What Bills Can You Pay with a Credit Card?

Most common household bills — including utilities, internet, phone service, insurance, medical bills, and even rent in some cases — can be paid with a credit card, though acceptance varies by provider. It is important to note that while using a credit card to pay your bills may offer convenience and rewards, some companies charge processing or convenience fees that can offset those benefits.

Before choosing to pay a bill with a credit card, it’s important to weigh potential rewards against added costs such as transaction fees or interest if the balance isn’t paid in full. Below, we break down which bills typically can be paid with a credit card and what to consider before using one. [1]

What bills should you pay with a credit card?

Some merchants may consider credit cards a nonstandard way to pay your bills, and credit card payments cost companies money to process. That’s why you may see a convenience fee or surcharge when you opt to pay by card instead of cash or check. [2] However, if it is commonplace to pay by credit card in a certain industry or business (such as everyday purchases in grocery stores), the company may not pass the fee on to you.

Service providers may allow you to pay bills with a credit card, but any of them could tack on convenience fees or other surcharges to offset their costs in the transaction. If you choose to pay rent using a credit card, for example, you could incur an extra fee for the payment to be processed through a third-party service.[3] If you pay $900 in rent, a 2.5% convenience fee for using a credit card would make your monthly payment $922.50.

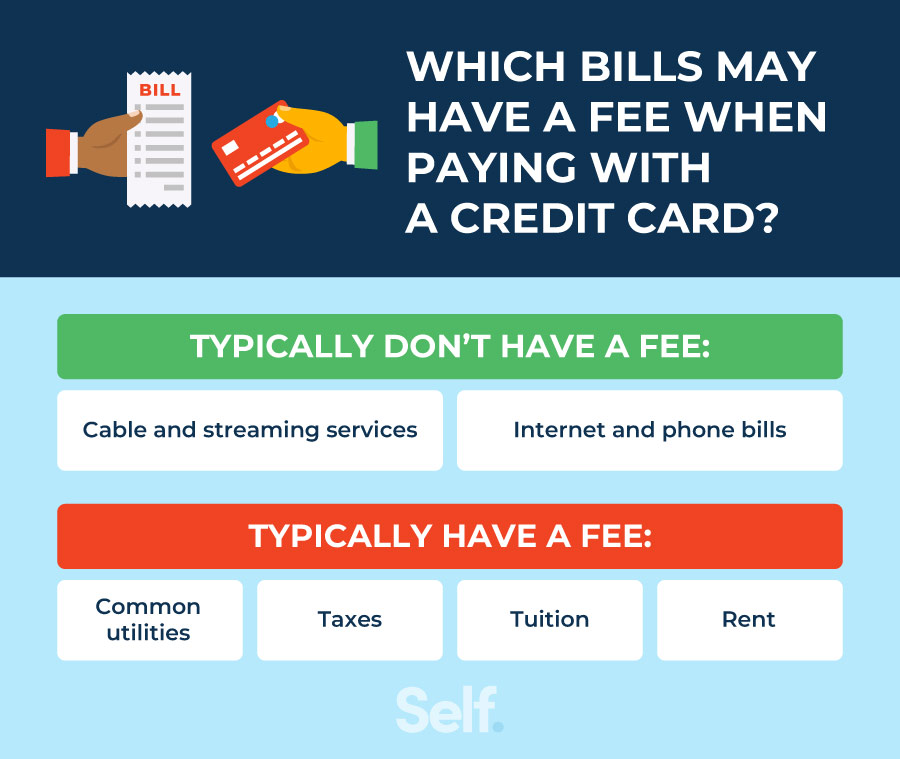

Bills that can generally be paid with a credit card

Payment options vary by provider, but the following utility bills are commonly eligible for payment with a credit card:[1]

- Cable service

- Electricity service

- Gas service

- Internet service

- Phone or mobile phone service

- Water service

Bills that typically have convenience fees for using a credit card

- Common utilities: They will likely pass these charges onto the consumer. They may charge a set amount (usually a few dollars) or a percentage of your total bill. Balancing how much these fees cost against what you receive in benefits — from the convenience of autopay to any cash back rewards — will help you decide if you should use a credit card for your utility bills.[1]

- Taxes: Paying taxes with a credit card typically involves a processing fee charged by the payment provider. For example, IRS-approved processors charge fees that are generally around 1.75% to 1.98% of the payment amount, depending on the provider.[5]

- Rent: Paying rent with a credit card usually requires the use of a third-party company, which may have an additional processing fee of 2% to 3% of the transaction amount. Again, unless you have decided that the benefits outweigh the drawbacks, you may not want to use a credit card to pay your rent.[3]

- Tuition: Much like taxes and rent, paying tuition with a credit card usually comes with a pretty steep convenience fee. FSome schools may charge a convenience fee when tuition is paid with a credit card, typically ranging from 2% to 3% of the transaction amount, which may reduce or outweigh any rewards earned. [6]

Bills that may not allow you to pay with a credit card

- Mortgages: Since lenders typically don’t accept direct credit card payments, you may find it difficult to pay your mortgage with a card. Like paying your rent, you would likely have to use a third-party service that could end up costing you an additional 2% to 3%.[3], [7]

- Loans: If you want to pay off a portion of your auto loan, private student loan, or personal loan with a credit card, you should contact the financial institution. Some lenders permit credit cards for loan payments, while others do not — or cannot by law. In some cases, people may consider using a credit card with a low or 0% introductory APR to pay off a loan. However, it’s important to weigh the pros and cons, as interest charges after the promotional period or additional fees could increase the total cost over time.[8]

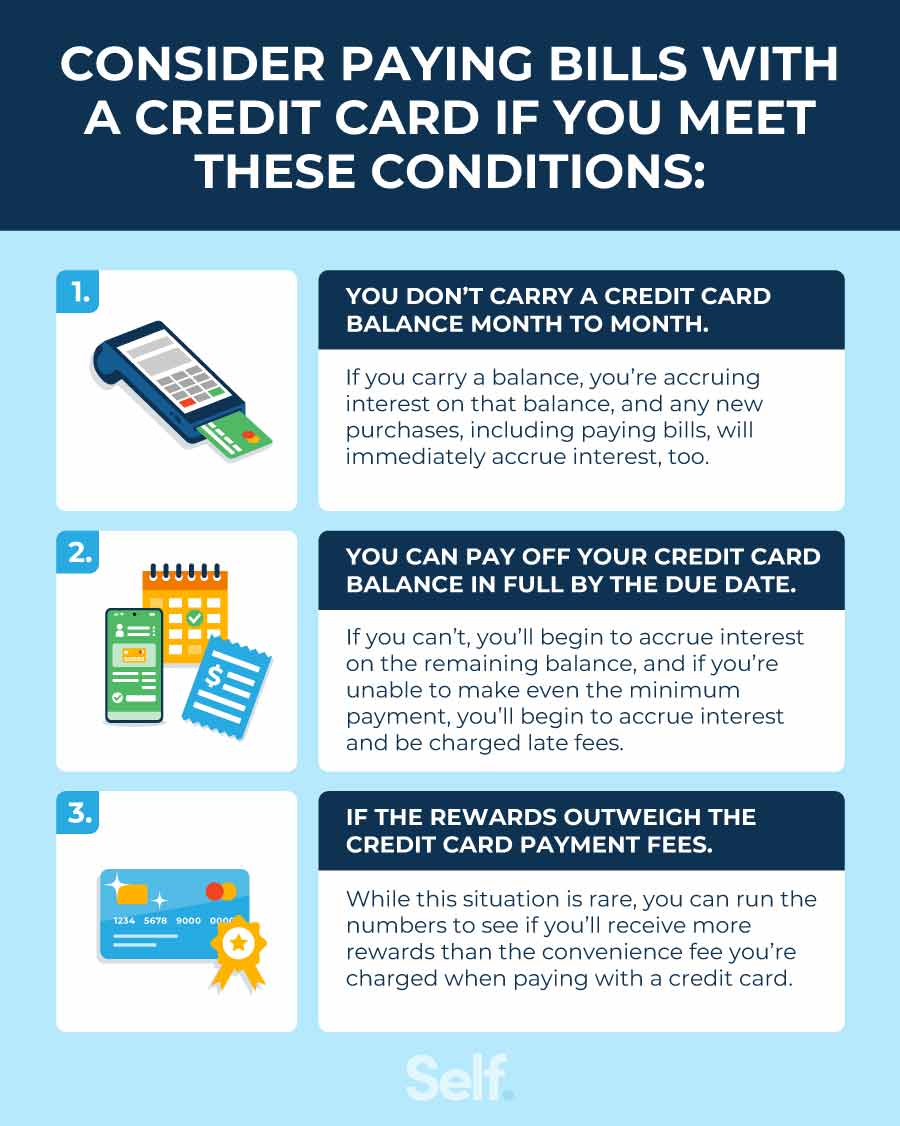

When should you consider paying bills with a credit card?

Depending on your unique financial situation and the specific bill involved, it may make sense to use a credit card. Below, we cover some common situations where you would consider using your credit card over other forms of payment. You may find the following guidelines useful when evaluating the best payment method for paying bills.

If you can pay off your credit card balance in full by the due date

The best credit cards to use when paying bills are those on which you don’t carry a balance and also pay the balance in full by the due date. Then you can take advantage of rewards and other perks without the drawbacks of paying interest.

Paying off your balance in full allows you to avoid credit card interest charges. [9]

Before paying a bill with a credit card, make sure that you can afford to pay everything you owe by the due date. If you can’t even pay the minimum payment, you’ll be charged late fees in addition to the interest on the balance.

If the rewards outweigh the credit card payment fees

Depending on your card’s program, putting a large bill on a credit card may help you gain rewards points quickly, especially with premium cards, and may pay off in cash back if you pay your balance by the due date (thereby avoiding additional charges).[3] Before deciding to pay a bill with a credit card solely for the perks, remember to consider fees, interest rates and other charges to make sure it makes sense.

When should you consider paying bills with another form of payment?

In other situations, it may make more sense to select another form of payment. The following considerations may help you decide when using a credit card to pay your monthly bills may not be the best choice.

If you can’t pay the minimum or full balance by the due date

When you don’t pay off your credit card bill in full each month, interest charges can add up fast. Furthermore, carrying a large balance can impact your CUR, eventually affecting your credit. While you may have a bill that’s so large you can only afford to put it on a credit card, make sure that you can at least make the minimum monthly payment. Failing to do so can result in late fees, impact your payment history and potentially impact your credit score.[10]

If the fees outweigh the benefits of using a credit card

Remember to calculate convenience fees and surcharges when deciding if it makes sense to use a credit card. Any rewards or cash back you may earn can quickly disappear. If you get 1% cash back on a $1,000 rental payment made by credit card, for example, you receive a $10 reward. If your landlord charges a $15 convenience fee, however, you actually end up losing $5 if you pay with a card. In this case, you may spend smarter by choosing another form of payment.

If you have high credit card debt

If you already have high credit card debt, paying bills with a credit card may not be the best option. You may want to focus on managing existing balances before taking on additional debt.

The Consumer Financial Protection Bureau recommends reviewing your financial situation, prioritizing payments, and contacting your lender or a credit counselor if you’re struggling to keep up with bills. [11]

Budget your expenses

Creating a budget can help you avoid taking on additional debt or simply get yourself into a better financial situation. If you have already accumulated a fair amount of debt, the following suggestions may help get your finances back on track.

- List off all of your debts and monthly expenses. An important first step to getting a handle on your finances is to have a good picture of where your money goes each month.

- Create an income-based budget to categorize your expenses. A basic budget can help you identify where to cut back and establish a payoff plan for debts. Setting monthly spending goals may enable you to use any extra cash to pay down balances on your credit cards or other debts.

- Find a debt repayment plan that works for you. The debt snowball method can help you pay down your debts by taking them one at a time. After making the minimum payment on all your accounts each month, any extra cash goes towards paying off the card with the lowest balance. The debt avalanche method offers a similar approach, but it has you start with the card with the highest interest rates.

- Have a discussion with your credit card issuer or a credit counselor for potential relief. Consider contacting your credit card issuer or a credit counselor for assistance. When speaking with your credit card company, you may need to explain why you’re unable to make payments, what you can afford, and when you may be able to resume normal payments. You can also consider working with a credit counseling organization, which can help you manage your money and understand your options.

[11]

Although you can pay several types of bills with a credit card, that doesn’t always mean you should. Any smart financial decision involves weighing the pros and cons of each option.

Sources

- Experian. “Can You Pay Utilities With a Credit Card?” https://www.experian.com/blogs/ask-experian/can-you-pay-utilities-with-credit-card/. Accessed on February 11, 2026.

- Discover. “What Is a Credit Card Convenience Fee?” https://www.discover.com/credit-cards/card-smarts/credit-card-convenience-fee/. Accessed on February 11, 2026.

- U.S. News & World Report. “Can You Pay Your Rent or Mortgage With a Credit Card?” https://money.usnews.com/credit-cards/articles/can-you-pay-your-rent-or-mortgage-with-a-credit-card. Accessed on February 11, 2026.

- Fifth Third Bank. “5 Monthly Expenses to Put on Your Credit Card.” https://www.53.com/content/fifth-third/en/financial-insights/personal/credit-cards/5-monthly-expenses-to-put-on-your-credit-card.html. Accessed on February 11, 2026.

- Internal Revenue Service. “Pay Your Taxes by Debit or Credit Card,” https://www.irs.gov/payments/pay-your-taxes-by-debit-or-credit-card. Accessed February 11, 2026.

- U.S. News & World Report. “Should You Pay Tuition With a Credit Card?” https://money.usnews.com/credit-cards/articles/should-you-pay-tuition-with-a-credit-card. Accessed February 11, 2026.

- Forbes. “How To Pay Your Mortgage With a Credit Card.” https://www.forbes.com/advisor/credit-cards/how-to-pay-your-mortgage-with-a-credit-card/. Accessed on February 11, 2026.

- Chase. “Can You Pay Off a Loan With a Credit Card?” https://www.chase.com/personal/credit-cards/education/basics/can-you-pay-off-a-loan-with-a-credit-card. Accessed on February 11, 2026.

- TransUnion. “Paying the Balance vs. Paying the Minimum on a Credit Card.” https://www.transunion.com/blog/debt-management/credit-card-101-paying-the-balance-vs-paying-the-minimum. Accessed on February 11, 2026.

- Experian. “What Happens if You Only Pay the Minimum on Your Credit Card?” https://www.experian.com/blogs/ask-experian/what-happens-if-you-only-pay-the-minimum-amount-due/. Accessed on February 11, 2026.

- Consumer Financial Protection Bureau. “What Should I Do If I Can’t Pay My Credit Card Bills?” https://www.consumerfinance.gov/ask-cfpb/what-should-i-do-if-i-cant-pay-my-credit-card-bills-en-1697/. Accessed February 11, 2026.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

About the author

Becca has over 10 years of experience as a content writer, working across various industries including finance, digital marketing, education, travel, and technology. Her work has been featured in publications including Forbes, Business Insider, AOL, Yahoo, GOBankingRates, and more.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).