What Is Bill Pay and Why to Consider It?

Bill pay is an online service that banks and credit unions provide you as an efficient way of making payments to companies or individuals in one place. By using this electronic payments service, you can schedule e-bill payments all in one place to ensure you don’t forget any bills and rack up late payments as a result. You can also use the service to pay bills manually if you are worried about overdrafts.[1][2]

Most electronic bill pay transactions are electronic transfers between accounts. However, if you are making a payment to an individual at a financial institution that does not accept these electronic payments, bill pay will send them a paper check.

Bill pay is a great option if you’re looking for an easier way to manage your bills and make payments, and this guide discusses some of the basics of how online bill pay works and how to get the most out of online bill payment.

How to set up bill pay with your bank or credit union

The first step is to set up your account at a bank or credit union to make bill pay transactions. You may have to do this via your desktop computer or via the mobile app. Either way, once it is set up, you can typically use your app to make payments. To set up bill pay, follow the steps below (although keep in mind these steps may vary somewhat depending on how your bank does bill pay).[2]

- Determine which bills you want to pay with bill pay. Once you’ve collected all of your bills, choose from the bills you want to pay with bill pay. This may be some or all of your bills — the number of bills you pay online is your choice.

- Add all of the payees’ information within bill pay. Include the requested information (such as account number, contact info, and so on) that will allow the bank to transmit the payment to the biller.

- Set up or select the account you want to make payments with. If you have multiple accounts with the banks (like a checking account and a savings account), you will need to choose the one you want to use to make payments.

- Select a payment option. You likely will be able to choose between scheduled or manual payment options, and you may also have the option for quick pay (quickly allows you to select a payee, the amount to send and the date to send the payment), classic pay (similar to quick pay, but gives you more options for sending a payment, such as frequency and memo) or multi-pay (gives you the option to pay multiple bills at one time in one session).[3]

Because not all banks and credit unions may have the same options or set up bill pay in the same way, check with your banking institution online or in person to discuss your bill pay options.

How can bill pay help me?

But why should you bother with bill pay and not just keep using paper bills the way you always have? Everyone’s situation is different, and bill pay may not be the best option for you. However, you should understand a couple of the benefits of bill pay before making a decision.

You can view all of your bills in one place and budget accordingly

With bill pay, if you’re paying all of your bills online, you’ll be able to see all of your bills in one place. So you can have an easier time when you need to create a budget since you can see where all your money goes.

Bill pay can also help you avoid late payments because you can view your bills all in one location. At one glance, you can see what bills need to be paid, the payment amounts, and when they are due, and that helps you get the right payments in on time, which is good because making payments on time is important for your credit score.

You can take control of your payments

Bill pay can take a little time to set up because you have to collect all of your bills and decide which ones to add to bill pay, but once you set it up, you have better control of your payments. Depending on your bank’s available options for setup, you may be able to choose from various flexible payment options, such as quick pay, multi-pay, classic pay, scheduled and manual.[1]

While it takes a little time to figure it all out, it will make your life easier in the long run by helping you avoid missed payments. You will begin to understand which bills work better with certain payment methods based on your situation. For example, you might want some bills, perhaps larger ones, to be paid manually so you can check the total in your account balance to ensure you can cover the payment. Or maybe you have a bill, like a utility bill, that fluctuates. You’ll want to be sure you don’t schedule a specific amount and end up paying less than what you owe.

You may even be able to set up notifications that alert you before a bill is due. You have many options to set yourself up for success in getting bills paid on time. Because lenders usually report late payments to the credit bureaus, on-time payments will have a positive effect on your payment history and may positively impact your credit score.

How can I get the most out of bill pay?

You can use bill pay strategically to improve your financial situation. Here are a few tips to help you get the most out of bill pay.

Track your funds to avoid overdrafts

If you opt for scheduled or automatic payments, track your funds so your account doesn’t run low when a payment is coming up. If your account is lower than the scheduled payment, the scheduled payment will either bounce or your account will overdraft, incurring fees and penalties. If this is happening often, it may cause you to take on debt and therefore you may want to switch to manual payments.[1]

Know the processing time so you pay on time

Sometimes, service providers for bill pay, such as banks and credit unions, will encourage you to schedule payments before the bill’s due date for it to arrive on time. For example, U.S. Bank requires five business days and Capital One requires four days. This may strain some users who may need a little more time before making the payment. You may need to prioritize payments, making sure the ones requiring more processing time get paid first.[4][5][6]

Manually pay fluctuating bills to avoid underpayment

Most monthly bills are the same each month, but some bills fluctuate, making it difficult to use bill pay. In that case, you’ll likely need to make one-time payments to avoid underpayment (or overpayment). So monitor your bill pay arrangements and keep an eye on each bill that a service provider submits to ensure you pay the correct amount each month.[1]

Plus keeping track of these amounts allows you to average your monthly costs for this specific bill. This comes in handy so you can budget properly. If you budget for the average cost, save the average in the months where your bill is lower so you can use it to pay the bill when it’s higher than average.

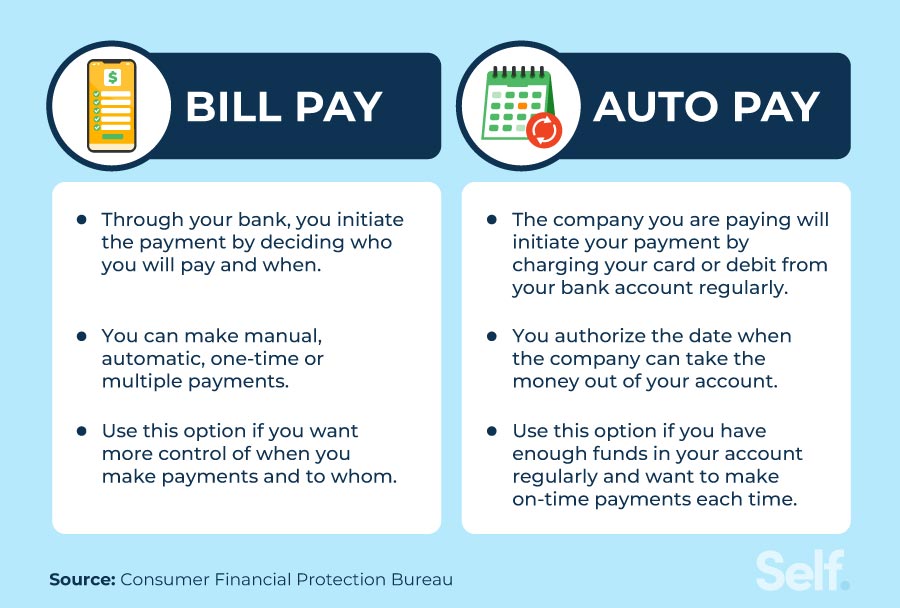

Bill pay vs. auto pay

Bill pay and auto pay may sound interchangeable, but they both operate differently. With bill pay, you’re initiating payments. You set up the payments to the companies through your bank account or credit union account. On the other hand, with auto pay, you’re allowing a company to charge your credit card or bank account on a recurring basis. In other words, with bill pay you are sending payments, and with auto pay they are pulling money from your account.[7]

They both carry the same benefit of protecting you from late payments and carry the same risk of creating the potential for overdrafts. However, you encounter more of a hassle to cancel auto-pay, since you would have to contact the company or perhaps even contact your bank to issue a stop-payment order (which carries a fee).[8]

Before you enroll in bill pay with your financial institution, you should consider how best you can incorporate this tool to make on-time payments so that you can impact your payment history positively. To make the most of your credit-building journey, Self’s financial products and information can help you get on the right track to understand how your payment habits can impact your credit.

Sources

- Consumer Financial Protection Bureau. "Ways to pay your bills," https://files.consumerfinance.gov/f/201507_cfpb_ways-to-pay-your-bills.pdf. Accessed Oct. 13, 2022.

- Capital One (YouTube video). "How To Set Up Bill Pay (reducing unnecessary errands)," https://www.youtube.com/watch?v=wAI4nXzkPIk. Accessed Oct. 13, 2022.

- Jeanne D'Arc Credit Union (YouTube video). "Online Banking: Bill Pay Tutorial," https://www.youtube.com/watch?v=5t6yYOt8Acg. Accessed Oct. 13, 2022.

- USBank. "How far in advance can I schedule a bill payment?" https://www.usbank.com/customer-service/knowledge-base/KB0203426.html. Accessed Oct. 13, 2022.

- Capital One. "Set up Bill Pay," https://www.capitalone.com/help-center/checking-savings/set-up-bill-pay. Accessed Oct. 13, 2022.

- Consumer Financial Protection Bureau. "I made a payment through my bank or credit union's online bill pay service. The payment arrived after the due date and I was charged a late fee. When should my bill pay payment have arrived?" https://www.consumerfinance.gov/ask-cfpb/i-made-a-payment-through-my-bank-or-credit-unions-online-bill-pay-service-the-payment-arrived-after-the-due-date-and-i-was-charged-a-late-fee-when-should-my-bill-pay-payment-have-arrived-en-1125. Accessed Oct. 13, 2022.

- ReliaBills. "Auto Pay vs. Bill Pay – Which One is Highly Recommended?" https://www.reliabills.com/blog/auto-pay-vs-bill-pay. Accessed Oct. 13, 2022.

- Consumer Financial Protection Bureau. “How do I stop automatic payments from my bank account?” https://www.consumerfinance.gov/ask-cfpb/how-do-i-stop-automatic-payments-from-my-bank-account-en-2023/. Accessed October 25, 2022.

About the author

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.

Editorial policy

Our goal at Self is to provide readers with current and unbiased information on credit, financial health, and related topics. This content is based on research and other related articles from trusted sources. All content at Self is written by experienced contributors in the finance industry and reviewed by an accredited person(s).