The Causes and Costs of a Negative Bank Balance

Key points

- A negative bank account balance occurs when the amount of money in your account is less than zero.

- A negative balance may result in fees, account closure, and potentially affect your ability to open new accounts. In some cases, unpaid negative balances could lead to legal action, including wage garnishment.

- You can opt in to overdraft protection. However, using this type of service can involve fees.

- Stay up to date on your available balances and transactions to prevent a negative account balance.

Spending more money than you have in your bank account will cause a negative bank balance. In addition to leaving you without available cash, a negative balance can cost you in fees — and it might not be just one fee, either. Your bank may charge you a fee each time you overdraw your account.

Overdraft fees can add up quickly. According to a Bankrate survey in 2024, they average $27.08 for each occurrence. [1] That’s why it’s important to avoid a negative account balance. The most obvious way to do so is to have enough money in your account to cover your transactions and employ strategies to alert you if your available balance is low.

Table of contents

- What is a negative bank account balance?

- What causes a negative bank account balance?

- What is overdraft protection?

- What could happen if you have a negative balance?

- What to do if your bank account balance is negative

- Tips to avoid overdrawing your account

- Negative bank balance FAQ’s

What is a negative bank account balance?

A negative balance is what happens when the amount of money in your account is less than zero.

A negative balance on your bank statement isn’t the same as a negative credit card balance on your credit card statement. In the latter case, it means you’ve overpaid or received a refund and the credit card company owes you money. In the former, it means your purchases have exceeded your available funds and you owe the bank money.

A negative account balance may bring with it two kinds of fees:

- Overdraft fee: This occurs when the bank covers the transaction, even if you don’t have enough money in your account to pay for it.

- Non-sufficient funds fee: This happens when you try to make a transaction, but there isn’t enough money in the account to pay for it.

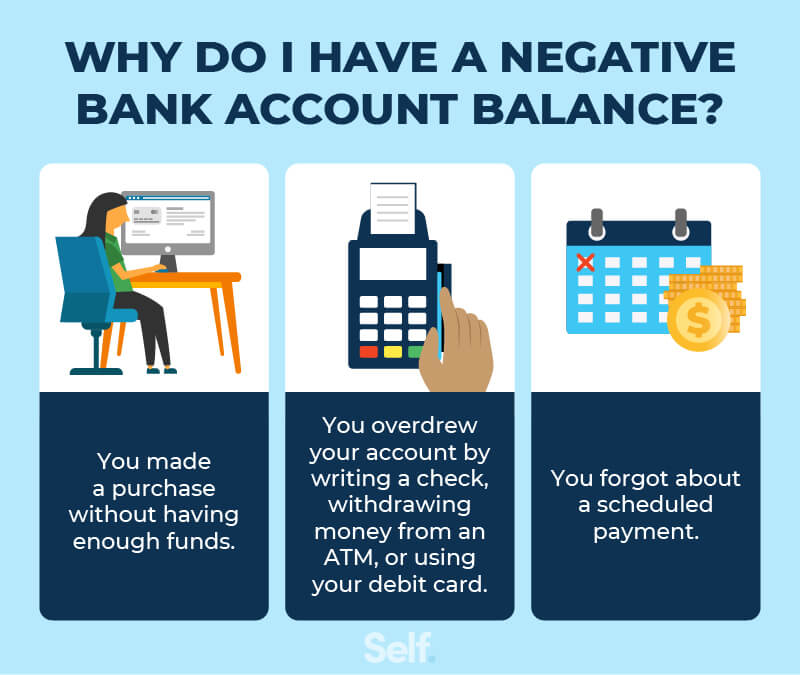

What causes a negative bank account balance?

There are a variety of reasons your bank account may have a negative balance:

- You forgot how much money was in your account.

- You overdrew your account by writing a check, withdrawing money from an ATM or using your debit card.

- You forgot about a scheduled payment. This may be more likely to happen on payments that occur at irregular intervals, such as automatic payments that are taken out every six months or once a year.

- A payment you made was late in posting to your account.

- Someone delayed cashing a check you’d written and it reaches the bank at a time when you have a low balance.

A negative bank account balance can trigger fees and leave you unable to access your funds, either to pay bills or make purchases. Bank charges may follow, and at worst, you may face account closure.

What is overdraft protection?

An overdraft protection plan is an overdraft service provided by your bank that ensures that the transaction goes through. When a customer opts in for this service, the bank designates a backup account for the bank to use as a source of funds to cover any overdrafts. This is typically a linked savings or line of credit account. The bank charges the customer overdraft fees to process the transaction.

Federal regulations prohibit banks from automatically enrolling their customers in this program. Opting into this service has its pros and cons. On the one hand, you are guaranteed that your transaction will be covered. On the flipside, you have to pay fees for the service. [2]

What could happen if you have a negative balance?

A negative account balance can have a variety of consequences, none of them good. Here are a few things that might happen.

Fees

You can face penalties in the form of fees that you will have to pay if you overdraw your account. As mentioned above, there are two main types of fees banks charge: overdraft fees and non-sufficient fund (NSF) fees.

Some banks charge you an overdraft fee each time you make a transaction while you’re in the red, so if you don’t notice a problem right away, you could be on the hook for overdraft fees into the triple digits. Other banks charge you a fee each day your account balance stays below zero.

A non-sufficient funds (NSF) fee is a fee your bank charges you if you try to spend more money than is in your account. Unlike an overdraft, the bank won’t cover anything more than what you have in your account, so you won’t go into the red. Instead, your debit card will be declined or your check will bounce. But you’ll still have to pay an NSF fee on top of that. [2]

The bank could close your account

A bank can close your account for any reason and without warning. This is called an involuntary closure. [3]

Reasons for an involuntary closure include too many bounced checks or overdrafts, maintaining a zero balance for too long, or failing to reconcile a negative balance. Questionable activity that may lead the bank to suspect identity theft can also lead to an involuntary closure, and so can a previously undisclosed criminal conviction.

Your bank may also limit the number of transfers you can make between accounts. If you exceed this limit, such as by repeatedly moving money from your savings account to your checking account to cover your expenses, the bank may close one of your accounts.[3]

Your credit score might decline

An overdraft does not affect your credit score directly. Your bank is not a creditor and therefore won’t report an overdraft to the three major credit bureaus.

However, having a negative bank balance can affect your credit indirectly. For instance, if you go to make a payment on your credit card, but the payment is declined because of non-sufficient or insufficient funds, you may wind up being late, which can hurt your credit. This is because payment history counts for the biggest chunk of your credit score (35%) under the FICO® system. Learn more about how credit score is calculated. [4]

Wage garnishment

If you overdraw your bank account, you owe the bank however much you’re in the red, plus any fees the bank may charge. If you don’t pay, the bank can take you to court and obtain a judgment against you. If they win the judgment, the court may allow them to garnish your paycheck. (Note: Not all states allow wage garnishment.) While this is an extreme consequence, it can happen. [5]

Opening a new checking account might be difficult

There is a bank reporting bureau called ChexSystems that monitors bank and credit union accounts for things like bounced checks, unpaid negative balances, overdrafts, fraud and involuntary closures. This doesn’t affect your credit report or score, but negative marks from ChexSystems may hurt your ability to open a new bank account in the future.[6]

A bank or credit union has every right to deny your application for a new account based on negative information in your banking history.[7]

What to do if your bank account balance is negative

If your bank account balance is negative, the worst thing you can do is ignore it. It’s important to take steps to rectify the situation. Here are some things you can do.

1. Ask if the bank can waive any fees

If you’ve overdrawn your account, and it’s not a regular occurrence, your bank may be willing to reverse the fee — especially if you have a good and reasonable explanation.[8]

You can contact your bank, explain what happened, and ask them to reverse the fee. If you have already paid your balance, that’s a point in your favor. If not, assure them that you plan to do so promptly. Politely remind them of your history as a reliable and valued customer, and ask to speak to a supervisor if the customer service representative can’t help you.

You may not want to give up after the first try; consider calling back at another time and talking to someone else to see if you can get overdraft fees back.

2. Pay necessary fees

Paying the fees you owe promptly shows the bank that you take the matter seriously and can help you avoid further overdraft fees. It will also restore access to your account.

3. Transfer money into the account

If you have more than one bank account like a savings account or a second checking account at the same institution, or a separate account at a different bank or credit union, you can transfer some of the funds from these accounts to the overdrawn account to put your account back in the black and keep you from risking further fees.

Tips to avoid overdrawing your account

The best way to deal with a negative bank account balance is to avoid having one in the first place. You can reduce the chances of winding up with a negative balance by taking some of these steps:

- Stay up to date on your available balances and transactions by checking your account online daily.

- Sign up for balance alerts or low-balance notifications from your bank so you’ll know when you need to stop spending and/or deposit more money into your account.

- Use direct deposit so you will know when your paycheck, benefits check or other forms of income will be available in your checking account.

- Consider linking your accounts so money from a secondary account can be used to cover any deficit in your checking account. Be aware that some banks may charge a fee for these automatic transfers, though this fee may be lower than an overdraft fee. [2]

- Be cautious about overdraft protection programs. Federal regulations prohibit banks from automatically enrolling customers in overdraft protection, and you cannot be enrolled without your permission. [2] If you don’t enroll in overdraft protection, the bank will simply decline purchase and withdrawal attempts that would push your balance into the negative.

Negative bank balance FAQs

Here are some frequently asked questions on how to deal with negative balances on your account.

Can you still use the cards linked to your bank account?

If you have overdraft coverage on your account, you may be able to continue using your debit card up to a point. However, in doing so, you risk incurring an overdraft fee with each use, so it’s not a good idea to do so.

Do you have to pay the negative balance back?

Yes, you do. Otherwise, your account will turn into a debt. Your bank can close your account and pursue legal means of recovering the money you owe.

How long does a bank allow a negative balance?

The timeframe varies by bank, and there is no standard minimum period. Account agreements may specify that banks will provide written notice before closing an account with a negative balance, but policies differ among financial institutions. Banks are not required to maintain accounts with negative balances for any specific length of time. [9]

What does the bank do when your account balance is negative?

A financial institution can close an account or freeze it if you fail to pay a negative balance, which might later appear on your credit reports as a collection account. While the bank can close an account with a negative balance, that doesn’t negate the responsibility to pay that balance. Similarly, the client can’t close the account in an attempt to eliminate the balance; the bank is the one that can terminate the account if it has a negative balance. [9]

How is your credit impacted by a negative bank account balance?

If you don’t pay a negative balance over a period of time, the bank may sell your debt to a collections agency. The debt collector will attempt to collect it along with additional fees. The collection agency will then create an account in your name and report that information to the credit bureaus if you refuse to pay. [10]

Any number of things can lead to a negative balance in your bank account, from debit card transactions to automatic payments to delayed checks. Monitoring your finances can help you avoid costly fees and problems that can ultimately affect your credit if you are unable to repay what you owe.

Staying on top of your account balances while monitoring your payments and transactions closely is key to ensuring you avoid negative balances, fees, and the risk that your account may be closed.

Sources

- Bankrate, “What is an Overdraft Fee?” https://www.bankrate.com/banking/checking/what-is-an-overdraft-fee/ Accessed February 5, 2026

- ABA, “Understanding Overdraft Protection” https://www.aba.com/advocacy/community-programs/consumer-resources/manage-your-money/understanding-overdraft Accessed February 5, 2026

- Motley Fool, “Involuntary Bank Account Closure and How to Avoid It” https://www.fool.com/retirement/2026/01/13/involuntary-bank-account-closure-how-to-avoid-it/ Accessed February 5, 2026

- MyFICO, “How Are FICO Scores Calculated?” https://www.myfico.com/credit-education/whats-in-your-credit-score Accessed February 5, 2026

- SoFi, “What Happens if You Overdraft Your Bank Account and Don’t Pay it Back?” https://www.sofi.com/learn/content/what-happens-if-you-overdraft-your-bank-account-and-dont-pay-it-back/ Accessed February 5, 2026

- Consumer Finance, “Chex Systems” https://www.consumerfinance.gov/consumer-tools/credit-reports-and-scores/consumer-reporting-companies/companies-list/chex-systems/ Accessed February 5, 2026

- Consumer Finance, “Why Was I Denied a Checking Account?” https://www.consumerfinance.gov/ask-cfpb/why-was-i-denied-a-checking-account-en-1113/ Accessed February 5, 2026

- U.S. News, “How to Get Overdraft Fees Waived” https://www.usnews.com/banking/articles/how-to-get-overdraft-fees-waived Accessed February 5, 2026

- SoFi, “What Happens if Your Bank Account Goes Negative?” https://www.sofi.com/learn/content/negative-bank-balance/ Accessed February 5, 2026

- Discover, “Does an Overdraft Affect Your Credit Score?” https://www.discover.com/credit-cards/card-smarts/does-an-overdraft-affect-your-credit-score/ Accessed February 5, 2026

About the author

Jeff Smith is the VP of Marketing at Self Financial. See his profile on LinkedIn.

About the reviewer

Ana Gonzalez-Ribeiro, MBA, AFC® is an Accredited Financial Counselor® and a Bilingual Personal Finance Writer and Educator dedicated to helping populations that need financial literacy and counseling. Her informative articles have been published in various news outlets and websites including Huffington Post, Fidelity, Fox Business News, MSN and Yahoo Finance. She also founded the personal financial and motivational site www.AcetheJourney.com and translated into Spanish the book, Financial Advice for Blue Collar America by Kathryn B. Hauer, CFP. Ana teaches Spanish or English personal finance courses on behalf of the W!SE (Working In Support of Education) program has taught workshops for nonprofits in NYC.