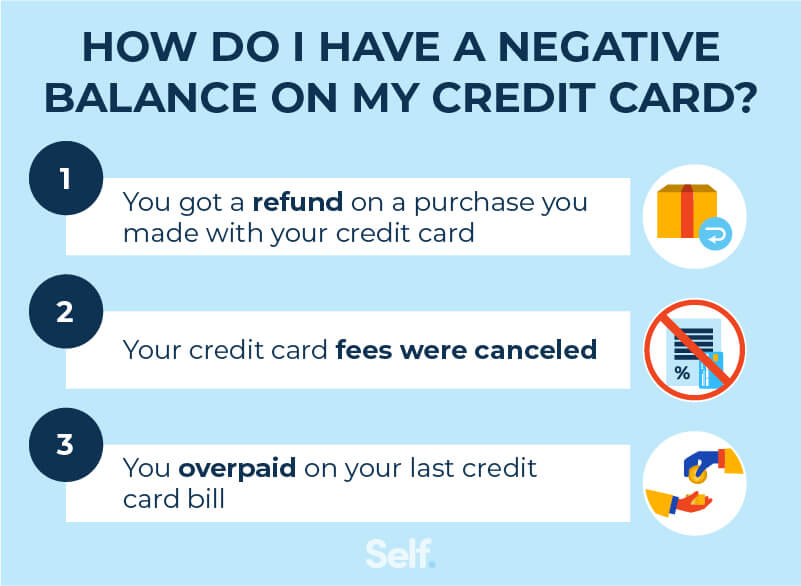

How do I have a negative balance on my credit card?

A negative credit card balance can occur for a number of reasons, including refunds, overpayments, or credits applied to your account.

Overpaying your credit card bill

If you make multiple payments toward your balance, you may end up paying more than you owe. This can happen if you enter an incorrect payment amount or submit a payment before a previous one has fully processed. Paying more than your current balance will result in a negative balance on your account.[1]

Refunds for returned purchases

If you return a purchase made with your credit card, the merchant may issue a refund as a credit to your account. If you have already paid off your balance, or if the refund amount is greater than your remaining balance, your account will show a negative balance.[1]

Statement credits

Some credit cards offer rewards that can be redeemed as a statement credit applied directly to your balance. If that credit exceeds your current balance, your account will show a negative balance.[1]

Waived fees

If a fee is charged to your account and later waived by your issuer, the reversal could result in a negative balance, particularly if you had already paid the fee before it was waived.[1]

Fraudulent or disputed charge reversals

If you report a fraudulent or disputed charge and your issuer resolves it in your favor, the amount will be credited back to your account. If you had already paid down your balance, this credit could push it below zero.[1]

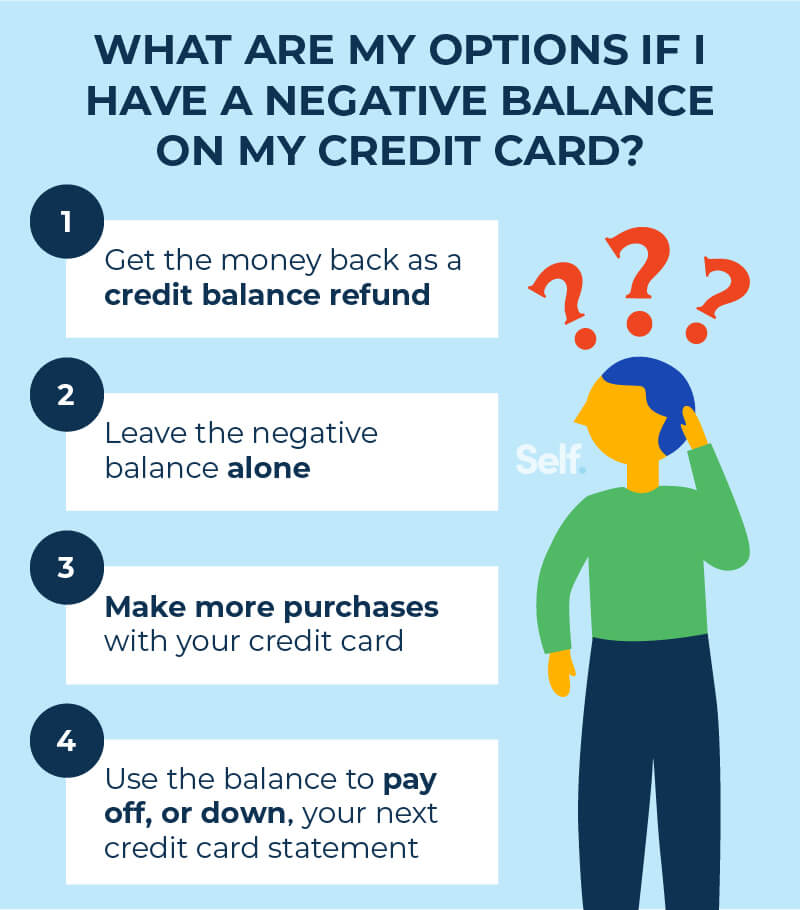

What are my options if I have a negative balance on my credit card?

Having a negative balance isn’t a bad thing. On the contrary, you have at least four options if you receive a credit card statement with a negative balance.

Get the money back as a credit balance refund

The Truth in Lending Act requires a lender to refund any negative balance over $1 within seven business days of receiving a written request. To request a refund under this provision, you can submit a written request to your credit card issuer. You may receive a refund in the form of a check, money order, or a deposit directly into your bank account.[2]

Make more purchases with your credit card

It’s easy to eliminate a negative balance by simply making new purchases on your credit card, thereby creating a zero or positive balance. [3]

You will want to be careful, however, to spend within your means. You don’t want to make too many future purchases and run up more interest charges on credit card debt you can’t pay. Another risk is that you forget to pay when it comes due because you mistakenly believe you still owe nothing.

Either scenario could damage your credit and personal finances.

Leave the negative balance alone

The easiest option is just to do nothing and leave the negative balance as it is. Your credit limit remains the same, but a negative balance increases your available credit, giving you a temporary extra cushion to spend against.

You can’t do this indefinitely, though. After six months, lenders are required to make a reasonable effort to return any negative balance. This means you may be mailed a check in the amount they owe you. [2] Consequently, while a negative balance may affect how much you can spend temporarily, it does not affect your credit limit. [3]

Use the balance to pay off, or down, your next credit card statement

If you are not interested in requesting a refund or making additional charges on your card immediately, you could allow the negative balance to remain on your account. Your creditor will likely apply the credit toward your future balance when additional charges are made.

You decide

If you have a negative balance and you want your money back, credit card companies are required to refund the money they owe you.

On the other hand, you can keep the negative balance on the books for up to six months. Moreover, it won’t hurt your credit score because credit card companies don’t report negative balances to the three main credit bureaus. As a result, the information won’t appear on your credit report.

You’ll appear to have a zero balance, which will indicate a low credit utilization ratio and reflect that you’ve made your monthly payments.

The bottom line

There’s nothing wrong with carrying a negative balance on your credit card. You can’t carry a negative balance indefinitely, but it can give you a temporary extra cushion. And it won’t hurt your credit because it will appear as a zero balance when reported to the credit bureaus.

As with anything else, you just have to be sure you keep an eye on your account for changes. Although it requires a little more effort, you may want to simply seek a refund, so you know where you stand and have a little extra cash to work with. But the choice is yours: If you have a negative balance, the credit card company can pay you now, or it can pay you later.

Sources

- Capital One. "What Is a Negative Balance on a Credit Card?" https://www.capitalone.com/learn-grow/money-management/overpay-credit-card/. Accessed May 22, 2026.

- Consumer Financial Protection Bureau. "§ 1026.11 Treatment of credit balances; account termination," https://www.consumerfinance.gov/rules-policy/regulations/1026/11/. Accessed May 22, 2026.

- Experian. "Can You Have a Negative Balance on a Credit Card?" https://www.experian.com/blogs/ask-experian/can-you-have-a-negative-balance-on-a-credit-card/. Accessed May 22, 2026.

About the Author

Lauren Bringle is an Accredited Financial Counselor® with Self Financial– a financial technology company with a mission to help people build credit and savings. See Lauren on Linkedin and Twitter.

About the author

Becca has over 10 years of experience as a content writer, working across various industries including finance, digital marketing, education, travel, and technology. Her work has been featured in publications including Forbes, Business Insider, AOL, Yahoo, GOBankingRates, and more.